Class 12 AHSEC 2020 Accountancy Question Paper Solved in English Medium, AHSEC Class 12 Accountancy Question Paper Solved PDF Download, to each Paper is Assam Board Exam in the list of AHSEC so that you can easily browse through different subjects and select needs one. AHSEC Class 12 Accountancy Previous Years Question Paper Solved in English can be of great value to excel in the examination.

Class 12 AHSEC 2020 Accountancy Question Paper Solved English Medium

AHSEC Old Question Paper provided is as per the 2020 AHSEC Board Exam and covers all the questions from the AHSEC Class 12 Accountancy Solved Question Paper 2020 English Medium. Access the detailed Class 12 Accountancy 2020 Previous Years Question Paper Solved provided here and get a good grip on the subject. AHSEC 2020 Accountancy Question Paper Solved Access the AHSEC 2020 Accountancy Old Question Paper Solved, AHSEC Class 12 Accountancy Solved Question Paper 2020 of English in Page Format. Make use of them during your practice and score well in the exams.

ACCOUNTANCY

2020

ACCOUNTANCY OLD QUESTION PAPER SOLVED

1. (a) Fill in the blanks with appropriate word / words:

(1) Unrecorded liabilities when paid are debited to Realisation Account.

(2) Life membership Fee is a Capital receipt.

(3) A partner acts as an agent of the firm.

(4) A company is required to publish its financial statements every year.

(b) Choose the correct alternative:

(1) When a new partner does not bring in his share of goodwill in cash, the amount of premium is debited to:

(a) Premium Account.

(b) Cash Account.

(c) Capital Account of new partner.

(d) Capital Account of old partner.

Ans: (c) Capital Account of new partner.

(2) Financial statements are:

(a) Summarised reports of recorded facts.

(b) Detailed reports of recorded facts.

(c) Summarised reports of only cash transactions.

(d) None of the above.

Ans: (a) Summarised reports of recorded facts.

(3) State whether the following statements are “True” or “False”:

(a) Subscription received in advance is an asset.

Ans: False, Liability.

(b) Interest on debenture is payable only when a company earns profits.

Ans: False, It is a charge.

2. Mention two differences between Receipts and Payments account and Income and Expenditure account.

| Basic | Receipt and Payment Account | Income and Expenditure Account |

| 1. Nature | It is a Real Account in nature. | It is nominal Account in nature. |

| 2. Basis | It is prepared on cash basis of accounting. | It is prepared on accrual basis of accounting. |

3. What is Premium for Goodwill?

Ans: Premium for Goodwill: When a new partner is admitted into the firm, he is required to compensate in favour of partners who sacrifices their shares in favour of new partner. The Compensation paid in cash by the new partner to the sacrificing partners is called premium for goodwill.

4. Give two situations under which a partnership firm is dissolved.

Ans: A Partnership is dissolved when:

(a) On expiry of the term for which the firm was constituted.

(b) If firm is constituted for a particular venture and that venture is completed.

5. A, B and C are partners sharing profits in the ratio 3:2: 1. A retires. B and C have decided to take up A’s share equally. Calculate the new ratio.

Ans: A: B: C = 3:2:1 (old ratio)

A’s share = 3/6 (acquired by B’s C in 1:1 ratio)

Now’ A’s share acquired by B = 3/6 x ½ = ¼

A’s share acquired by C = 3/6 x ½ = ¼

Again, B’s New share = 2/6 + ¼ = 4+3/12 = 7/12

C’s new share = 1/6 + ¼ = 2+3 /12 = 5/12

B: C = 7:5 (New ratio)

6. Name any two items of current assets.

Ans: Cash in Hand, Cash at Bank

7. Mention three uses of financial statement.

Ans: Uses of financial statements:

(a) To Management: Management is interested in knowing the existing profits, earnings per share, chances of survival, possibility of growth and diversification etc. from the financial statements so that is can frame suitable strategy for its entity.

(b) Potential investors: Potential investors are keen to know the earning potential of the business. They want to know how safe the investment already made is and how safe the proposed investment will be.

