Management Accounting Unit 1 Introduction, College and University Answer Bank for BA, B.com, B.sc, and Post Graduate Notes and Guide Available here, Management Accounting Unit 1 Introduction to each Unit are provided in the list of UG-CBCS Central University & State University Syllabus so that you can easily browse through different College and University Guide and Notes here. Management Accounting Unit 1 Introduction can be of great value to excel in the examination.

Management Accounting Unit 1 Introduction

Management Accounting Unit 1 Introduction Notes cover all the exercise questions in UGC Syllabus. Management Accounting Unit 1 Introduction provided here ensures a smooth and easy understanding of all the concepts. Understand the concepts behind every Unit and score well in the board exams.

Introduction

MANAGEMENT ACCOUNTING

| VERY SHORT TYPES QUESTION & ANSWERS |

1. Fill in the blanks:

(a) Management accounting is concerned with the _____________of accounting information that is useful to management.

Ans: Presentation.

(b) Preparation of financial statements is necessary under _____________ law.

Ans: Company.

(c) Management accounting is based on ___________ information.

Ans: Accounting.

(d) Management accountant is only to ____________ the management and not to supply decisions to term.

Ans: Guide.

(e) Financial accounting states the ____________ position of a concern.

Ans: Financial.

(f) Only __________ information is recorded in accounting.

Ans: Quantitative.

(g) Management accounting statements are not to be ____________.

Ans: Published.

(h) Management accounts cannot be ____________.

Ans: Audited.

(i) Management accounting uses ___________ data for planning and forcasting.

Ans: Historical.

(j) Financial accounts are governed by ___________ principles.

Ans: Generally accepted.

(k) Management accounting relates to ____________ of accounting data.

Ans: Presentation.

(l) Management accounting is helpful in increasing _____________.

Ans: Efficiency.

(m) In Management accounting no emphasis is given to ____________.

Ans: Actual figures.

(n) Management Accounting interprets various financial statements to the ____________.

Ans: Management.

(o) Management Accounting is based on data supplied by _____________.

Ans: Financial Accounting.

2. State whether the following statements are true or false:

(a) Management accounting provides decisions to management.

Ans: False.

(b) In Management accounting no emphasis is given to actual figures.

Ans: True.

(c) Publication of management accounting statements is not compulsory.

Ans: True.

(d) Management accounting reports are leased on current year’s figures as in financial accounting.

Ans: False.

(e) Management accounting deals with both qualitative and quantitative information.

Ans: True.

(f) Management accounting is concerned only with the present state of the business concern.

Ans: False.

(g) The avoidance of insignificant things will not affect accounting results.

Ans: True.

(h) Intuitive decision limit the usefulness of management accounting.

Ans: True.

(i) The management accounting process begins with identification measurement and accumulation of relevant data from financial and cost accounting records.

Ans: True.

(j) Financial data is generally collected and presented in a technical way.

Ans: True.

(k) Management Accounting is a technique of selective nature.

Ans: True.

(l) In Management Accounting only those figures are used which can be measured in monetary terms.

Ans: False.

(m) Management Accounting will not provide information in a prescribed proforma like that of financial accounting.

Ans: True.

(n) The main objectives of management accounting is to help the internal management.

Ans: True.

(o) Management accounting is concerned only with the present state of the business concern.

Ans: False.

SHORT TYPE QUESTIONS & ANSWERS

1. What do you mean by Management Information System (MIS)?

Ans: Management Information System (MIS) is an approach of providing timely, adequate and accurate information to the right person in the organization which helps in taking right decisions. In other words MIS is a scientific way of collecting, processing, storing and communicating information relating to the various activities of an organization to the various level of management.

2. Explain the term ‘Decision making Process’?

Ans: Decision making is an important job of a manager. Every day he has to decide about doing or not doing a particular thing. A decision is the selection from among alternatives. A decision represents a course of behaviour chosen from a number of possible alternatives. Thus, decision making process is a technique through which a manager chose the best out of various alternatives available.

3. What do you understand by ‘Financial Controller’?

Ans: The term ‘Financial Controller’ is used in the United States of America for top management accountant executive in a firm. He is considered to be the figure partner in the management team since he has the responsibility for collection of figures both from within and outside the company.

4. Write in brief about the following:

(a) Management accounting.

Ans: Management accounting is the presentation of accounting information in such a way as to assist management in the creation of policy and the day-to-day operation of an undertaking. Accounting to J. Batty, a management accounting is the term used to describe the accounting methods, systems and techniques which, coupled with special knowledge and ability, assist management in its task of maximising profit or minimising losses.

(b) Management accounting information.

Ans: Accounting provides information to vested interests in a business organization:

Managers, shareholders, employees, creditors, customers etc. various parties are interested to know about the activities of the business. As for example, managers may use accounting information as a managerial tool, shareholders will be interested in financial health, creditors will be interested in credit worthiness and the like. So, different parties use accounting information according to their needs.

