Class 12 Business Study Chapter 8 Controlling Question answer to each chapter is provided in the list so that you can easily browse through different chapters HS 2nd Year Business Study Notes, Class 12 Business Study Chapter 8 Controlling, Class 12 Business Study Question Answer In English Notes and select needs one.

Class 12 Business Study Chapter 8 Controlling

Also, you can read the SCERT book Notes Class 12 Business Study Chapter 8 Controlling online in these sections Solutions by Expert Teachers as per SCERT Class 12 Business Study Chapter 8 Controlling (CBSE) Book guidelines. These solutions are part of SCERT All Subject Solutions. Here we have given Assam Board Class 12 Business Study Chapter 8 Controlling Solutions for All Subjects, You can practice these here Class 12 Business Study Chapter 8 Controlling.

Controlling

Chapter: 8

PART – A

VERY SHORT TYPE QUESTIONS ANSWERS (1 MARK EACH)

1. What is meant by controlling ?

Ans: Controlling is the process of checking whether the plans are being adhered to or not, keeping a record of progress and the corrective measures if there is any direction en taking

2. An efficient control system helps to accomplish organisation objectives only. [Correct/ Incorrect]

Ans: Incorrect.

3. Morale of employees can be achieved through an effective control system. [Correct/Incorrect]

Ans: Correct.

4. The controlling function of an organisation is forward looking or backward looking. Write appropriate word.

Ans: Controlling function is both forward as well as backward looking.

5. Control system can judge accuracy of standard. [Correct/ Incorrect]

Ans: Correct.

6. Give meaning of the term, “Deviation used in Management.”

Ans: Deviation is the difference between actual performance and standard performance.

7. Management audit is a technique to check on the performance of company. Do you agree ? Give reasons.

Ans: Yes, management audit is a systematic appraisal of the managerial performance of an organisation. It identifies the deficiencies of managerial performance.

8. Does budgeting control require the preparation of budget ? Give reason.

Ans: Yes, budgetary control involves the use of budgets to plan, coordinate and control the day-to-day operations of business in accordance with its overall objectives.

9. Is controlling “The End of Management Cycle” ? Give reason.

Ans: No, controlling is not the end of management cycle because in the process of controlling we find out deviations which gives way to us for further action for which we need to do the planning.

10. What is critical point of control ?

Ans: Key areas that are critical for the success of an organisation should be the focus of control.

11. Name the function which reviews the operations in a business unit.

Ans: Controlling function.

12. Name the two situations in which corrective action is not required.

Ans: (i) Zero Deviation.

(ii) Positive Deviation.

13. What is budgetary control ?

Ans: Same as Q.No 34.

14. Name any one type of budget.

Ans: Sales Budget.

15. What is feedback in controlling ?

Ans: Report of happening of event or performance by individuals and groups.

16. Name any one modern technique of management control.

Ans Management Information system (MIS)

B. SHORT TYPE QUESTIONS ANSWERS TYPE-I (3 MARKS EACH)

17. Which two steps in the process of control are concerned with compelling events to conform to the plan.

Ans: The two steps in the process of control that are concerned with compelling events to conform to the plan are given below :

(i) Setting standards of performance: Every enterprise plan its activities in advance. On the basis of these plans the objectives and goals of every department, branch etc. are fixed. The goals are converted into quantity, value, man hour etc. These are to be achieved in future. The standard for measuring the results of a particular work as satisfactory average or poor should be predetermined so that the person responsible for, should be able to assess their performance.

(it) Comparing actual performance with standards: This step involves appraisal of performance i.e., comparison of actual performance with the standards laid down at the first stage. The process of appraisal will reveal deviations from the standards. The manager should analyse the various deviations and investigation into their causes.

18. Break even analysis shows the performance of an organisation. Explain in brief.

Ans: Break even analysis is a process of identifying the break-even point, where there is neither profit or loss. It is the study of relationship between costs, volume and profits, it determines the probable profit and losses at different levels of activity. So, with the help of break even analysis the performance of an organisation can be found.