(c) Bankers and financial institutions: These institutions are interested in the security of the loan advanced, entity’s capacity to repay the principal interest as per terms. Financial statements help these institutions to check the operating efficiency and financial position.

8. What is common size statement? Mention its two uses.

Ans: Common Size Statements: Common size statement is a statement in which amounts of individual item of balance sheet and profit and loss account for one or more years are expressed in terms of percentage of a common base. The common base can be net sales in the case of profit and loss account and total of balance sheet for the balance sheet.

Uses of Common size statement:

(i) A common size statement facilitates both types of analysis, horizontal as well as vertical. It allows both comparisons across the years and also each individual item as shown in financial statements.

(ii) It helps in finding trend of percentage share of each asset in total assets and percentage share of each liability in total liabilities.

(iii) These statements help the management in making forecasts for the future.

Or

Q.9. Current Ratio is 3: 5: 1 and Quick Ratio 2: 5: 1. Inventory is Rs. 50,000. Calculate current assets and current liabilities.

Ans: Given,

Current ratio = 3: 5: 1

Quick ratio = 2: 5: 1

Inventory = 50,000

Now, let the CA be 3.5x

LA be 2.5x

CL be x

A/q, CA-LA = Inventory

⇒ 3.5x – 2.5x = 50,000

⇒ x = 50,000

CA = 3.5 x 50,000 = 1, 75,000

CL = 50,000

9. Explain the super profit method of valuation of goodwill.

Ans: Super Profit Method: Super Profits means excess of actual average maintainable profits over normal Profit of a firm. Normal profits mean the profit which the firms could normally earns in a particular business. It is calculated by multiplying capital employed in the firm with normal rate of return. Goodwill under this method is calculated by multiplying super profit with the agreed number of year’s purchase.

Under this method, the following steps are to be followed for calculation of goodwill:

1. Calculate average maintainable profit with the help of following formula: Total Actual maintainable profits /no of years.

2. Calculate normal profit by multiplying capital employed with normal rate of return.

3. Calculate super profit. Super profit is the excess of average maintainable profit over normal profit.

4. Calculate the value of goodwill = super profit x no. of year’s purchase

10. State three features of Not-for-profit organisation.

Ans: Characteristics of Not-for-profit organisations: Following are the main characteristics or the salient features of Not for Profit organisations:

(a) The main objective of not-for-profit organisations is not to make profit but to provide service to its members and to the society in general.

(b) The main source of income of these organisations is admissions fees, subscriptions, donations, grant-in-aid, etc.

(c) Financial statements of not for profit organisations include receipts and Payments A/C, Income and Expenditure A/c and Balance sheet.

Or

Calculate the amount of subscription to be credited to Income and Expenditure Account for the year ended 31st March, 2019.

(1) Subscription received during the year ended 31st March, 2019 Rs. 2, 50,000.

(2) Outstanding subscription on 1/4/2018 Rs. 50,000.

(3) Outstanding subscription on 31/03/2019 Rs. 35,000.

(4) Advance subscription on 01/04/2018 Rs. 25,000.

(5) Advance subscription on 31/03/2019 Rs. 30,000.

Ans: Calculation of subscription Income:

| Subscription receivedAdd: Out subscription (31-03-19)Add: Advance subscription (1-4-18)Less: Out subscription (1-4-18)Less: Advance subscription (31-03-19)Subscription Income | 2, 50,00035,00025,00050,00030,0002, 30,000 |

11. What is gaining ratio? Give two distinctions between gaining ratio and sacrificing ratio.

Ans: Gaining Ratio: Gaining Ratio is calculated at the time of retirement or death of partner. It is the excess of new share over old share. It is calculated as follows: Gaining Ratio = New share – Old share. Calculation of gaining ratio is necessary to compensate the outgoing partners by payment of goodwill in their gaining ratio.