(c) Management accounting conventions.

Ans : Accounting convention is an established usage or custom followed in recording and presenting financial data to make the financial statements clear and meaningful to the users. In management accounting also, some conventions are applied in recording, analyzing and interpreting financial statements. As for example – only normal costs should be considered while finding out the cost of the products, the convention of objectivity should be followed while presenting financial statements, etc.

LONG TYPE QUESTIONS & ANSWERS

1. Define the term Management Accounting. State the objectives of Management Accounting?

Or

Define the term Management Accounting. Describe the uses of accounting information for managerial decision making purpose?

Or

Define the term Management Accounting. Discuss the management accounting as a tool in:

(i) Decision making, and

(ii) Exercising control.

Ans: Anglo-American Council on productivity defines Management Accounting in the following terms:

“Management Accounting is the presentation of accounting information in such a way as to assist the management in the creation of policy and the day-to-day operation of an undertaking”.

J. Betty defines Management Accounting as follows: ‘Management Accounting is the term used to describe the accounting methods, systems and techniques which, coupled with special knowledge and ability assist management in its task of maximising profits and minimising losses.’

According to the management Accounting Practices Committee set up by the national Accounting Association of the USA. ‘Management Accounting is the process of identification, measurement, analysis, preparation, interpretation and communication of financial information by management to plan, evaluate and control within an organisation and to assure appropriate use of an accountability for its resources.’

Thus it is the process of:

(i) Identification and evaluation of financial transaction.

(ii) Measurement of such business transactions.

(iii) Recording of such transaction.

(iv) Preparation and interpretation of business information.

The essence of management process is decision making for specific objectives and the decision making system is said to be efficient when such objective are realised with minimum use of resources.

Objectives:

(a) Planning an policy formulation: Planning is statement what should be done, and how it should be done, and when it should be done. It is the design of a desired future state of an entity and of the effective ways of bringing it about, (According to Welsch).

(b) Organisation: Organisation is the establishment of relationship among the different individual in a concern. It involves the delegation of authority and the fixing of responsibility.

Management accounting helps the management in establishing cost. Centres, Preparing budget, preparing cost control accounts and fixing responsibility for different functions.

(c) Co-ordination: Co-ordination among the different departments is essential for successful materialisation of goals. It is done through enforcing each department to stick to its budgeted performance and the management accountant assists the management in this respect by providing it with budget appraisal reports.

(d) Controlling: Control implies the measurement and evaluation of performance.

It involves the following functions:

(i) Comparison of actual performance against predetermined budgets and standards.

(ii) Initiation of an action that may correct the deficiencies indicated.

(iii) Follow-up to appraise the effectiveness of the corrective action.

(e) Motivation: Management accounting is a motivational device. It is oriented towards persons. Performance reports prepared by the management accountant focuses on the actual performance of the concerned personal and incentives are offered or penalty is awarded on performance appraisal.

(f) Decision Making: Where Management is confronted with alternatives for the attainment of budgeted goals, management accounting appraises alternative and suggests the better one. This is done through flexible budgeting, marginal, costing and capital budgeting techniques.

2. What do you mean by Management Accounting? Explain the nature or characteristics of Management Accounting.

Ans: Management Accounting is the presentation of accounting information in such a way as to assist the management in the creation of policy and the day-to-day operation of an undertaking”. Managerial accounting, also called management accounting, is a method of accounting that creates statements, reports, and documents that help management in making better decisions related to their business’ performance. Managerial accounting is primarily used for internal purposes.

The following characteristics or Nature:

(i) Decision Making System: It provides information to the management which assists it in the creation of policy and day-to-day operations of the undertaking.

(ii) Systematic Approach to planning and control: It provides, information to the management for a system of setting standards, plans or targets and reporting variances between planned and actual performances for corrective actions.

(iii) Futuristic: It helps the management to evaluate future through the use of standard costs and budgets.

(iv) Supplies Data: It provides accounting data for projection and planning future.

(v) Provides tools and Techniques: It provides various tools and techniques for control of business operations, improvement of overall efficiency in using economic resources and maximisation of profit.

(vi) Cause and Effect relationship: It shows cause and effect relationship through various analysis technique and enables the management in taking remedial measures.

3. Discuss the scope of management accounting. Describe the tools and techniques of management accounting needed for managerial decision.

Ans: The scope of management accounting inter-alia including:

(i) Installation and operation: Installation and operation cost accounting in order to determine the cost of production of different products and services and to bring about cost control and cost reduction.

(ii) Providing Means of communication: It provides a means of communicating management plans to various levels of organisation. It also co-ordinates their activities, defines their roles and assists the management in directing their activities to the common goal.

