Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques Question answer to each chapter is provided in the list so that you can easily browse through different chapters HS 2nd Year Banking Chapter 6 Cheques Collection And Payment Of Cheques Notes and select needs one.

SCERT Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques

Also, you can read the SCERT book online in these sections Solutions by Expert Teachers as per SCERT (CBSE) Book guidelines. These solutions are part of SCERT All Subject Solutions. Here we have given Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques Solutions for All Subjects, You can practice these here.

Cheques Collection And Payment Of Cheques

Chapter: 6

Answer Questions

Q.1. Give an example of material alteration of cheque.

Ans :- Changed of date, Amount, Person, are an example of material alteration of cheque.

Q.2. Who can cross a cheque ?

Ans :- The holder of a cheque can cross a cheque.

B. Short answer question : Type – I

Q.3. How do you cross a Cheque ?

Ans :- A cheque is said to be crossed or crossed cheque when two transverse parallel lines with or without any words are drawn across its face. Crossing may be written, stamped, perforated or printed.

Q.4. What is Post Dated Cheque ?

Ans :- If the drawer or any holder mentions of date on the cheque, which is subsequent to the date on which it is drawn, it is called a post – dated cheque.

Q.5. Who is Collecting Banker ?

Ans :- A bank collects a cheque either as a holder for value or merely as an agent to the holder thereof is called collecting banker.

C. Short answer questions : Type – II

Q.6. Explain the difference between Open and Crossed Cheque .

Ans :- The difference between Open and Crossed cheque are :

Open Cheque :

1. An open cheque is one the payment of which can be made across the counter of the bank.

2. An open cheque which can be presented for payment by holder at the counter of the drawee’s bank.

Crossed Cheque :

1. A cheque is said to be crossed or crossed cheque when two transverse parallel lines with or without any words are drawn across its face.

2. A crossed cheque which can be paid only through a collecting banker.

Q.7. State two differences of Bearer and Order Cheque.

Ans :- The two differences of Bearer and order cheque are as follows :

Bearer Cheque :

1. When a cheque is made payable to a person named in an instrument or to the bearer cheque.

2. A bearer cheque is transferable by mere delivery. Endorsement is not required in case of bearer cheque.

Order Cheque :

1. When the word ‘bearer’ is deleted from the cheque, it becomes an order cheque. An order cheque is made payable to the order of the person named in the instrument or to his order.

2. An order cheque can be transferred by endorsement and delivery.

Q.6. What do you mean by Bearer Cheque?

Ans :- When a cheque is made payable to a person named in the instrument or to the bearer thereof , it is called bearer cheque.

A bearer cheque is transferable by mere delivery. Endorsement is not required in case of bearer cheque.

Q.7. Write a note on the significance of crossing.

Ans :- Following are the significance of crossing of a cheque are :

1. Crossing of a cheque does not affect its negotiability.

2. Crossing of a cheque refers to the instruction to the banker relating to the payment of the cheque.

3. A crossing is the direction to the paying banker that the cheque should be paid only to a banker.

Q.8. What is material alteration of cheque ?

Ans :- A cheque with material alterations make the instrument null and void. Therefore, if a cheque without any apparent but with material alteration is paid by banker he will not get the protection provided by sections 80 and 82 of the Bills of Exchange Act 1882. All alteration is material which in any way alters materially or substantially the operation of the instrument and the liabilities of the parties there to, irrespective of whether or not the change is prejudicial to the payee. Material alterations include the alteration of the date, crossing, place of payment amount and name of the payee.

Material alteration may be in the following forms :

(i) Alteration of date.

(ii) Alteration of place of payment.

(iii) Alteration of amount.

(iv) Alteration in the names of parties.

(v) Alteration of the word ‘bearer’ in place of ‘order’.

(vi) Alteration of Crossing.

According to section 87 of the Negotiable instrument Act, any material alteration of a negotiable instrument renders the same void as against anyone who is a party thereto at the time of making such alteration, and does not consent thereto unless it was made in order to carryout the common intention of the original parties, and any such alteration, if made by an endorsee, discharges his endorser from all liability to him in respect of the consideration there of.”

Q.9. State the duties of a Collecting Banker.

Ans :- The Collection of cheques and bills on behalf of customers is an important function of almost every modern bank because it provides a facility which can hardly be despondent with especially in case of crossed cheques. It is necessary that in preforming these functions bank should be careful, otherwise he may lead himself in difficulties.

Thus the collecting banker has the following duties and responsibilities :

(i) Presentment for payment with a reasonable time :- The collecting bank should collect the cheques sent by the customer with due care and should present it to the drawee bank within a reasonable time.

(ii) Agent for Collection :- If the cheque is drawn on a place where the banker is not a member of the clearing house, he may employ another banker. In such a case, the latter banker becomes a substituted agent.

(iii) Permittance of proceeds to the customers :- Where a cheque is released by a collecting banker, he should pay the proceeds to the customer as soon as practicable in accordance with the customer’s direction, usually, the amount is credited to the customers account.

(iv) General duties :- The following are the general duties of a collecting banker in connection with a cheque :

(a) It is the duty of the collecting banker to accept the cheque from his customers for collection.

(b) It is the duty of the collecting banker to fully verify the ownership right to his customer in respect of the cheque he has accepted for collection.