Distinguish between sacrificing ratio and gaining ratio:

| Basis | Sacrifice Ratio | Gaining Ratio |

| Meaning | Sacrificing Ratio is a ratio in which the old partners have agreed to surrender their share of profit in favour of new partner. | Gaining Ratio is ratios in which remaining partners’ gain the retiring partner’s share. |

| Objective | The main purpose to calculate the sacrificing ratio is to ascertain the compensation to be paid by incoming partner to the sacrificing partner’s in the form of goodwill. | The main purpose to calculate the gaining ratio is to find out the compensation to be paid by the gaining partner’s to the retiring partner. |

| When to Calculate | Sacrificing Ratio is calculated at the time of admission of a new partner. | Gaining Ratio is calculated at the time of retirement or death of a partner. |

| Method | Sacrificing Ratio = Old Ratio – New Ratio | Gaining Ratio = New Ratio – Old Ratio |

| Effect | It reduces the profit sharing ratio of the existing partners. | It increases the profit sharing ratio of the remaining partners. |

Or

What are the items shown under shareholders’ fund?

Ans: Items shown under shareholder’s fund:

(1) Shareholders’ Funds.

(a) Share capital.

(b) Reserves and surplus.

(c) Money received against share Warrants.

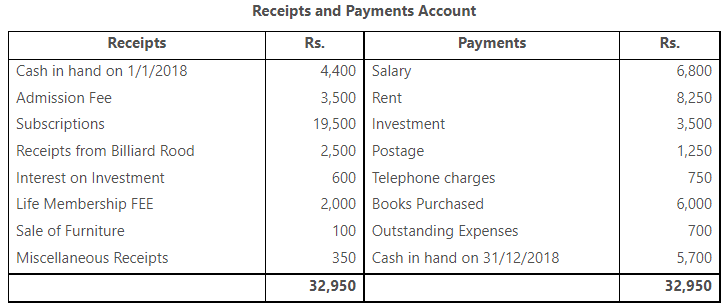

12. Prepare Income and Expenditure A/c from the following Receipts and Payments A/c of Ekta Club for the year 31st December, 2018:

Additional information:

(1) Outstanding subscription Rs. 1,000.

(2) 60% of the admission fees and the whole of the life membership subscriptions are to be capitalized.

(3) Depreciation on Books Rs. 600.

Ans: Students Do Yourself.

Or

What is the meaning of Fund Based Accounting? Mention any three principles of Fund Based Accounting.

Ans: Fund based accounting is used in Non-Profit concerns to record transactions related to certain items. In such cases a fund is created in the books of accounts & all the revenues related to that item, for which we have created a fund, are added to the fund and all the related expenses are subtracted from the fund.

There are three principles of Fund Based Accounting.

- Variations in Fund Accounting.

- Accountability Over Profitability.

- Reporting and Oversight.

1. Variations in Fund Accounting: Fund accounting is an accounting system for recording resources whose use has been limited by the donor, grant authority, governing agency, or other individuals or organisations or by law. It emphasizes accountability rather than profitability, and is used by Nonprofit organizations and by governments.

2. Accountability Over Profitability: Business accountability means that you are focused on achieving your goals and your tasks and ultimately achieving profit. It means limiting distractions interruptions and external pressures to focus on your goals and achieve them efficiently.

3. Reporting and Oversight: financial reporting oversight role means a role in which a person is in a position to or does exercise influence over the contents of the financial statements of the Company or anyone who prepares them, such as when the person is a member of the board of directors or similar management or governing body, chief.

13. X Ltd. made a profit of Rs. 5,00,000 after considering the following items:

| Rs. | |

| (1) Preliminary expenses written off(2) Depreciation on fixed assets(3) Loss on sale of machinery(4) Provision for doubtful debts(5) Gain on sale of Land | 5,00050,00020,00010,0007,500 |

Position of current assets and current liabilities:

| 2017 (Rs.) | 2018 (Rs.) | |

| DebtorsBills ReceivedPrepaid expensesCreditorsBills PayableExpenses Payable | 52,00015,0002,00040,00019,00034,000 | 78,00012,0003,00051,00012,00020,000 |

Calculate cash from operating activities.

Ans: Students Do Yourself.

Or

What is meant by “cash equivalents”? Mention any three objectives of preparing cash flow statement.