(iii) Providing a system of Feed-Back reports: It provides a system by which feedbacks of departmental activities can be reported to management. In it relevant information is provided to the management with a suggestion for taking corrective measures in desired cases.

(iv) Analysis and Interpretation: Analysis and Interpretation of facts are made understandable and usable to the management in order to enable it to fix responsibilities and to bring about necessary changes in orgainisation.

(v) Providing Method of Evaluation of performance: It provides methods and techniques for evaluating the performance of management against the declared objectives.

(vi) Modification of Techniques: It modifies and sharpens the effectiveness of the existing techniques of analysis in order to increase the profitability of the enterprise.

(vii) Inventory controlling: Its function involves exercising control over inventory through fixing different levels of stocks, perpetual inventory etc. It is essential in managing liquidity and profitability.

The various tools and techniques used in management accounting for assisting the management in decision making are discussed below:

(i) Financial Planning: Financial planning involves determining both long-term and short-term financial objectives of an enterprise, formulating financial policies and developing financial procedures to achieve the objectives.

(ii) Historical cost Accounting: Financial Accounting record actual cost which are used in operative a standard costing system and determining variance.

(iii) Standard costing: It is an important tool of cost control. It involves the preparation of standard costs, their comparison with the actual costs and analysis of the differences. It is also necessary for performance appraisal.

(iv) Marginal costing: It is a method of costing which is concerned with the changes in costs resulting from the changes in volume of production. It is concerned with variable cost.

(v) Decision Accounting: Decision making is the primary function of the top management. It involves a choice from various alternatives. It facilities the correct selection of a proposal.

4. Discuss the importance of management accounting. Explain the nature of Management Accounting.

Ans: The importance of management accounting are as follows:

(i) Increases Efficiency: Management accounting increases efficiency of business operations. The targets of different departments are fixed in advance and the achievements of these goals is a tool for measuring their efficiency.

(ii) Proper Planning: Management is able to plan various operations with the help of accounting information. The work load of each and every individual is fixed in advance. The activities of the concern are planned in a systematic manner.

(iii) Maximizing Profitability: The trust of various management techniques is to control cost of production in the organization. The steps of controlling costs are able to reduce cost of production. The profits of the enterprise are maximized with the help of management accounting system.

(iv) Improves service to customers: The cost control devices employed in management accounting enable the reduction of prices. All employees in the concern are made cost conscious. The quality of products become good because quality standards are pre-determined. The increase in production of goods also enhances supply of goods to consumers.

(v) Effective Management Control: The tools and techniques of management accounting are helpful to the management in planning, co- ordinating and controlling activities of the concern. Everybody assesses his own work and immediate actions are taken in case of deviations in performance.

Nature of Management Accounting are explained below :

(i) Provides Information: As we have mentioned above, management accounting means to provide information to different levels of management. It’s necessary to represent the information in a proper way to meet the managerial requirements.

The accounting department is responsible for collecting the data that is used to evaluate some policy decisions and make changes if it is necessary. The management team is interested only in the data from position state merit and income statement, which will be helpful for them to make accurate decisions on several aspects of the business.

(ii) Cause and Effect Analysis: One of the main distinctive features of managerial accounting from financial accounting is that it reviews the cause and effect relationship, while the financial accounting only focuses on determining the profit and loss. Managerial accounting explores the reasons behind loss and profit and analyzes their effect. For example, profits are compared to current assets, sales, share capital, and so on. It gives the opportunity to the management team to make appropriate conclusions.

(iii) Special Techniques and Concepts: Management accounting utilizes special techniques and concepts in order to make accounting information more useful and functional for the management team.

These techniques include standard costing, marginal costing, financial planning and analyses, budgetary control, cash flow, and so on. Generally, these techniques are considered to be very effective in representing the data and takin control over business operations.

(iv) Decision Making: We have already highlighted, that the main goal of management accounting is to provide the information to the management team in order to facilitate the decision-making process for them.

The managers carefully study the historical data in order to see its impact and make some predictions for the future. They are able to develop some alternative plans and choose the most advantageous course of action for the company.

It’s always extremely difficult for the managers to make decisions and management accounting made it a much easier process for them.

(v) Objectives: Managerial accounting is very useful in determining the objectives and forming plans for the future. It’s done based on analyzing the historical information and comparing it to the current situation. The managers get the appropriate idea about the performance of several departments and they make some necessary changes if there are any deviations of actuals when they evaluate the past results.

This can be achieved by the above-mentioned special techniques such as budgetary control and standard costing. As a result, the managers are able to establish the objectives and improve their overall performance.

(vi) No Fixed Rules: Although financial accounting has various established rules and conventions in providing financial accounts there are no such norms for managerial accounting. The techniques and tools are the same for both of them, but how you use those techniques depends on the concern and situation. The management team should be intelligent and experience enough to analyze the provided data and decide which technique should be utilised in a certain situation.