(c) It is his duty to ask for introductory references of the account of the customer which was opened without introduction.

● Write short notes on :

Q.10. Stale Cheque.

Ans :- Stale cheque also termed as an ‘out of date cheque’. It is the custom of the bankers not to pay cheques which are presented after a certain period has elapsed since the apparent date of their issue. The period varies from banks to banks. In some banks if is 3 months while in case of others it is 6 months. Generally the period of 6 months is more popular when such a cheque is presented for payment, the bankers returns it with the answer ‘out-of-date’.

Q.11. Post Dated Cheque.

Ans :- If the drawer or any holder mentions a date on the cheque, which subsequent to the date on which it is drawn, it is called a postdated cheque. For example, if a cheque is drawn on 27 June 2007 and bears the date of 27 September 2007, the cheque is post dated and it should be honoured by the bankers, not earlier than 27 September 2007.

In case a bankers honours a post-dated cheque, it runs the following risks :

(i) The drawer may countermand the payment before the date mentioned on the cheque and then the banker will not be entitled to debit the customer’s account with the amount of the cheque.

(ii) The drawer may take the banker liable for dishonouring of other cheques on account of insufficiency of funds resulting because of payment of the post-dated cheques.

(iii) In case of insolvency or death of the drawee before the date mentioned on cheque, the banker shall not be entitled to debit the customer’s account, if it has already made payment of the cheque.

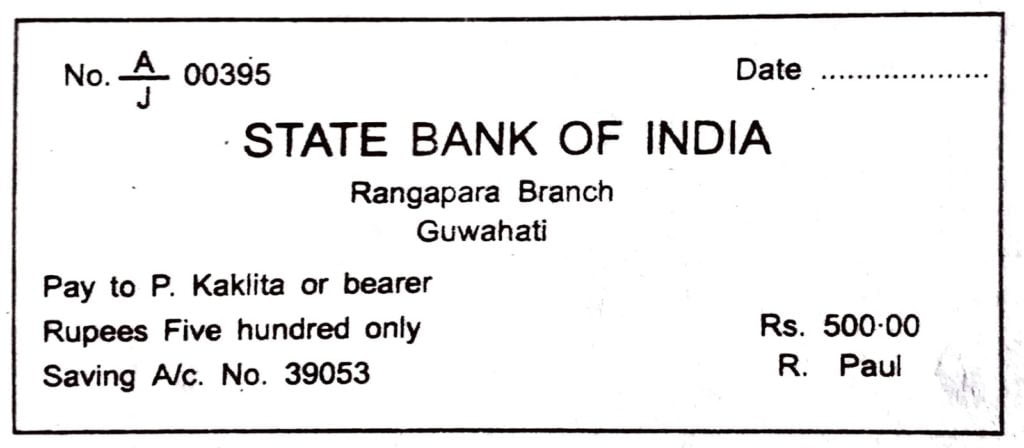

Q.12. Bearer Cheque.

Ans :- In case of a bearer cheque, the paying banker need not seek the identification of the holder of the cheque. An order cheque is paid by the paying banker on being satisfied about the true identity of the presenter of the cheque. However, even in the later case, there is some risk involved.

A bearer cheque is transferable by mere delivery. Endorsement is not required in case of bearer cheques.

The specimen of a bearer cheque are given below :

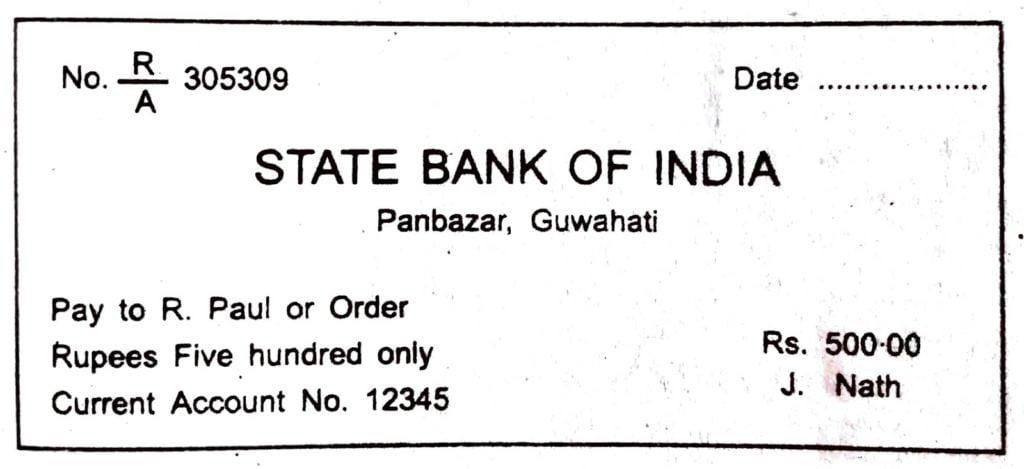

Q.13. Order Cheque.

Ans :- When the word ‘or bearer’ is deleted from the cheque, it becomes an order cheque. An order cheque is made payable to the order of the person named in the instrument or to his order. Such a cheque is paid by the bank only when the banker is satisfied with the identity of the person claiming payment of the cheque. It can be transferred by endorsement and delivery.

Q.14. Material Alteration.