Ans: Cash equivalents are the total value of cash on hand that includes items that are similar to cash; cash and cash equivalents must be current assets. A company’s combined cash or cash equivalents is always shown on the top line of the balance sheet since these assets are the most liquid assets.

There are three objectives of preparing cash flow statement here:

1. Operating activities.

2. Investing activities.

3. Financing activities.

1. Operating activities: Operating activities are the functions of a business directly related to providing its goods and/or services to the market. These are the company’s core business activities, such as manufacturing, distributing, marketing, and selling a product or service.

2. Investing activities: Investing activities include purchases of physical assets, investments in securities, or the sale of securities or assets. Negative cash flow from investing activities might not be a bad sign if management is investing in the long-term health of the company.

3. Financing activities: Financing activities are transactions between a business and its lenders and owners to acquire or return resources. In other words, financing activities fund the company, repay lenders, and provide owners with a return on investment. Financing activities include: Issuing and repurchasing equity.

14. Calculate the values of opening and closing stock from the following information:

| Cost of goods soldStock Turnover RatioStock at the beginning is 1.5 time more than the stock at the end | Rs. 2,00,0008 times |

Ans: Students Do Yourself.

Or

What is Ratio Analysis? Mention any three uses of ratio analysis.

Ans: Ratio analysis is a quantitative method of gaining insight into a company’s liquidity, operational efficiency, and profitability by studying its financial statements such as the balance sheet and income statement. Ratio analysis is a cornerstone of fundamental equity analysis.

Uses of Ratio Analysis:

1. Comparisons: One of the uses of ratio analysis is to compare a company’s financial performance to similar firms in the industry to understand the company’s position in the market.

2. Trend line: Companies can also use ratios to see if there is a trend in financial performance. Established companies collect data from the financial statements over a large number of reporting periods.

3. Operational efficiency: The management of a company can also use financial ratio analysis to determine the degree of efficiency in the management of assets and liabilities.

15. Ram, Shyam and Mohan were in partnership sharing profits and losses in the ratio of 3:2:1. On 31/12/2018 Shyam retired from the firm, Balance Sheet of the firm on that date was as under:

Balance Sheet

| Liabilities | Rs. | Assets | Rs. |

| Sundry CreditorsReserveBills PayableCapital:Ram 20,000Shyam 15,000Mohan 12,000 | 5,0006,0002,600 47,000 | CashDebtors 15,000Less: Provision 1,500StockFurnitureMachinery | 600 13,50018,5008,00020,000 |

| 60,600 | 60,600 |

The terms of retirement were:

(1) Goodwill of the firm to be valued at Rs. 12,000.

(2) Machinery to be appreciated by Rs. 5,000.

(3) Furniture to be depreciated by Rs. 1,000.

(4) Provision for bad debts to be increased by Rs. 400.

Prepare Revaluation A/c and Partners’ Capital A/c.

Ans: Students Do Yourself.

Or

What is share? Explain different types of shares.

Ans: A share represents a unit of equity ownership in a company. Shareholders are entitled to any profits that the company may earn in the form of dividends.

The different types of shares in a limited company?

- Ordinary shares.

- Non-voting shares.

- Preference shares.

- Redeemable shares.

1. Ordinary shares: These are the most common class of shares that Australian companies issue. They generally give the shareholder the right to attend meetings, vote and receive dividends. This class of shares generally do not carry any special or preferred rights over other shareholders.

2. Non-voting shares: A non-voting share is a share in the capital of a company that belongs to a class that has no voting rights. This is distinct from, for example, an ordinary share which gives the shareholder standard rights to vote at shareholder meetings in proportion to their shareholding. Upon issuing shares to a shareholder, the subscription documents and share certificate will specify the class of shares.

3. Preference shares: As the name suggests, these shares have preferential rights attached to them. Preference shareholders will often have priority over ordinary shareholders to receive dividends and distributions of the company’s assets on winding up.

4. Redeemable shares: Redeemable shares in a private company may be redeemed out of distributable profits, the proceeds of a fresh issue of shares made for the purposes of the redemption, or out of capital. Where shares are redeemed, they are treated as cancelled and the amount of the company’s issued share capital is lowered by the nominal value of the shares redeemed.