19. Control is an indispensable function of management. Give reasons. Why corrective measures are taken in controlling.

Ans: Controlling is an indispensable function of management Without control, a manager cannot complete his job. All other managerial functions may prove to be futile activities if there is no control in. the enterprise. It is controlling that makes sure that there is proper execution of these function to attain the objective of the enterprise. Corrective measure are taken when there is deviation. If the performance is not satisfactory corrective measures are taken.

20. What are the techniques of Management Control ?

Ans: Modern business enterprises use a large number of techniques of managerial control.

These may be grouped into two categories as follows:

(i) Traditional or conventional techniques such as personal. observation, statistical reports, break-even analysis, budgetary control etc.

(ii) Modern or contemporary techniques such as – Rate of Return on Investment (ROI), Ratio Analysis, Responsibility Accounting, Management Audit, PERT, CPM and Management Information System.

C. SHORT TYPE QUESTIONS ANSWERS TYPE II (4 MARKS EACH)

21. “Controlling is an indispensable function of management”. Do you agree ? Give four reasons in support of your answer.

Ans: Yes, I agree with the statement, controlling is a necessary function of management because of the following reasons –

(i) Efficient Use of Resources: Each activity is performed in accordance with predetermined standards. As a result there is better use of resources and wastages and inefficiencies are reduced.

(ii) Judging Accuracy of Standards: Through controlling, a manager can judge whether the standards or targets set are accurate or not.

(iii) Better Result: It brings out the shortcomings of planning, organising, staffing and directing and helps in taking corrective action to improve the performance of these functions.

(iv) Coordination of Activities: Control facilitates coordination of the activities of various units. It integrates the complex activities of the various departments of the enterprise. It provides unity of direction to all the departments.

(v) Ensuring Order and Discipline: Controlling insists on continuous check on the employees and thus creates an atmosphere of order and discipline.

(vi) Decision-making: Control facilitates decision-making. The process of control is complete only when corrective measures have been taken.

22. “Controlling is a systematic process involving series of steps”. State the steps involved in the process.

Ans: Same as Q.No 30.

23. Explain four features of a good control system.

Ans: (i) Clear-cut Objectives: Before planning a control system, it is essential to know clearly the objectives it will tend to achieve. The standards of performance should be based on these objectives.

(ii) Simplicity: A good system of control should be simple and easy to understand. The employees must know what is expected of them and how their performance will be evaluated.

(iii) Forward Looking: The system of control should be forward looking in the sense that it should detect and report deviations promptly. Timely action is the essence of control.

(iv) Corrective Action: Merely pointing out deviations is not sufficient in a good control system. It must lead to taking of corrective action to achieve the desired objectives.

24. “Controlling is a systematic process involving a series of steps”. Explain.

Ans: Same as Q.No 40.

25. Explain in brief the importance of controlling.

Ans: The following importance of controlling are described below:

(i) Efficient use of resources: Each activity is performed in accordance with predetermined standards. As a result there is better use of resources and wastages and inefficiencies are reduced.

(ii) Judging accuracy of standards: Through controlling a manager can judge whether the standards or targets are accurate or not.

(iii) Better results: Controlling brings out the shortcomings of planning. organising, staffing and directing helps in taking corrective action to improve the performance of these functions.

(v) Ensuring order and discipline: Controlling insists on continuous check on the employees and these create an atmosphere of order and discipline.

26. What is Critical Path Method (CPM) ?

Ans: Critical Path Method is basically a technique of project management, which is useful in planning, scheduling and controlling. The planning of any project involves the listing of various jobs that have to be performed to complete the venture. Requirements of man, materials and equipment are drawn up along with the estimates of costs and durations for the various jobs, in the process of planning. CPM are used in construction of ships, buildings and highways, in the planning and launching of new products, in the publication of books, in the installation and debugging of computer systems.

27. What is Programme Evaluation and Review Technique (PERT)

Ans: Programme Evaluation and Review Technique (PERT) is a basic network which includes planning, monitoring and controlling of a project.