Ans :- A Cheque with Material alterations make the instrument null and void. Therefore, if a cheque without any apparent but with material alteration is paid by a banker, he will not get the protection provided by sections 80 and 82 of the Bills of Exchange Act 1882. Material alterations include the alteration of the date, crossing, Place of payment, amount and name of the payee.

Material alteration may be in the following forms :

(i) Alteration of date.

(ii) Alteration of place of payment.

(iii) Alteration of amount.

(iv) Alteration in the names of parties.

(v) Alteration of the word ‘bearer’ in place of ‘order’.

(vi) Alteration of crossing.

According to section 87 of the Negotiable instrument Act, any material alteration of a negotiable instrument renders the same void as against anyone who is a party there to at the time of making such alteration, and does not consent thereto unless it was made in order to carryout the common intention of the original parties, and any such alteration, if made by an endorsee, discharges his endorser from all liability to him in respect of the consideration thereof.”

Q.15. Collecting Banker.

Ans :- A bank collects a cheque either as a holder for value or merely as an agent to the holder thereof is called collecting Banker.

The Collecting banker has the following duties and responsibilities :

(a) Presentment for payment with a reasonable time :- The bank should collect the cheques sent by the customers with due care and should present it to the drawee bank within a reasonable time.

(b) Agent for Collection :- If the cheque is drawn on a place where the banker is not a member of the clearing house, he may employ another banker. In such a case, the latter banker becomes a substituted agent.

(c) Permittance Proceeds to the Customers :- When a cheque is released by a collecting banker he should pay the proceeds to the customer as soon as practicable in accordance with the customer’s direction, usually, the amount is credited to the customer’s account.

Q.16. Paying Banker.

Ans :- The paying banker is defined as the banker to whom the order is made to pay, where the order is issued in the form of cheque. It is the only bank who makes the final settlement of the instrument. It is an obligation of the bank to honour the cheque of the customer if there is sufficient balance in the account.

According to section 31 of Negotiable Instrument Act, 1881, “The drawee of a cheque having sufficient funds of the drawer in his hands, properly applicable to the payment of such cheque, must pay the cheque when duly required to do so and in default of such payment, must compensate the drawer for any loss or damage caused by such default.

Thus a paying banker is statutorily bound to honour the cheque of his customers.

Example :- If Rahul has given Biju crossed cheque of Rs. 10000 of S.B.I., but Biju is not having an account in S.B.I so he deposited the cheque in Rajasthan Bank. Now here Rajasthan bank will be a collecting bank.

S.B.I will be the paying bank. So it is clear that cheques which are perfect in all respect should be honoured and cheques which are not in order should be dishonoured.

Q.17. Holder for value.

Ans :- If the collecting banker pays to the customers the amount of the cheque or credit such amount to his account and allows him to draw it, before the amount of the cheque is actually realised from the drawee banker, the collecting banker is deemed to be its ‘holder for value’.

A banker becomes its holder for value by giving its value to the customer in any of the following ways :

(a) By lending further on the strength of the cheque.

(b) By paying over the amount of the cheque or part of it in cash or in account before it is cleared.

(c) By accepting the cheque in avowed reduction of an existing overdraft ; and

(d) By giving cash over the counter for the cheque at the time it is paid in for collection.

Q.18. Double special crossing.

Ans :- The banker to wham the cheque is crossed specially may again cross it specially to another banker his agent for collection. This is called double special crossing.

Q.19. Not Negotiable Crossing.

Ans :- Section 123 and 124 permit that the words ‘not negotiable’ may be included in the general and special crossing respectively. The inclusion of the words ‘not negotiable’ in the crossing has great practical significance. These words do not make the cheque non-transferable but their inclusion in the crossing takes away one of the important characteristics of a negotiable instrument.

Section 130 States :

A person taking a cheque crossed generally or specially, bearing in either case the words, ‘not negotiable’ shall not have and shall not be capable of giving a better title to the cheque than that which the person from whom he took it had.

The primary objective of ‘not negotiable’ Crossing is to safeguard the interest of the true owner of the cheque. It is in reality a warning to the payee or endorsee or the holder of the cheque to accept it only if he knows the endorser well and is convinced that the later has good title there to.

Q.20. Account Payee Crossing.

Ans :- The words “Account Payee” or “Account Payee only” in the crossing have special significance because they intend to make the cheques more safe. These words constitute an instruction to the collecting banker that he should collect the amount of the cheque for the benefit of the payees account only, i.e., to credit the amount to the account of the payee only and nobody else. ‘Account Payee’ crossing doesn’t restrict transferability of the cheque, which can be endorsed further, but in practice such endorsement shall not prove to be effective because the collecting banker is being directed by drawer to credit the proceeds to the account of the payee only.

Q.21. Forgery of drawers signature.

Ans :- A banker is expected to know the signatures of his customers. The paying banker should carefully ascertain that the cheque bears the genuine signature of the drawer after comparing the same with his specimen signature. The cheque must be signed by the drawer on its face and not on its back. The account holder may change his specimen signature any time and supply to the banker his fresh specimen signature. Banker is bound to accept the new specimen signature with effect from a specified date.