16. What is Profit and Loss Appropriation A/c? Why is it prepared?

Ans: It is prepared to provide a clear picture of how the profits or losses are distributed among the partners of the firm. The main purpose of profit and loss appropriation is to show the allocation and distribution of Net Profit among the partners, reserves, and dividends.

Profit and Loss Appropriation A/c prepared Because

1. While preparing the final accounts of a partnership firm it is preferable to ascertain the net profit of the firm before any personal adjustments of the partners are adjusted.

2. This will show separate results for the business activities and facilitate comparisons year after year.

All adjustments like partner’s salary, commission, bonus, interest on capital, loans, drawings, and sharing of profits are passes through a separate account called Profit & Loss Appropriation Account.

3. Thus, the profit and loss Appropriation account are prepared to show how net profit is distributed among the partners.

Or

Ajoy, Bijoy and Sanjay were partners in a firm sharing profits in the ratio of 3 : 2 : 1. On 31st March, 2019 their Balance Sheet was as under:

Balance Sheet

| Liabilities | Rs. | Assets | Rs. |

| CreditorsReserveCapital:Ajoy 24,000Bijoy 12,000Sanjay 8,000 | 4,0006,000 44,000 | BuildingMachineryStockDebtorsCash at Bank | 20,00016,0005,1006,0006,900 |

| 54,000 | 54,000 |

Ajoy died on 30/09/2019. Under the partnership agreement the executors of a deceased partner were entitled to:

(a) Amount standing to the credit of Partners’ Capital account.

(b) Interest on Capital @ 12% p.a.

(c) Share of goodwill on the basis of 4 years purchase of last 3 years average profits.

(d) Share of profit from the closing of the last financial year to the date of death on the basis of last year’s profit.

(e) Profit for the last three years were:

| Year | Profit |

| 2016-172017-182018-19 | 8,000 /-12,000 /-7,000 /- |

Prepare Ajoy’s Capital A/c on the date of his death.

Ans: Students Do Yourself.

17. What is dissolution of partnership? How does it differ from dissolution of firm?

Ans: A Partnership is an association of two or more people to conduct business. A Partnership is a relation between persons who agreed to share the profits of a business carried on by all or any of them acting for all. Partners are someone who is associated with another in a common activity or interest, like a business or partnership law member. Partners are the persons who have entered into a partnership individually. A firm is a business partnership; the name under which it trades. Dissolution of a firm or partnership is disintegration or going into solution. Dissolution is to break the continuity of, to separate, to repel.

Dissolution of a Firm means termination of the firm and end of business relationship among all the partners. Dissolution of Partnership means there is a change in the business relationship among all the partners and the firm continues to run.

Or

Dipali and Rajshri were partners in a firm sharing profits and losses in the ratio of 3 : 2. They decided to dissolve their firm on 31st December, 2019, when their Balance Sheet was as under:

Balance Sheet

| Liabilities | Rs. | Assets | Rs. |

| Capital:Dipali 18,400Rajshri 10,600Sundry Creditors | 29,0002,000 | LandInvestmentsSundry DebtorsStockCash at Bank | 16,0004,0002,0003,0006,000 |

| 31,000 | 31,000 |

Investments are sold at Rs. 3,800. Other assets realised as follows:

(a) Land Rs. 28,000, Sundry Debtors Rs. 1,800, Stock Rs. 2,800.

(b) Creditors agreed to accept 5% less. Expenses of realisation amounted to Rs. 400.

Prepare Realisation A/c, Partners’ Capital A/c and Bank A/c.

Ans: Students Do Yourself.

18. Explain the following terms: (any two)

(1) Calls-in-advance.

(2) Under Subscription.

(3) Pro-rata allotment of shares.

Ans: (1) Calls-in-advance: Calls in Advance is just opposite to Calls in Arrear. It is a situation when the shareholders of a company pay the amount not yet called upon his shares. In other words, Calls in Advance is the amount of future calls which is received by the company in advance.