It addition to its use in schedule planning and control the network concept in PERT provides the framework for treating a wide range of project management problems.

The steps in PERT are as follows:

(i) Identify the component activities that must be performed.

(ii) Show the sequencing of the component activities in a network.

(iii) Perform an analysis of the time required to complete individual activities and the entire project.

(iv) Improve upon the initial plan through modifications.

(v) Control the project.

28. Explain in brief Return on Investment. (ROI)

Ans: Rate of Return on Investment (ROI) is regarded as a useful technique of control to evaluate the success of a business enterprise. It determines the ratio of earnings of the enterprise to its investment. That is why, it is also called return on capital employed. The essence of this approach is that profit is not taken as an absolute figure, but is considered in relation to the invested capital. This helps in comparing the rate of return of two companies whose profit figures and capital investment are different.

Rate of return on investment can be calculated by the following

formula: ROI= E/I

Where, E stands for net earnings and I stands for investment (i.e. capital and free reserves)

29. What is Ratio analysis ?

Ans: Ratio analysis means the analysis of financial statements through computation of ratios.

Some of the important ratios are as follows:

(i) Liquidity ratio: Such ratios are calculated to determine short term solvency of business. Analysis of current position of liquid funds determines the ability of the business to pay the amount due to its stakeholders.

(ii) Solvency ratios: Such ratios are calculated to determine the long term solvency or business. They determine the ability of a business to service its indebtedness.

(iii) Profitability ratios: Such ratios are calculated to analyse the profitability position of a business in relation to. sales, or funds or capital employed.

(iv) Turnover ratios: Turnover ratios are calculated to determine the efficiency of operations based on effective utilisation of resources.

30. Why information system is important in Business ?

Ans: Information system is a system designed to supply information required for effective management of an organisation. Management Information’s System (MIS) is important to supply information required for effective management of the organisation.

It is also important for the following purpose:

(i) It provides right information to all the managers at different levels.

(ii) It provides the required information in a cost effective manner.

(iii) It provides the quality of information provided to the managers.

(iv) It helps in planning, controlling and decision making.

31. What is management by exception ?

Ans: Management by Exception (MBE) is an important principle of management control. According to this principle, only significant deviations from the standards require management’s attention as they constitute exceptions. This principle implies that minor deviations from the standards may be ignored or given less attention. This would conserve managerial time, effort and energy which could be utilised on important matters. But wherever deviations from standards are higher than the accepted level, management must take corrective measures to deal with the situation.

32. What are the different types of Budgets ?

Ans: The different types of budgeting are described bellows:

(i) Sales Budget: It includes a forecast of total sales during a specified period (say one year) expressed in money or quantities.

(ii) Cash Budget: The cash budget usually gives detailed estimates of cash receipts and cash available in time for meeting the financial commitments.

(iii) Production Budget: It includes a forecast of the output during a particular period analysed according to-

(a) products.

(b) manufacturing departments. and

(c) periods of production.

(iv) Material Budget: It generally deals with the direct materials for the budgeted output. It is based on the production budget. Materials requirement for a unit of production is determined and is multiplied by the budgeted output to arrive at the total quantity of direct materials required.

(v) Labour Budget: It reveals the requirements of labour financial requirements to meet the wage bill of workers for the and the budget period.

(vi) Master Budget: Master budget incorporates all financial budgets. It projects a comprehensive picture of the proposed activities and anticipated results during the budget period.