5. How is management accounting different from financial accounting?

Ans: Financial accounting and management accounting are closely related because the management accounting draws out a major part of the accounting information from financial accounting and modifies the same for managerial use Financial accounting is concerned with recording and classifying the business transaction and preparing periodical financial statement for financial position. On the otherhand, management accounting is to provide necessary information for management planning and control.

The distinguishing point of Management and Financial accounting are stated below:

(i) Objective: Financial accounting is attached more with reporting the results and position of the business to the persons and authorities other than the management- creditors, investors, government, etc.

Management accounting is concerned more with generating information for the use of internal management in decision making process such as planning, control etc.

(ii) Nature: Financial accounting is historical in nature and transactions are recorded after they have taken place.

Management accounting analyses the events as they take place and project them for future.

(iii) Precision: Financial accounting is historical in nature hence is actual and precise.

Management accounting reflects the future hence it is mere estimation, so it requires periodical adjustments.

(iv) Periodicity Reporting: Periodicity in reporting finance accounts is much wider than that in the management accounting e.g. annual statements.

In management accounting, weekly, fortnightly, even monthly reporting is done.

(v) Accounting Principles: Financial accounting has to be governed by the generally accepted accounting principles and legal provisions since it has the cater the information needs of the outsiders.

Management accounting need not worry about such conventional and legal constraints. It is free to formulate its own rules, procedures and forms since it is used for internal use.

(vi) Legal Compulsion: Financial accounting is compulsory in case of a joint stock Company and is necessary for other forms of business organisation for tax purposes.

On the other hand, management accounting is optional and its forms and contents depend upon the outlook of the management.

(vii) Contents: Financial accounting contains only the monetary information. Whereas management accounting contains both monetary and nonmonetary information.

(viii) Publication a Audit: Financial statements are published for the benefit of public and are subject to audit especially in case of companies.

On the other hand, management accounting is prepared for internal use of the management. So it is not required to be published or audited.

6. Discuss the functions of Management Accounting.

Or

“Management accounting is the presentation of accounting data in such a way as to assist the management in the creation of policy and in the day-to-day operation of an undertaking. Explain the statement bringing out essential services of management accounting.” Explain.

Or

Discuss the services of the management accountant.

Or

Management Accounting is concerned with information which is useful to management.

Or

Explain the above statement highlighting the nature of information referred to.

Ans: It includes the following functions:

(i) Planning and forecasting: Management fixes various targets to be achieved by the business in future. Planning and forecasting are essential. They can help greatly in this process through various techniques such as budgeting, standard costing, marginal costing, fund flow statement, profitability trend analysis, etc. Thus it helps the management in short term and long-term forecasts and planning the future operation of the business.

(ii) Communication: Management accounting is the important medium of communication. Different levels of management, such as top, middle and lower levels, needs different types of information and the management accounting provides them with necessary information as and when they are needed.

(iii) Modification of Data: Management accounting modifies the available accounting data by re-arranging them in such a way that they become easily understandable and useful to the management.

(iv) Decision Making: Management accounting analyses and ranks different proposals on the basis of their profitability and submits the appraisal report to the management for investment decision.

(v) Co-ordination: Co-ordination is an important part of management control. Management accountants act as a coordinator among the different functional departments. It facilitates the management to direct all departmental activities towards the common goal.

7. How does management accounting different from cost accounting?

Ans: Management accounting and cost accounting and two branches of accounting. Both cost accounting and management accounting are internal to the organisation and both assist the management in their managerial function.

In many areas both are overlapping in their functions, still the two systems can be differentiated on the following grounds:

(i) Object: Primary objective of cost accounting is the ascertainment, allocation and distribution of costs.

While the purpose of management is to provide information to the management for the purpose of planning, coordinating and controlling of business activities.

(ii) Nature of information: Cost accounting is based on past and present facts and figures.

While management accounting is based on future projects and plans based on present and past cost data.

(ii) Principle: Certain principles and procedures are followed in cost accounting.

While no such principles and procedure are being followed in management accounting.

(iv) Nature of Data used: In cost accounting, only quantitative data is used.

While in management accounting both quantitative and qualitative data are used.

(v) Scope: The scope of cost accounting is comparatively narrow and primarily concerned with cost ascertainment.

While the scope of management accounting is very wide. It includes financial accounting, cost accounting, budgeting, tax planning etc.

(vi) Installation: Cost accounting can be installed without management accounting.

While management cannot be installed without a proper cost accounting system.

8. Management Accounting is mainly concerned with presentation of accounting information is such a way that is useful to management in decision making.” Explain the statement.