(2) Under Subscription: “Undersubscribed” refers to a situation in which the demand for an issue of securities such as an initial public offering (IPO) or another offering of securities is less than the number of shares issued.

(3) Pro-rata allotment of shares: Pro-rata allotment refers to the allotment of shares in proportion of the shares applied for. When a company makes pro-rata allotment, it adjusts the excess money received at the time of application firstly, towards the allotment and then towards calls.

Or

Prepare a common size Income Statement from the following information:

| (Rs.) | |

| SalesCost of Goods SoldOperating ExpensesDepreciationIncome from InvestmentIncome Tax | 5,00,0003,78,00062,50022,00070,00032,500 |

Ans: Students Do Yourself.

19. Nanu and Manu are partners of a firm. The Trial Balance of the firm as on 31st March, 2019 was as under:

Trial Balance

| Debit | Rs. | Credit | Rs. |

| Plant and MachineryGoodwillSundry DebtorsClosing StockSalariesDepreciation on Plant and MachineryStationeryInsuranceCash in handInvestmentDrawings:Nanu 4,000Manu 2,000 | 50,0005,00031,00020,0007,0005,0001,0002,0001,00010,000 6,000 | Capital:Nanu 40,000Manu 30,000Sundry CreditorsCommissionSundry ReceiptsOutstanding wagesInterest on InvestmentTrading A/c:Gross ProfitBank Loan | 70,00010,0003,000200600200 50,0004,000 |

| 1,38,000 | 1,38,000 |

Prepare Profit and Loss A/c, Profit and Loss Appropriation A/c, and the Balance Sheet of the firm for the year ended 31st March, 2019, after considering the following information:

(1) Write off of Rs. 1,000 as bad debt and provide 5% provision for doubtful debts on remaining debts.

(2) Commission received in advance Rs. 500.

(3) Transfer 10% of Net Profit to General Reserve.

(4) Allow Interest on Capital @ 5% p.a.

Ans: Students Do Yourself.

20. Bijoya Ltd. issued 2,000 shares of Rs. 100 each at par, payable as follows:

| On ApplicationOn AllotmentOn First CallOn Final Call | Rs. 30Rs. 30Rs. 20Rs. 20 |

All the shares were duly subscribed for, call-up and paid-up, except the following:

(a) Arnab holding 100 shares failed to pay first call and final call money.

(b) Ayushi holding 60 shares failed to pay the final money.

All the above shares were forfeited after final call.

Give journal entries in the books of the company to record the above transactions.

Ans: Students Do Yourself.

Or

(a) Mention three differences between shares and debentures.

(b) Mention three uses of securities premium.

(c) What is Authorised Capital of a company?

Ans: (a) 1. Share or Share Capital is a company’s owned capital while a Debenture is its obligation to the debt provider or creditor.

2. When going public to the investors, the issue of shares is compulsory while the issue of debentures is optional.

3. Shares provide an entitlement towards the dividend rights to their owners while debentures provide an entitlement towards the interest payment component.

4. Debenture holders do not have any management rights like shareholders because they are a creditor to the company while shareholders are owners of the capital with voting rights.

5. Convertible debentures allow the owner to convert into shares or other forms of ownership capital while this conversion option is not with a shareholder.

6. One can find the shareholder’s fund in the balance sheet under the shareholder’s fund section. On the other hand, debentures are listed in the non-current liabilities section stated under long-term liabilities.

(b) Securities premium can be used for these activities:

1. Issuing fully paid up bonus shares to existing shareholders.

2. Writing off expense of issue of shares and debentures, such as discount given on issue of shares.

3. Writing off preliminary expenses.

4. Buying back shares.

5. For paying premium payable on redemption of debentures.

(c) Authorized share capital—also known as “authorized stock,” “authorized shares,” or “authorized capital stock”—refers to the maximum number of shares a company is legally allowed to issue or offer based on its corporate charter.

21. Give journal entries in the books of PM Ltd. relating to issue of debentures under the following conditions:

(a) 120, 8% Debentures of Rs. 1,000 each issued at a discount of 5% and redeemable at par.

(b) 150, 8% Debentures of Rs. 1,000 each issued at 5% discount and redeemable at 10% premium.