D. LONG TYPE QUESTIONS ANSWERS TYPE – I (6 MARKS EACH)

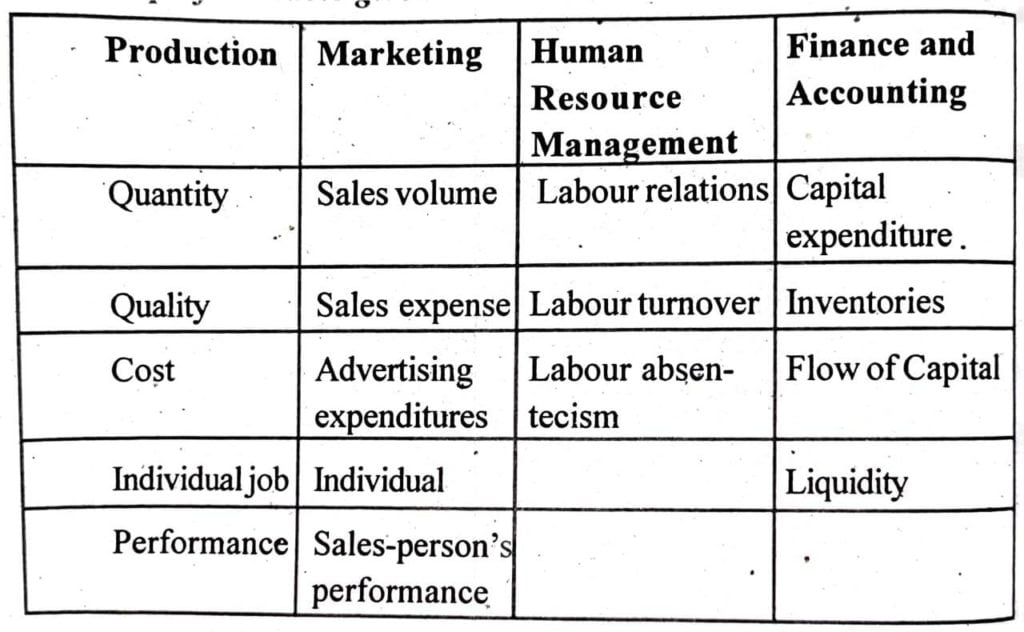

33. Explain the standards used in functional area.

Ans: Standards are the criteria against which actual performance would be measured. Thus, standard serve as benchmarks toward which an organisation strives to work. Standards can be set up in both quantitative as well as qualitative terms. For instance, standards. set in terms of cost to be incurred, revenue to be earned, product units to be produced and sold, time to be spent in performing a task the all represent quantitative standards.

Standards used in functional areas can be highlighted with the help of the table given below:

34. What is Budgetary control. Explain.

Ans: Budgetary control is the oldest technique of control which is still being used by business enterprise. Budgetary control involves the use of budgets to plan, coordinate, and control the day to day operations of business in accordance with its overall objectives. According to Walter W. Bigg, “Budgetary control is a system of management and accounting control by which all operations and output are forecast as far ahead as possible and the actual results, when known, are compared with the budget estimates.”

35. Explain the relationship between planning and controlling.

Ans: The relationship between planning and controlling can discussed as follows:

(i) Planning originates controlling: In planning the objectives or targets of the organisation are set. In order to achieve these objectives control process is needed. So planning proceeds control.

(ii) Controlling sustains planning: Controlling directs the course of planning. Controlling find out the areas where planning is required. Controlling provides information for planning: In controlling the actual performance is compared to the standards set and records the deviation if any. The information collected for exercising control is used for planning also.

(iv) Planning and controlling is integrated: Planning is the first function of management. Control records the actual performance and compares with standards set. In case the performance is less than standards corrective measures are taken to improve. Planning is the first and control is the last function. Both are dependent upon each other.

(v) Planning and controlling are forward looking: Planning and control are concerned with the future activities of the business. Planning is always for future and control is also forward looking. No one can control the past, it is the future which can be controlled.

36. Management can achieve the goal in implementing an effective control system.

Ans: The control function helps the management in different shapes. It guides the management in achieving its predetermined goals.

The importance of controlling in the management of an organisation may be explained as follows:

(i) Basis for future action: Control provides basis for future action. The continuous flow of information about project keeps the long range planning on right track. It helps in taking corrective measures in future, if the performance is not upto to the mark.

(ii) Facilitates decision-making: Whenever there is any deviation between the standard set for and actual performance the control will help in deciding the future course of action.

(iii) Efficient use of resources: Each activity is performed in accordance with predetermined standards. As a result there is better use of resources and wastages and inefficiencies are reduced.