If the signature on the cheque differs from the specimen signature of the drawer or the former is a forged one, the banker must refuse payment of the cheque. Payment of a cheque with the forged signature of the drawer is deemed as payment without the authority of the customer. The paying banker is therefore, not given any protection under the law, if he pays a cheque with the forged signature of the drawer. The banker cannot debit his customer’s account with the amount of the cheques bearing the forged signature of the drawer and will suffer the loss himself.

Q.22. Collecting banker as an agent.

Ans :- A collecting banker acts as an agent of the customer if he credits the latter’s account with the amount of the cheque after the amount is actually realised from the drawee’s banker. Thereafter, the customer is entitled to draw the amount of cheque. The banker thus acts as an agent of the customer and charges from him commission for collecting the amount from the outstation banks.

As an agent of his customer, the collecting banker does not possess title to the cheque better than that of the customer. If the customer has no title thereto, or his title is defective, the collecting banker can not have good title to the cheque. In case the cheque collected by him did not belong to his customer, he will be held liable for “Conversion of Money” i.e. illegally interfering with the rights of the true owner of the cheque unless he can prove that he acted in good faith and without negligence and that the cheque was crossed before it came into his hands.

D. Long Answer questions : Type-I

Q.23. State the duties of a paying Banker.

Ans :- The paying banker should performed the following duties :

(i) Proper from of cheque :- Firstly the banker should sec whether the cheque presented at the counter is the one which he had supplied to the customer, or else he can refuse the payment. If a cheque from supplied to another customer is used the banker may not be justified in refusing payment.

(ii) Date of the cheque :- A cheque should be properly dated. If it is a post-dated cheque, he should not pay the cheque. If it is a stale cheque, he may return the cheque. In case if the cheque bears no date, the banker may return the cheque as he is not sure of its date of issue.

(iii) Language :- A cheque should be drawn in a language to be understood by the banker. If the banker is unable to understand the language, he may refused the payment.

(iv) Crossing :- If the cheque is uncrossed, payment may be made through the counter. If it is a crossed one, he should advice the customer to present the cheque through his account.

(v) Signature :- At the time of opening an account the banker obtains specimen signature of the customer.

(vi) Banking hours :- A banker should pay the money only during banking hours i.e. during the period of time when the public transacts banking business.

(vii) Mutilated cheques :- A mutilated cheque is one torn into pieces. The banker should examine if the material part of the cheque is torn, than he should refuse payment. In case he has doubt about the genuineness of the instrument, he can clarify with the customer.

(viii) Endorsement :- The Banker should sec whether the endorsements are regular. In case of irregular endorsement, cheques should not be paid.

(ix) Amount of the cheque :- The amount of the cheque must be clearly mentioned in words and figures, adding the word ‘only’ or drawing a line after the amount in figures. For example : Rupees thousand only or Rs 1000/-

Q.24. State the liabilities of a Paying Banker.

Ans :- Liabilities of Paying Banker It is he liability of the paying banker to honour the cheques of their customer provided that

(i) There is sufficient balance in the customer account or he has been allowed overdraft facility by the bank.

(ii) It is presented for payment on time and in working day [within 6 months from the date of issue].

(iii) It is written in proper form.

(iv) There is no restriction imposed on payment of cheque neither from the customer nor from the state.

Q.25. Explain the protection available to a paying banker.

Ans :- Following are the protection available under Negotiable instrument Act, 1881 :

1. Protection in case of order cheque : Section 85(1) provides statutory protection to the paying banker in case of an order cheque as per to this section.

“Where a cheque payable to order purports to be endorsed by or on behalf of the payee the drawee is discharged by payment in due course”.

This section great protection to the paying banker if they have made payment to wrong person whose signature does not tally with that of specimen signature. Two conditions must be satisfied for getting protection :

(i) Regular Endorsement

(ii) Payment in due course.

2. Protection in case of bearer cheque : Section 85(2) of Negotiable Instrument Act, 1881 provides statutory Protection to the paying bank in case of bearer cheque as :

“Where a cheque is originally expressed to be payable to bearer, the drawee is discharged by payment in due course to the bearer thereof, not withstanding any endorsement whether in full or in blank appearing thereon, and not withstanding that any such endorsement purports to restrict or exclude further negotiation.”

3. Protection incase of crossed Cheque : Section 128 of Negotiable Instrument Act provides protection to paying bank in case of crossed cheque :

“Whereas the banker on whom a crossed cheque is drawn has paid the same in due course, the banker paying the cheque and drawer there (in case such cheques has come to the hands of the payee) shall be entitled respectively to the same right and placed in the same position if the amount of the cheque has been paid to and received by the true owner thereof.”

4. Protection in case of obliterated cheque : Under section 89 of the N.I. Act 1881, ” whereas a cheque is presented for payment which does not at the time of presentation appeared to be crossed or to have had a crossing which has been obliterated, payment thereof by banker is liable to be paid and paying the same according to the apparent thereof at the time of payment and otherwise in due course, shall discharge such banker from all liabilities thereon and such payment shall not be questioned by reason of the cheque having been crossed.”

5. Protection incase of drafts : Section 85 of the N.I. Act. The section states : “Whereas any draft i.e. under to pay money drawn by the office of a bank upon another office of the same bank for a sum of a money payable to order on demand, purports to be endorsed by or on behalf of the payee, the bank is discharged by payment in due course.

Q.26. Explain the statutory protection to a collecting banker.