Ans: Financial accounting is the presentation of accounting information for stakeholders and regulators. It presents the financial position for an entire time period. On the other hand, Management accounting is the presentation of analysis of business activities to the internal management to facilitate decision making.he financial accounting is mainly concerned with the preparation of final accounts, i.e. Profit and Loss Account and Balance sheet. The business has become so complex that mere final accounts information is not sufficient in meeting informational needs. The management needs information for planning, controlling and coordinating business activities. It is because of the limitations of financial accounting that cost accounting and management accounting have developed.Financial accounting is a technical subject. The recording of transactions and making their use requires knowledge of accounting principles and conventions. A person who is not aware with accounting subject has little utility of financial accounts.This presentation includes forecasts, budgets and in-depth analysis. Hence it assists the management in planning the business activities. Since management accounting presents various charts, forecasts and analysis the management uses it for decision making.

9. Explain the Functions of Management Accounting. Elaborate the Organisation for Management Accounting.

Ans: Main objective of management accounting is to help the management in performing its functions efficiently. The major functions of management are planning, organising, directing and controlling. Management accounting helps the management in performing these functions effectively.

(i) Presentation of Data: Traditional Profit and Loss Account and the Balance Sheet are not analytical for decision making. Management accounting modifies and rearranges data as per the requirements for decision making through various techniques.

(ii) Aid of Planning and Forecasting: Management accounting is helpful to the management in the process of planning through the techniques of budgetary control and standard costing. Forecasting is extensively used in preparing budgets and setting standards.

(iii) Help in Organising: Organising is concerned with establishment of relationships among different individuals in the firm. It includes delegation of authority and fixing responsibility. Management Accounting aims at aiding the Management in organising through establishment of cost centres, profit centres, responsibility centres, Budget preparation etc. AH these activities are helpful in setting up an effective organisational frame work.

(iv) Decision Making: Management accounting provides comparative data for analysis and interpretation for effective decision making and policy formulation.

(v) Reporting to Management of Different levels: One of the Major objectives of Management accounting is to keep the Management informed about the performance, adherence to plans and progress of various sections of the organisation.

Top Management needs feed-back about implementation of its plans policies and programmes. Middle level Management and even junior executives need data for day to day operating decisions. Periodical and frequent reports are prepared and sent in time by Management Accountant to cater to the needs of all the levels of Management.

(vi) Communication of Management Policies: Management accounting conveys the policies of the management downward to the personal effectively for proper implementation.

(vii) Effective Control: Standard costing and budgetary control are integral part of management accounting. These techniques lay-down targets, compare actuals will standards and budgets to evaluate the performance and control the deviations.

(viii) Incorporation of Non-Financial Information: Management accounting considers both financial and non-financial information for developing alternative courses of action which leads to effective and accurate decisions.

(ix) Coordination: The targets of different departments are communicated to them and their performance is reported to the management from time to time. This continual reporting helps the management in coordinating various activities to improve the overall performance.

(x) Motivating Employees: Budgets, standards and other programmers are to be implemented in practice by the employees. A major objective of Management accounting is to determine the targets in the form of budgets, standards and programmer in such a way that the employees feel motivated to achieve them. This is usually accomplished by making the targets practicable and offering suitable monetary and Non-Monetary incentives to achieve them.

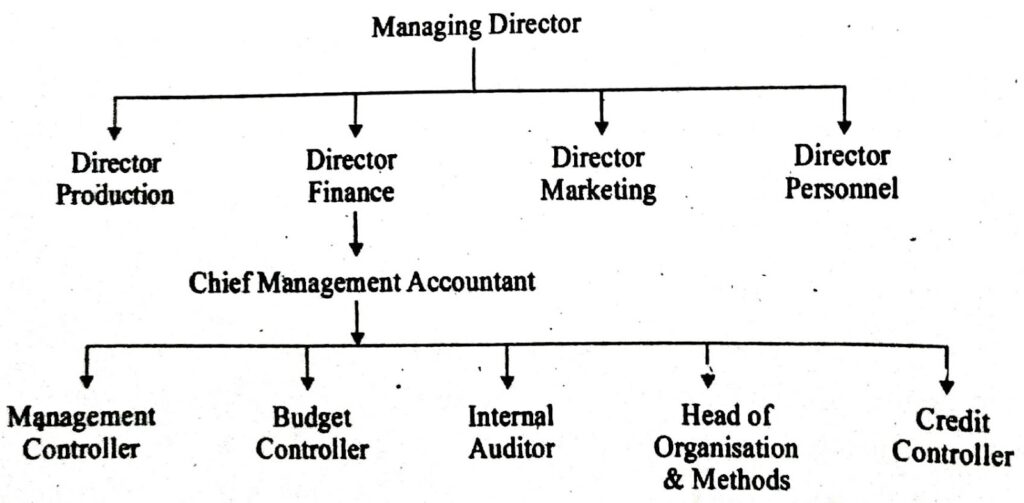

The Organisation for Management Accounting system will depend on the scale of operations, nature of business, nature of organisation, etc. In a small concern, management accountant is directly under the owner. In a big concern management accounting may be assigned to financial controller.