(iv) Employee morale: Controlling can help in building high morale of the employees if it leads to increase in efficiency of workers and recognition of efficient workers. The control system should facilitate higher wages and other benefits to the efficient workers.

(v) Contribution to organisational goals: Control helps in achieving business objectives. Control helps to ensure the regular supply of factors of production and high quality of goods and services at economical costs. This is how it helps in achieving business objectives of profits through high quality goods and services.

37. “An effort to control everything may end up in controlling nothing.” Elucidate the statement.

Ans: An effort to control should be given from the initial stage of the activity. Controlling provides direction to all activities and efforts for achieving organisational goals. Each department and employees. is governed by predetermined standards which are well co ordinated with one another. This ensures that overall organisational objectives are accomplished. Controlling functions measures progress towards the organisational goals and bring to light the deviations if any then it indicates corrective action. It thus, guides the organisation and keeps it on the right track. So, an effort to control should be given from the initial stage of the activity. Because if control is done in the ending of the activity, then some serious mistake cannot be removed and solved. So, the principle control is that it should be started from initial stage of every function.

38. “Break even analysis is a technique used by the managers to study the relationship between cost, volume and profit.” Elucidate the statement.

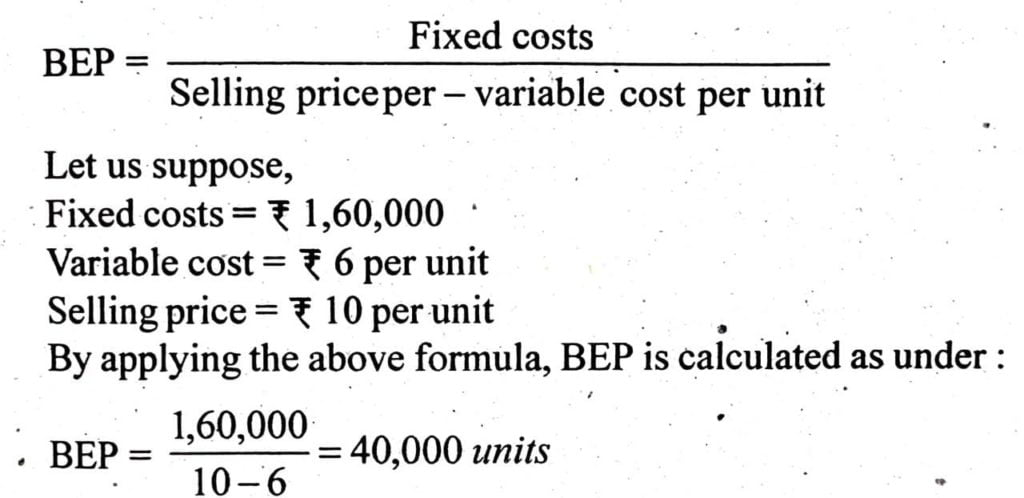

Ans: Break-even analysis is concerned with the effect which changes in fixed costs, variable costs, sales volume, sales prices and sales mix will have on profits. In other words, it establishes relationship between cost of production, volume of production, profits and sales. This analysis helps in determining the volume of sales at which total cost will be fully covered and beyond which profits will occur. The volume of sale at which there is no profit or loss is known as ‘break-even point.”

Break-even point (BEP) can be calculated by the following formula:

39. Responsibility of Accounting is an important, Test of Controlling.

Ans : Responsibility accounting is a system of accounting in which costs and revenues are identified with persons assigned to their control rather than with products or functions. It classifies costs and revenue according to the responsibility centres that are responsible for incurring the cost and generating the revenues. It also classifies the cost assigned to each responsibility centre according to weather they are controllable or non-controllable. Controllable costs are classified by items. The aims is to show the results of operation by each section or division having control over resources and their use.

A responsibility centre is an organisational unit such as division, department or section headed by a manager who is responsible for specified targets. In a cost centre, financial performance is measured by the degree to which assigned tasks are accomplished within the budgeted amount to expense.