Ans :- The collecting banker gets statutory protection under Section 131 of N.I. Act 1881-

“A banker who has in good faith and without negligence received payment of a cheque crossed generally or specially to himself shall not incase the title of the cheque prove defective, incur any liability to the owner of the cheque by reason of having received such payment.”

Thus, for getting protection the collecting banker are required to satisfy the following conditions :

1. Good Faith and without Negligence : For getting protection, collecting banker have to prove that they have collected the cheque in good faith. Here good faith means honestly. A thing is deemed to be done in good faith when it is in fact done honestly whether negligently or not, he should not be negligent in receiving the payment. Generally speaking negligence indicated lack of care which is necessarily to be taken in any circumstances.

2. For crossed cheque only : Section 131 of N.I. Act 1881, a banker will be give a protection only with to crossed cheque. The banker will not be provided any protection in case of open cheque because open cheque need not to be collected through bank. Open Cheque are paid on the counter of the bank. It is also necessary that cheque should be crossed before depositing to the collecting banker.

3. Agent of his customer : For getting statutory protection here the bank is required to collect cheque only of his customer. Customer means a person who has an account with the bank. If a bank is collecting cheque for a person who is not the customer of bank then he will not be provided Statutory protection. The Statutory protection will be provided to the bank under Section 131 of N.I. Act, only when he is collecting cheque as an agent of his customer and not as a holder for value.

Q.27. Explain briefly about the material alteration of a cheque.

Ans :- A cheque with material alterations make the instrument null and void. Therefore, if a cheque with out any apparent but with material alteration is paid by a banker, he will not get the protection provided by sections 80 and 82 of the Bills of Exchange Act 1882. An alteration is material which in any way alters materially or substantially the operation of the instrument and the liabilities of the parties thereto, irrespective of whether or not the change is prejudicial to the payee. Material alteration include the alteration of the date, crossing, place of payment, amount and name of the payee. As discussed in Gourchandra Das Vs. Prasanna Kumar Chandra, 33 Calcutta 812. 816.” Any change in an instrument which causes to speak a different language in legal effect from that which is it originally spoke or which changed the legal identity or character of the instrument either in terms or in relation to parties thereto is material alteration.” Material alteration may be in the following forms :

(i) Alteration of date.

(ii) Alteration of place of payment.

(iii) Alteration of amount.

(iv) Alteration in the names of parties.

(v) Alteration of the word ‘bearers in place of order’.

(vi) Alteration of crossing.

According to section 87 of the Negotiable instruments Act. “any material alteration of a negotiable instrument renders the same void as against anyone who is a party thereto at the time of making such alteration, and does not consent thereto unless it was made in order to carry out the common intention of the original parties; and any such alteration, if made by an endorse, discharges his endorser from all liability to him in respect of the consideration thereof.”

Q.28. Briefly mention the duties and responsibilities of a collecting banker.

Ans :- The collection of cheques and bills on behalf of customers is an important function of almost every modern because it provides a facility which can hardly be despondent with especially in case of crossed cheques. It is necessary that in performing these functions bank should careful, otherwise he may lead himself in difficulties.

Thus the collecting banker has the following duties and responsibilities.

(i) Presentment for payment with a reasonable time :

The bank should collect the cheques sent by the customer with due care and should present it to the drawee bank within a reasonable time. He must use only the recognised channels for collection, when a cheque is drawn on a bank in the same place, the banker should present it the day after he receives it. When the cheque is drawn on a bank in another place it should be presented or forwarded in the day after receipt. In case, if he fails in his duty, and as a consequence customer suffers a loss, the loss will be compensated by the collecting banker.

(ii) Serving notice of dishonour :

When the cheque is dishonoured the collecting banker must within a reasonable time give notice to the customer as to him to take action against the prior parties. Incase, the banker fails, it will be liable to the customer for any loss that the customer might have suffered on account of such failure.

In case a cheque is returned by the drawee bank for confirmation of endorsement, it is not dishonoured. In such case, notice should be given to the customer. If such notice is not given and the cheque is returned second time and the customer suffers a loss, the banker may be held liable for the loss.

(iii) Agent for Collection :- If the cheque is drawn on a place where the banker is not a member of the clearing house, he may employ another banker who is a member in it for the purpose of collecting the cheque. In such a case, the latter banker becomes a substituted agent.

(iv) Permittance of proceeds to the customer :- When a cheque is released by a collecting banker he should pay the proceeds to the customers as soon as practicable in accordance with the customer’s direction, usually, the amount is credited to the customer’s account.

(v) General duties :- The following are the general duties of a collecting banker in connection with a cheque which he has accepted from his customer with a view to collect the payment for and on behalf of his customer while functioning as the agent of his customer :

(i) It is the duty of the collecting banker to accept the cheque from his customer for collection.

(ii) It is the duty of the collecting banker to fully verify the ownership right to his customer in respect of the cheque he has accepted for collection.

(iii) It is again the duty of the collecting banker to accept the cheque for collecting only from the customer whose accounts were opened with proper introductory reference.

(iv) It is his duty to ask for introductory references of the account of the customer which was opened without introduction.

(v) If an open cheque is submitted to the banker for collection, the banker owes a duty towards himself to get cheque crossed by the depositing customer.