A concern with a divisional set up will have a different management organisation. The role of management accountant has been emphasised by Anderson and Schmidt management accounting will be specifically concerned, about the problem of cooperation with all other is no other functional element in the whole organisation that has necessary relations with so many different units.

Management account is concerned with various levels of managers, supervisors and operators in all sections of business operations.

An organisational chart for a large scale concern is given below:

In the organisation chart, director finance is placed above chief management accountant. The functions like budgeting, auditing, O & M, credit control etc., are all placed under Chief Management Accountant.

10. State the application of computer in management decision making process.

Or

Discuss the role of computer in managerial decision making process.

Ans: Computer and its functions: A computer is an electronic data processing device. It can read, write, compute, compare, store and process large volume of data with high speed, accuracy and reliability and works on the instructions given to it. Once the data and instruction are fed into the memory (CPU), it obeys instructions and performs actions on the data and produces results.

Therefore a computer has three devices:

(i) Input device.

(ii) Processing device (CPU). and

(iii) Output device.

(i) Input device: They help the user to feed the instructions key Board, punch card Reader, Paper tape Reader speech Recognition system, Floppy Disk, Mouse.

(ii) Processing device: Processing device (Central processing Unit or CPU) does the computing function includes addition subtraction, division, multiplication and summarisation, etc. This device processes the data according to the instructions of user.

(iii) Output devices: Output device produces the results. Output devices are used for the processed values results from the computer. This device includes visual display unit, printers, plotters, Micro film recorders, etc.

Thus a computer records, stores, process and produces the desired information for the managerial persons at different levels at different times as per their requirements.

Role of computer in Managerial Decisions Making: In this MIS computer plays pivotal role because all information about the business can be fed, stored, processed and required information can be obtained quickly and accurately as and when needed. A computer functions like a storehouse of processed information for immediate needs and future reference. Thus different levels of management can use computer for various types of information as and when they require for the purpose of their decision making.

Different levels of Management and their information Need:

The function of management has been decentralised at:

(a) Lower Level Management or supervising level: Managers at this level deal with day to day operations or activities. Those activities include inventory control, pay roll, processing sales transactions, keeping track of employee work hours, etc. These are routine work and repetitive nature. They need feed back reports for the purpose of control and co- ordination.

(b) Middle level Management: Managers at this level are required to co-ordinate control and monitor various activities in an organisation. They act as a liason between lower management and top management.

(c) Top-level Management: Managers at this level are concerned with general direction of the company and long term planning of the organisation. They have to take decision on various strategic decisions and for the purpose they need adequate and reliable information about the affairs. They get this information from the data base of the computer.

11. Management Accounting has been evolved to meet the needs of management.” Explain this statement.

Ans: The term management accounting refers to accounting for the management. Management accounting provides necessary information to assist the management in the creation of policy and in the day-to-day operations. It enables the management to discharge all its functions i.e. planning, organisation, staffing, direction and control efficiently with the help of accounting information. The two principles serve the management accounting community and its customers – the management of businesses. The above principles are incorporated into the Managerial Costing Conceptual Framework (MCCF) along with concepts and constraints to help govern the management accounting practice. The framework ends decades of confusion surrounding management accounting approaches, tools and techniques and their capabilities.Management Accounting has brought out an apparent shift in the aim of accounting. The main emphasis is Management Accounting is on analysing and interpreting to assist the management to secure better results. In this way, Management Accounting eradicates intuition, which is not at all dependable, from the field of business management to the cause and effect approach. Major functions of the management include planning, organising, directing and controlling. Management accounting facilitates the performance of each of these functions in numerous ways.

12. Discuss various steps required for installing management accounting system.

Ans: The installation of management accounting system involves the following steps:

(i) Organization Manual: First of all organization manual should be prepared and adopted. This will clearly explain the duties and responsibility of various managerial levels in the organizational hierarchy.

(ii) Preparing Forms and Returns: The second step in installing management accounting system will be the designing and preparing of various forms and returns required for collection and presentation of information for management needs.

(iii) Requisite Staffing: The requisite staff should be recruited for making this system effective. The objectives are clear to everyone associated with this system.

(iv) Classifying accounts and integrating the system: The accounts are classified to facilitate collection and analysis of data. The financial and cost accounting system should be integrated.

(v) Introducing standard costing techniques: The technique of standard costing are introduced for setting up standards and recording the performance so that reasons for variations are ascertained and corrective measures are taken in time.

(vi) Setting up budgetary control system: Budgetary control system should be introduced to plan the activities of various departments.