LONG TYPE QUESTIONS ANSWERS TYPE-11 (6/8 MARKS EACH)

40. Explain the various steps involved in the process of control.

Ans: The steps in controlling process are classified into four categories which are as follows:

(a) Setting standards of performance.

(b) Measurement of actual performance.

(c) Comparison of actual with standard performance.

(d) Analysing deviations.

(e) Taking corrective action.

(a) Setting standards of performance: Every enterprise plans its activities in advance. On the basis of these plans the objectives and goals of every department, branch etc. are fixed. The goals are converted into quantity, value, man, hour etc. These are to be achieved in future. Specific persons are made responsible for achievements of the goals. The standard for measuring the results of a particular work as satisfactory average or poor should be pre determined so that the person responsible for should be able to assess their performance.

(b) Measurement of actual performance: This step involves measuring of actual performance of various individual, groups or units for comparing it with the standards. The performance should be measured quantitatively as far as possible and recorded properly so as to avoid any confusion. This would make the task of comparing actual performance with the desired performance or standards quite easier.

(c) Comparing of actual performance with standards: This step involves appraisal of performance i.e, comparison of actual performance with the standards laid down at the first stage. The process of appraisal will reveal deviations from the standards. The manager should analyse the various deviations and investigate into their causes.

(d) Analysing deviations: Deviation refers to the differences between actual performance and planned or standard performance. Once the nature and magnitude of deviations are ascertained, the causes of deviations should be identified. This is necessary for taking appropriate corrective actions.

(e) Taking corrective action: The final step in the process of control is taking corrective actions, if there are deviations. This may involve modification of plans and standards, reorganisation of duties, clarification of standards, etc. It may also necessitate improving the process of selection and training of workers and introducing new techniques of motivation. Thus, controlling may require change in all other managerial functions.

41. Explain the traditional techniques and modern techniques of management control.

Ans: Various techniques of managerial control can be classified into two categories.

Such as:

(a) Traditional Techniques.

(b) Modern Techniques.

(a) Traditional Techniques: Under traditional techniques following techniques can be discussed

(i) Personal Observation: It is the technique of collecting first hand information. It creates a psychological pressure on the employees. to perform well as they are aware that they are being observed personally on their job.

(ii) Statistical Reports: Various important organisational data aid information are presented in the form of charts, graphs, tables etc. which help managers to compare these standard with their actual performance.

(iii) Break-even Analysis: Break-even analysis is a process of identifying the break-even point, where there is neither profit or loss. It is a study of relationship between costs, volume and profits. It determines the probable profit and losses at different levels of activity.

(iv) Budgetary Control: Under budgetary control all operations are planned in advance in the form of budget. Thereafter, actual results are compared with budgetary standards. On the basis of budget. necessary action can be taken to accomplish the organisational goals.

(b) Modern Techniques: Following are the modern techniques of control.

(i) Return on Investment: Return on investment is techniques which can be used effectively for generating reasonable amount of return.

Following are the formula of calculating ROI.

(ii) Ratio Analysis: Ratio analysis implies the analysis of financial statements through computation of ratios. Various ratios are

(i) liquidity ratio.

(ii) solvency ratios.

(iii) profitability ratios.

(iv) Turnover ratios.

Current and quick ratio are under liquidity ratio. Debt equity proprietary, investment coverage ratios are under solvency ratio. Gross profit, net profit and return on capital employed ratios are under profitability ratio. Inventory turnover, stock turnover, debtors turnover ratios are under turnover ratios.

(iii) Responsibility Accounting: It is a system of accounting in which different sections, divisions and departments of an organisation are set up as “Responsibility Centres”. The head of the centre is responsible for achieving the target set for him centre.

(iv) Management Audit: Management audit is a systematic appraisal of the managerial performance of an organisation. It identifies the deficiencies of managerial performance. So, it is an evaluation of the functioning performance and effectiveness of management of an organisation.

(v) PERT and CPM: PERT (Programme Evaluation and Review Technique) and CPM (Critical Path Method) are network techniques useful in planning and controlling. These techniques are especially useful for planning, scheduling and implementing time bound projects involving performance of a variety of complex, diverse and interrelated activities.