Q.29. Discuss the precautions a banker should take for payment of Mutilated Cheques.

Ans :- 1. Precaution regarding ‘form of the cheque’ :- The cheque should be proper from. The Negotiable instruments act defines a cheque but does not prescribe its form. But almost every bank in India requires that cheque must be drawn on the banks printed form and the bank reserves its right to refuse payment of any cheques drawn otherwise. This makes it essential that the cheques forms issued by the banker must be used by the customers.

2. Precaution regarding date :- The banker should refuse to honour an undated cheque which has been presented to it for payment. The drawer of a cheque fills in the date before the cheque is issued, but if he has not done so, the instrument does not become invalid. The payee of the cheque or any subsequent holder thereto may fill in the date. The date should not be incomplete i.e. it must include besides the year the name of the month and the member of the day.

3. Precaution regarding “amount’ :- The banker should see that the amount mentioned both in figures and words in the cheque are the same. In case they differ, the amount stated in words may be taken as correct and the banker may make the payment. Incase the amount has been started in words only and not in figures the banker should pay the cheque. But where the amount has been mentioned in figures only not in words, the banker should return the cheques.

4. Precaution regarding ‘funds’ of the customer :- There should be sufficient funds in the account of the customer for payment of the cheque. Cheque has to be paid in full and not in part. Therefore, inadequacy of funds will result in dishonour of the cheque.

The cheque should be paid in Chronological order of their receipt by the bank. Therefore, incase of inadequacy of funds, the cheques will be paid in the order in which they are received by the bank to the extent the funds permit and the rest will be dishonoured.

5. Precaution regarding ‘material’ alteration :- A cheque contains a mandate of the drawer to his banker to pay a specified sum of money to the bearer or the person mentioned therein or to his order. In case a cheque is materially altered and the banker makes the payment, he shall be discharged from liability.

6. Precaution regarding drawer’s signature :- A banker is expected to know the signatures of his customers and therefore, if the drawer’s signatures has been forged, and the banker makes the payment it shall not be entitled to debit the customer’s account with the payment. The loss will be borne by banker.

7. Precaution regarding Mutilated cheques :- A cheque is said to be mutilated when it is turn into two or more pieces. Before making payment of a mutilated cheque, the banker should examine it carefully to ascertain if the cheque was mutilated with the intention to cancel it. If such intention is evident or if the main contents of the cheque are illegible, the banker should not pay the cheque. In other case, banker should get the drawer’s confirmation on the mutilated cheque. He may pay a cheque which is turn of the corner and no material fact is erased or cancelled.

8. Precaution regarding banking hours :- The banker should make payment of only such cheques which have been presented to its for payment during its banking hours. Any payment of cheques which was presented after banking hours will not be taken as a payment in due course and banker will not be entitled to debit the customer’s accounts.

9. Precaution regarding crossing :- If the cheque is a crossed one, it should not be paid on the counter but through a collecting banker.

Q.30. Discuss the precautions a banker should take for payment of Crossed Cheques.

Ans :- (1) Date of cheque :- A banker should take more precaution regarding the date of a cheque. The banker has to pay those cheques where the date is valid. As per law a cheque is valid upto six (6) months. If a cheque comes for payment after six months the banker may refuse to make payment and ask the holder to get the cheque rectified.

(2) Signature of customer :- A change in the sign and the specimen with the bank warrant security precautions. In such a case proper questioning is to be done to the customer. A banker always keep a complete updated record of the signature of the drawer A banker is supposed to know the signature of his customer but not of all the subsequent endorsee.

(3) Sum of Money :- In the time of writing a cheque it is to be mention the amount of the worth of cheque both in words and figures. In case of may major difference in both, the bank has to ascertain the correct figure and if that can not be easily decided, banker may refuse payment.

(4) Proper Format of cheque :- In general all customer with a savings account are given cheque books if they request for the same and in case of current account normally every account has a cheque book.

Q.31. Explain the obligation of banker to pay cheque.

Ans :- The obligation of banker to pay cheque are :-

(1) Precaution regarding form of the cheque :- The cheque should be in proper form. The negotiable Instruments act defines a cheque but does not prescribe its form. But almost every bank in India requires that “cheque must be drawn on the banks printed forms and the bank reserves its right to refuse payment of any cheques drawn otherwise.

(2) Precaution regarding date :- The banker should refuse to honour and undated cheque which has been presented to it for payment. The drawer of a cheque fills in the date before the cheque is issued, but if he has not done so, the instruments does not become invalid.

(3) Precaution regarding ‘amount’ :- The banker should see the amount mentioned both in figures and words in the cheque are the same. In case they differ, the amount stated in words may be taken as correct and the banker may make the payment. In case the amount has been started in words only and not in figured the banker should pay the cheque.

(4) Precaution regarding ‘funds of the customer :- The fund should be sufficient in the account of the customer for payment of the cheque. Cheque has to be paid in full and not in part. Therefore, inadequacy of funds will result in dishonour of the cheque.

(5) Precaution regarding material alteration :- A cheque a mandate of the drawer to his banker to pay a specified sum of money to the bearer or the person mentioned therein or to his order. In case a cheque is materially altered and the banker makes the payment, he shall be discharged from liability.