(vii) Setting up operational research techniques: The business is operating under changing economic, political, and social environment. Everyday a new challenge is faced. The operational research techniques will be essential to cope with the need.

13. Difference between Cost accounting and Management Accounting.

Ans:

| Basis | Cost accounting | Management accounting |

| (i) Meaning | Cost accounting is a managerial accounting process that involves recording, analysing, and reporting a company’s costs. Cost accounting is an internal process used only by a company to identify ways to reduce spending. | Managerial accounting is the practice of identifying, measuring, analysing, interpreting, and communicating financial information to managers for the pursuit of an organisation’s goals. |

| (ii) Principles | Established procedures and practices are followed in cost accounting. | No such prescribed practices are followed in Management accounting. |

| (iii) Scope | Focused on distribution, allocation, determination and accounting factors of the cost. | Convey (impart) and effect factor of the cost. |

| (iv) Data | Cost accounting uses only quantitative information. | Management accounting uses both qualitative and quantitative information. |

| (v) Objective | It helps to control the operational Cost so that it does not exceed the budget constraint. | It helps to formulate efficient Management strategies. |

| (vi) Planning | It can be practised without employing a Management Account. | It cannot be applied without Cost Accounting. |

14. Enumerate the functions of a management accountant.

Ans: The functions of the management accountant are as follows:

(i) Planning for control: Management accountant establishes, co- ordinates and maintains an integrated plan for the control of operations.

(ii) Reporting: management accountant measures performance against given plans and standards. The results of operations are interpreted to all levels of management. This function will include installation of accounting and costing system and recording of actual performance so as to find out deviations, if any.

(iii) Evaluating: He should evaluate various policies and programmes. The effectiveness of planning and procedures to attain the objectives of the organization will depend upon the calibre of the management accountant.

(iv) Administration of Tax: Management accountant is expected to report to government agencies as required under different laws and to supervise all matters relating to taxes.

(v) Appraisal of External Effects: He is to assess the effects of various economic and fiscal policies of the government and also to evaluate the impact of other external factors on the attainment of organizational objects.

(vi) Protection of Assets: The protection of business assets is another function assigned to the management accountant. This function is performed through the maintenance of internal control, auditing and assuring proper insurance coverage of assets.

15. Discuss in detail the limitations of management accounting.

Ans: Limitations of management accounting are explained as follows:

(i) Based on records: The management accountant takes into consideration the past records provided by the financial and cost accounting while making decisions for future.

(ii) Lack of knowledge: The use of management accounting requires the knowledge of a number of related subject. For taking a sound decision it is necessary that the management must have knowledge of various field.

(iii) Intuitive Decisions: Though management accounting provides scientific analysis of various situations and enables decision taking based on facts and figures, there is a tendency to make decisions intuitively.

(iv) No substitute of administration: The techniques and tools suggested by the management accountant are not alternatives of good administration but in facts these are only to supplement the sound management and administration.

(v) Costly: The installation of a management accounting system in a concern requires large organization and a wide network of rules and regulations and thus requires a heavy investment.

(vi) Psychological Resistance: The installation of management accounting involves basic change in organizational set-up. New rules and regulations are also required to be framed which affect a number of personnel and hence there is a possibility of resistance from the staff on the other.

16. Write a detailed note on application of computer in management decision making process.

Ans: With the coming of the computer age, management information system is becoming popular in the corporate circle for giving quick information to the management. The purpose of MIS is reporting and is to provide the necessary information to manager and supervisors at various levels to help them to discharge their functions in decision making.

MIS is a scientific way of collecting, processing, storing and communicating information relating to the various activities of an organization to the various levels of management so that management may be facilitated in discharging its function efficiently and run the organization in an efficient way for the betterment of all.

Management Information System (MIS) is an approach of providing timely, adequate and accurate information to the right person in the organization which helps in taking right decisions. So, MIS is a planned and organized approach to the transferring of intelligence within an organization for betterment of management.

MIS is of two types:

(i) Management operating system meant for meeting the information needs of lower and middle level management. The information supplied generally relates to operations of the business.

(ii) Management reporting system which supplies information to the top level management for decision making. The information is presented in a way which enables management to take quick decisions.

17. Explain the essentials for success of Management Accounting Systems.

Ans: Management accounting system must possess the following features:

(a) Simplicity: It must be simple, flexible and adaptable to the changing conditions. And it must be easily understandable to the various levels of management. The information provided must be in the proper order, in the right time and to the right persons so as to be utilised fully.

(b) Budgeting: Budgeting is a critical technique that involves setting financial goals and allocating resources to achieve them. By creating budgets for specific departments or projects, organisations can monitor performance, identify variances, and make adjustments to ensure financial targets are met.

(c) Cash Flow Analysis: Cash flow analysis is a technique that involves monitoring the inflows and outflows of cash within an organisation. By analysing cash flow patterns, management accountants can identify potential liquidity issues and take proactive measures to ensure a healthy cash position.