(vi) Management Information System: MIS is a computer based information system that provides information and support for effective managerial decision making. MIS provides the necessary information to management as per requirement of the top level manager for taking managerial decisions.

42. What are the limitations of controlling? Explain.

Ans: Limitations of controlling or problems faced by the organisation in implementing an effective control system are as follows:

(i) Difficulty in setting quantitative standards: Practically it is difficult task to set quantitative standards because everything cannot be impressed in quantitative terms This creates difficulties in manning the standard.

(ii) Little control on external factors: There are some external factors such as political, legal, social market, etc. which cannot be controlled as per desire of the management. So, managerial control system cannot bring these external factor in favour of the business environment.

(iii) Limitations of corrective action: All reasons for deviations cannot be ascertained because of cost and time involved in investigation. Sometimes, within the organisation, minor deviations are by-passed on the ground of practical expediency.

(iv) Costly process: Control is an expensive process because it involves careful investigation into the causes of deviations from the standards. Moreover, it can operates successfully only if it is accepted by the managers and the operative employees.

(v) Resistance from employees: In time of introducing control system, many employees may show various difficulties, which may go against into control. It is matter of fact that no control system can satisfy every employee equally, so multifarious resistance be emerged from the employees also.

(vi) Difficulty in fixing responsibility: It is assumed that every person should be responsible for his action. and he will take corrective But there are a number of deviations for which nobody in particular can be held responsible. It is here that control becomes ineffective.

43. What process is to be taken into consideration in control.

Ans: See Answer to Question No. 40.

44. What are the causes of deviation ? What corrective mea are taken by the management ?

Ans: The causes of deviations of actual performance from stand might be one or more of the following:

(a) External environmental factors e.g. changes in prices or cha in governmental policies regarding raw material allocations, ch in import and export regulation etc. Factors like intense compe or changing social values having a bearing on sale figures are included in the category of external factors.

(b) Internal environmental factors e.g. inadequacy of product facilities, outdated or substandard technology deteriorating relations etc.

(c) Imperfections in planning, like vague objectives, inapprop courses of action etc.

(d) Flows in directing techniques, like lack of free-flo communication, unsuitable leadership style, careless supervi inadequate motivation etc.

(e) Staffing defects, like faulty selection of employees, inapprop placements, lack of or inadequate training programmes etc.

The corrective measures that taken by the management given below:

(a) Betterment of internal environment like ensuring adequate production facilities, acquisition of superior technology, taking for improving human relations etc.

(b) Modifications or improvements in planning like expressing object clearly, more scientific determination of standards, making a choice among alternative course of actions etc.

Organisational restructuring like making the organisational structure more compact through coordination of jobs, replanning span of management striking a better balance between authority and responsibility etc.

Overcoming staffing defects e.g through better selection procedures, careful placements, better organisation of training programmes etc. Betterment of directing techniques e.g. adopting democratic styles of leadership, exercising more careful supervision, insisting on communication feedback or introducing better motivational schemes etc.

45. What is management information system? What are its advantages ?

Ans: Information system is a system designed to supply information required for effective management of an organisation. Management Informations System (MIS) is important to supply information required for effective management of the organisation.

It is also important for the following purpose:

(i) It provides right information to all the managers at different levels.

(ii) It provides the required information in a cost effective manner.

(iii) It provides the quality of information provided to the managers.

(iv) It helps in planning, controlling and decision making.

The advantages of Management Information System are as follows:

(i) It provides right information to all the managers at different levels.

(ii) It provides the required information in a cost effective manner.

(iii) It improves the quality of information provided to the managers.

(iv) It reduces information overload i.e only relevant information is provided to the managers.

(v) It helps in planning, controlling and decision-making.

Hi, I’m Dev Kirtonia, Founder & CEO of Dev Library. A website that provides all SCERT, NCERT 3 to 12, and BA, B.com, B.Sc, and Computer Science with Post Graduate Notes & Suggestions, Novel, eBooks, Biography, Quotes, Study Materials, and more.