(6) Precaution regarding drawer’s signature :- A banker is expected to know the signatures of his customers and therefore, if the drawer’s signatures has been forged and the banker makes the payment if shall not be entitled to debit the customers account with the payment.

(7) Precaution regarding mutilated cheques :- A cheque is said to be mutilated when it is torn into two or more pices. Before making payment of a mutilated cheque, the banker should examine it carefully to certain if the cheque was mutilated with the intention to cancel it.

Q.32. Explain the advantages and disadvantages of bearer cheque.

Ans :- The advantages of bearer cheque are :-

(i) A bearer cheque is transferable by mere delivery.

(ii) Indorsement is not needed.

The disadvantage of bearer cheque are :-

(i) The paying banker need not seek the identification of the holder of the cheque.

(ii) Such cheques are risky, this is because if such cheques are lost, the finder of the cheque can collect payment from the bank.

Q.33. Explain the position of a collecting banker as a ‘holder for value’.

Ans :- The position of the collecting banker as a ‘holder for value’ they are :

If the collecting banker pays to the customers the amount of the cheque or credit such amount to his account and allows him to draw it, before the amount of the cheque is actually realised from the drawee banker, the collecting banker is deemed to be its ‘holder for value’.

A banker becomes its holder for value by giving its value to the customer in any of the following ways :

(a) By lending further on the strength of the cheque.

(b) By Paying over the amount of the cheque or part of it in cash or in account before it is cleared.

(c) By agreeing either than or earlier, or as a course of business that customer may draw before the cheque is cleared.

(d) By accepting the cheque in avowed reduction of an existing overdraft and

(e) By giving cash over the counter for the cheque at the time it is paid in for collection.

In any of these circumstances the banker becomes the holder for value and also the holder in due course. He bears the liability and possesses the right enjoyed by the holder for value.

Q.34. Explain the advantages and disadvantages of Bearer Cheque.

Ans :- See the Answer of Question No. 32.

E. Long answer questions : Type-II

Q.35. When should a Banker refuse payment of a cheque ?

Ans :- Following are the circumstances for which the banker must refuse payment of the cheques.

(i) When the balance to the credit of the customer is insufficient to meet the cheque.

(ii) When the funds are not properly applicable to the payment of a cheque.

(iii) After receiving the notice or information of death, the banker should stop payment of all cheques drawn against the account.

(iv) When the customer has informed the bank about the loss of cheque.

(v) When the bank comes to know of the defect in title of the person presenting a cheque.

(vi) When the bank comes to know about the customer is applying funds in breach of trust.

Q.36. Discuss the precautions a banker should take for making payment of his customer’s cheque.

Ans :- The precaution of a banker for making payment of his customer cheque are :

1. Date of cheque :- A banker should take more precaution regarding the date, of a cheque. The banker has to pay those cheques where the date is valid. As per law a cheque is valid upto six (6) months. If a cheque comes for payment after six months banker may refuse to make payment and ask the holder to get the cheque rectified.

2. Signature of Customer :- A change in the sign and the specimen with the bank, warrant security precaution. In such a case proper questioning is to be done to the customer. A banker always keep a complete updated record of the signature of the drawer. A banker is supposed to know the signature of his customer but not of the subsequent endorsees.

3. Sum of Money :- In the time of writing a cheque it is to be mention the amount of the worth of cheque both in words and figures. In case of any major difference in both, the bank has to ascertain the correct figure and if that can not be easily decided banker may refuse payment.

4. Proper Format of cheque :- In general all customer with a saving account are given cheque books if they request for the same and in case of current account normally every account has a cheque book.

5. Crossing of the cheque :- We have already mentioned that, crossed cheques are paid only through another bank. A specific crossing of cheque makes it obligatory on the bank to obey the crossing.

6. Condition of Cheque :- We know that a cheque is a negotiable instrument. So it should not be defined mutilated or in any other way the original documents must not be charged.

7. Time of Presentation :- Cheques paid over the counter should be paid normal working how. Payment in good faith is sometime risky for the bank if the drawer dies, or is declared insolvent.

Q.37. Define crossing. Explain the different forms of crossing.

Ans :- Crossing is an instruction given to the paying banker to pay the amount of the cheque through a banker only and not directly to the person presenting it at the counter. A cheque bearing such an instruction is called a crossed cheque others without such crossing are open cheque which may be encashed at the counter of the paying banker as well.

The different types of crossing are :- Section 123 to 131 of the Negotiable Instrument Act 1881 contain provision relating to crossing. Crossing on cheques is of two types : General crossing and Special crossing.

General Crossing :- According to section 123, Where a cheque bears across its face an addition of the words and company or any abbreviation thereof, between two parallel transverse lines, or two parallel transverse lines simple, either with or without the words ‘not negotiable’ that addition shall be deemed a crossing and the cheque shall be deemed to be crossed generally.

It is to be noted that the above that drawing of two parallel transverse lines on the face of the cheque constitutes ‘general crossing’.

The lines must be

(i) On the face of the cheque.

(ii) Parallel to each other. And

(iii) In cross direction (i.e. transverse)

Special Crossing :- According to section 124, “where a cheque across in face an addition of the name of a banker, either with or without the words not negotiable, that addition shall be deemed a crossing and the cheque shall be deemed to be crossed specially and to be crossed to the banker.