(d) Economy: The management accounting system must suit the finance available. The expenditure must be less than the benefits derived from the system adopted.

(e) Overall Efficiency of management Accountant: The work of the management accountant under a good system of management accounting must be clearly defined as his duties and responsibilities to the firm are very essential.

(f) Business Asset Protection: The management accountant is responsible for the funds required to maintain, replace and repair the fixed assets available in the organisation. It is necessary for the smooth and uninterrupted flow of production, which may adversely affect the company’s profits. The finance required for fixed asset insurance also comes under the management accounting function.

18. Explain the Advantages/ Merits/ Uses of Management Accounting.

Ans: Management Accounting is of immense value and utility for the management of any firm and it has been considered as indispensable, particularly in large organisations where the task of Management is complex.

The following can be listed as the benefits or uses of Management Accounting:

(a) Increase in Efficiency: Management accounting contributes significantly towards increasing efficiency in operations of a firm. Budgets, standards, reports etc., usually elevate the level of performance.

(b) Effective Planning: Policy formulation and planning of operations become more effective through the ‘decision data’ provided by Management Accounting.

(c) Performance Evaluation: Evaluating performance of employees, departments, etc., is facilitated by Management accounting through Variance Analysis, control ratios etc.

(d) Profit Maximisation: Management accounting is helpful in profit planning to pursue decisions which can optimise profits.

(e) Reliability: The Tools used by Management accounting usually make the data supplied to Management accurate and reliable.

(f) Elimination of Wastages: Standard costs, Budgets, cost control techniques, etc., contribute towards elimination of wastages, production of defectives etc.

(g) Effective Communication: Regular and systematic reporting ensures constant flow of information about operations to various levels of Management.

(h) Employee Morale: Morale of employees can be created and sustained through attainable standards, practical budgets and incentive schemes.

(i) Control and Co-ordination: Control on costs and co-ordination in the efforts of different segments of an organisation can be achieved through performance reporting, variance analysis and follow up action etc.

The greatest benefit of Management accounting is its advisory role in making the Management to take the best possible decisions on a day-to- day basis on routine matters and also vital policy matters.

19. Write the steps involve in Installation of Management Accounting System:

Ans: Installation of Management accounting system involves the various following steps:

(a) Organisation Manual: The first step is to prepare an organisational manual. The manual will clearly pin point the duties and responsibilities of each level of management and the horizontal and vertical relationship among the key personnel.

(b) Preparation of Various Forms and Reports: The second step in the installation process is designing the perform of various and reports. The objective should be to minimise their under and simplify them to avoid ‘Bureaucratization’.

(c) Requisite Staffing: The staff required for implementing the system is to be recruited and trained.

(d) Classification of Accounts: Financial and cost accounts should be classified, confined and integrated to the extent possible to suit the requirement of management accounting.

(e) Setting Up of Cost Centres: Investment centres, profit centres, cost centres and budget centres are to be clearly set up so that information can be collected and analysed in relation to each of them.

(f) Introducing Management Accounting Techniques: Various techniques of management accounting are to be introduced, based on the needs of the firm, and practicability.

(g) Providing for Usage of ‘Operations Research’ (O.R) Techniques: Everyday new challenges are faced because business is operated under changing economic, political and social environment.

20. Difference between Financial Accounting and Management Accounting.

Ans:

| Basis | Financial accounting | Management accounting |

| (i) Meaning. | An accounting system that helps in classifying, analysing, summarising, and recording a company’s financial transactions. | An accounting system that helps in collecting, analysing, and understanding the financial, qualitative, and statistical information ultimately helps the management in making effective decisions regarding the business. |

| (ii) Data. | Financial accounting is mainly concerned with the recording of past events. | Management accounting is concerned with future plans and policies. |

| (iii) Publishing and auditing. | Required to be published and audited by statutory auditors. | It is not meant to be published or audited. It is for internal use only. |

| (iv) Application. | It helps in showing a true and fair picture of the financial position of an organisation. | It helps the management in making meaningful decisions and strategizes accordingly. |

| (v) Nature. | Financial accounting is based on measurement. | Management accounting is based on judgment. |

| (vi) Rules. | Rules of GAAP are followed. | No fixed rules for the preparation of reports. |

Hi! my Name is Parimal Roy. I have completed my Bachelor’s degree in Philosophy (B.A.) from Silapathar General College. Currently, I am working as an HR Manager at Dev Library. It is a website that provides study materials for students from Class 3 to 12, including SCERT and NCERT notes. It also offers resources for BA, B.Com, B.Sc, and Computer Science, along with postgraduate notes. Besides study materials, the website has novels, eBooks, health and finance articles, biographies, quotes, and more.