(c) 200, 7% Debentures of Rs. 100 each, issued at a premium of 5% and redeemable at 10% premium.

Ans: Students Do Yourself.

Or

Explain different methods of redemption of debentures.

Ans: Redemption Reserve Methods: Debentures can be redeemed in several different ways. For bookkeeping purposes, each approach is handled differently. It is possible to place these methods into the following buckets:

Lump-sum Method: After the maturity term, the corporation will make a single redemption payment in full to the holder of the debenture. The principal amount and maturity date will be agreed upon during debenture issuance. Since the corporation knows the maturity date, it can plan accordingly. In addition, this debenture amount received in lump sum includes the cash held in the debenture’s redemption reserve account.

Instalment Method: In this form of debenture redemption, the borrowed funds are repaid in a series of payments, either regularly or irregularly, depending on the rescue of the debenture above.

Purchasing Method: Market participants are eager to buy the debentures these corporations and organisations issued. They may also be terminated instantly, allowing the corporation to extend the debenture’s term until its repayment is within its means.

In addition, the corporation may increase its income by purchasing debentures on the open market at a discount, which reduces the total redemption payment.

Conversion Method: Conversion to a different debenture or stock in the issuing firm is an additional perk of redeemable debentures. As part of the debenture’s issuing process, the holder is informed of the terms and circumstances under which the debenture may be converted.

Convertible debentures are the word used to describe this kind of debt instrument. At par, at a discount, or at a specified premium, the company can issue new equity shares in exchange for such debentures or issue new debentures.

22. Jugal and Govind are partners in a firm sharing profits and losses in the ratio 2:1. Their Balance Sheet as on 1st June, 2019 was as under:

Balance Sheet

| Liabilities | Rs. | Assets | Rs. |

| Capital:Jugal 30,000Govind 24,000ReserveSundry CreditorsBills Payable | 54,0006,00012,0003,000 | GoodwillSundry AssetsCash at Bank | 12,00057,0006,000 |

| 75,000 | 75,000 |

On the date Khirod was admitted as a new partner. He paid Rs. 30,000 towards his capital but unable to pay anything for goodwill in cash. It was agreed that goodwill will be valued at Rs. 21,000. The new profit sharing ratio among Jugal, Govind and Khirod was agreed at 3 : 2 : 1 respectively.

Pass Journal Entries to record the above transactions and show the Balance Sheet of the new firm.

Ans: Students Do Yourself.

Or

(1) Mention any three features of partnership business.

Ans: The following are the three characteristics of a partnership:

- Sharing of profits and losses.

- Mutual agency.

- Unlimited liability.

(2) Mention five distinctions between “Fixed” and ‘Fluctuating” Capital.

Ans:

| Basis | Fixed Capital Account | Fluctuating Capital Account |

| 1. No. of Accounts Maintained | Two Accounts are maintained for each partner 1. Partners Current Account & Partners Capital Account | Only single account is maintained for each partner i.e. Partners Capital Account |

| 2. Frequency of Change | Closing Balance of Fixed Capital Account does not change until additional capital or withdrawn out of capital is not practiced. Closing Balance of Partners Current account changes every year. | Closing Balance of Partners capital account changes every year. |

| 3. Transferring the Transactions | Transactions relating to additional capital and withdrawal out of capital are recorded in Capital Account. regular transactions such interest on capital, interest on drawings, partners salary, commission and distribution of profit and losses are shown in current account of partners. | All transactions are shown in partners capital account. no current account is maintained here. |

| 4. Balance | Capital account always show credit balance. current may show credit or debit balance. | capital account may show credit or debit balance. |

Hi! my Name is Parimal Roy. I have completed my Bachelor’s degree in Philosophy (B.A.) from Silapathar General College. Currently, I am working as an HR Manager at Dev Library. It is a website that provides study materials for students from Class 3 to 12, including SCERT and NCERT notes. It also offers resources for BA, B.Com, B.Sc, and Computer Science, along with postgraduate notes. Besides study materials, the website has novels, eBooks, health and finance articles, biographies, quotes, and more.