Section 123 and 124 permit that the words not negotiable may be included in the general and special crossing respectively. The inclusion of the words ‘not negotiable’ in the crossing has great practical significance. These words do not make the cheque non-transferable but their inclusion in the crossing takes away one of the important characteristics of a negotiable instrument.

Section 130 States

A person taking a cheque crossed generally of specially bearing in either case the words, ‘not negotiable’ shall not have and shall not be capable of giving a better title to the cheque than that which the person from whom he took it had.

The words “Account Payee” or “Account Payee only” in the crossing have special significance because they intend to make the cheques more safe. These words constitute an instruction to the collecting banker that he should collect the amount of the cheque for the benefit of the payees account only i.e….. to, credit the amount to the account of the payee only and nobody else. “Account Payee” crossing does not restrict transferability of the cheque which can be endorsed further.

Q.38. Explain the obligations of banker to pay cheque.

Ans :- 1. Precaution regarding form of the cheque : The cheque should be in proper form. The Negotiable Instruments act defines a cheque but does not prescribe its form. But almost every bank in India requires that cheque must be drawn on the banks printed forms and the bank reserves its right to refuse payment of any cheques drawn otherwise.

2. Precaution regarding ‘date’ :- The banker should refuse to honour an undated cheque which has been presented to it for payment. The drawer of a cheque fills in the date before the cheque is issued, but if the has not done so, the instrument doesn’t become invalid.

3. Precaution regarding ‘amount’ :- The banker should see that the amount mentioned both in figures and words in the cheque are the same. In case they differ the amount stated in words may correct and the banker may make the payment. In case the amount has been stated in words only and not in figures the bankers should pay the cheque.

4. Precaution regarding ‘funds’ of the customer :- There should be sufficient funds in the account of the customer for payment of the cheque.

5. Precaution regarding material alteration :- A cheque contains a mandate of the drawer to his banker to pay a specified sum of money to the bearer or the person mentioned therein or to his order. In case a cheque is materially altered and the banker makes the payment, he shall be discharged from liability.

6. Precaution regarding drawer’s signature :- A banker is encepted to know the signatures of his customers and therefore if the drawer signatures have been forged and the banker makes the payment it shall not be entitled to debit the customers account with the payment.

7. Precaution regarding mutilated cheques :- A cheque is said to be mutilated when it is torn into two or more pices. Before making payment of a mutilated cheque, the banker should examine it carefully to ascertain if the cheque was mutilated with the intention to cancel it.

8. Precaution regarding banking hours :- The banker should make payment of only such cheques which have been presented do its for payment during its banking hours. Any payment of cheques which was presented after banking hours will not be taken as a payment in due course and banker will not be entitled to debit the customers account.

Q.39. What are the duties and liabilities of a collecting banker ?

Ans :- (1) Immediate credit :- Many banks gives instant credit to the account of the customers for cheques lodged with them for collection. This services is dependent on the customers credit rating with the bank.

(2) Cheque of outstation :- In the modern world many banks along with State Bank of India have given the facilities to many customers of crediting their accounts immediately for outstation cheque.

(3) Right of lien :- Is some cases collecting banker enjoys the right to lien over the cheques that have been credited to the accounts of customers and the payment is not received.

(4) Offset against overdraft :- The customers some times gives clear instructions to the banker that the particular cheque is meant for adjusting against his overdraft.

(5) Checking endorsement :- The collecting bank should check the endorsement to a reasonable extent. When the name of endorsee and the signature of the subsequent endorser should match.

(6) Doctrine of Conversion :- When a banker wrongfully interferes or cheque the Negotiable Instrument in such a way that the right of owner are damaged, it is called conversion.

(7) Normal Mode of collection :- The normal mode of collecting is to present the instrument to the acceptor or maker on the drawee bank depending on which type of negotiable Instrument it is.

- SEBA Class 6 English Rainbow MCQ Chapter 1 Afternoon on the Hill

- SEBA Class 6 Charitra Path MCQ Chapter 14 জুইৰ ব্যৱহাৰ নকৰাকৈ খাদ্য প্ৰস্তুতকৰণ

- SEBA Class 6 Charitra Path MCQ Chapter 13 প্ৰকৃতিৰ সৈতে বন্ধুত্ব

- SEBA Class 6 Charitra Path MCQ Chapter 12 দুজন বাটৰুৱা

- Anandaram Dhekial Phukan Biography | আনন্দৰাম ঢেকিয়াল ফুকনৰ জীৱনী

Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques Question answer to each chapter is provided in the list so that you can easily browse through different chapters HS 2nd Year Banking Chapter 6 Cheques Collection And Payment Of Cheques Notes and select needs one.

SCERT Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques

Also, you can read the SCERT book online in these sections Solutions by Expert Teachers as per SCERT (CBSE) Book guidelines. These solutions are part of SCERT All Subject Solutions. Here we have given Class 12 Banking Chapter 6 Cheques Collection And Payment Of Cheques Solutions for All Subjects, You can practice these here.

Hi, I’m Dev Kirtonia, Founder & CEO of Dev Library. A website that provides all SCERT, NCERT 3 to 12, and BA, B.com, B.Sc, and Computer Science with Post Graduate Notes & Suggestions, Novel, eBooks, Biography, Quotes, Study Materials, and more.