Indian Banking System Unit 1 Banking Meaning and Definition, College and University Answer Bank for BA, B.com, B.sc, and Post Graduate Notes and Guide Available here, Indian Banking System Unit 1 Banking Meaning and Definition to each Unit are provided in the list of UG-CBCS Central University & State University Syllabus so that you can easily browse through different College and University Guide and Notes here. Indian Banking System Unit 1 Banking Meaning and Definition can be of great value to excel in the examination.

Indian Banking System Unit 1 Banking Meaning and Definition

Indian Banking System Unit 1 Banking Meaning and Definition Notes cover all the exercise questions in UGC Syllabus. Indian Banking System Unit 1 Banking Meaning and Definition provided here ensures a smooth and easy understanding of all the concepts. Understand the concepts behind every Unit and score well in the board exams.

Banking Meaning and Definition

INDIAN BANKING SYSTEM

| VERY SHORT TYPES QUESTION & ANSWERS |

A. Multiple choice question and answers:

1. We should keep our savings with banks because ―

(a) It is safe.

(b) Earns interest.

(c) Can be withdrawn anytime.

(d) All of above.

Ans: (d) All of above.

2. Bank does not give loan against ―

(a) Gold Ornaments.

(b) LIC policy.

(c) Lottery ticket.

(d) NSC.

Ans: (c) Lottery ticket.

3. Bank having maximum number of branches in India –

(a) Reserve Bank of India.

(b) State Bank of India.

(c) Punjab National Bank.

(d) Bank of Baroda.

Ans: (b) State Bank of India.

4. 100/- Rupee note is signed by-

(a) Prime Minister.

(b) Finance Minister.

(c) RBI Governor.

(d) None of above.

Ans: (c) RBI Governor.

5. Bank does not provide loans for-

(a) Crop loans.

(b) Education loans.

(c) Home loans.

(d) (d) Drinking & Gambling.

Ans: (d) Drinking & Gambling.

6. Bank Pass Book is-

(a) Issued by Bank.

(b) Contains transaction details of Bank account.

(c) Shows balance in account.

(d) All of above.

Ans: (d) All of above.

7. Banks pays interest on-

(a) Deposits.

(b) Loans.

(c) Both (a) & (b).

(d) None of above.

Ans: (a) Deposits.

8. Currency notes are issued by-

(a) RBI.

(b) NABARD.

(c) Public sector banks.

(d) Central Government.

Ans: (a) RBI.

9. Coins are issued by-

(a) Government of India.

(b) NABARD.

(c) Public sector banks.

(d) State Bank of India.

Ans: (a) Government of India.

10. Which bank is known as banker’s bank?

(a) RBI.

(b) SBI.

(c) PNB.

(d) NABARD.

Ans: (a) RBI.

B. Fill in the blanks:

1. The bank of venice was established in _____________.

Ans: 1157.

2. The lead bank scheme introduced by the Reserve Bank of India towards the end of _____________.

Ans: 1969.

3. The Reserve Bank of India Act was passes in ______.

Ans: 1934.

4. Scheduled Banks are those banks which are included in the _____________ of the R.B.I. Act.

Ans: Second Schedule.

5. The imperial bank of India nationalized in 1955 and renamed as _____________.

Ans: State Bank of India.

6. The bank of England was founded in _____________.

Ans: 1694.

7. RBI ACT was comes in to existence _____________.

Ans: 1934.

8. Banking Regulation Act was comes into existence _____________.

Ans: 1945.

9. _____________ Section of the Negotiable Instruments Act defines a bill of exchange.

Ans: Section 5.

10. _____________ controls the credits in an economy.

Ans: Central Bank.

C. Answer the following:

1. State any one importance of Banking system.

Ans: Banking system offers many facilities to the people like Core banking, Electronic Fund Transfer, Tele-banking, Anywhere banking, Mobile banking etc.

2. State any one function of a Bank.

Ans: Bank accepts deposits from the public for the purpose of lending or investments.

3. Why are pay-in-slips used in Banks?

Ans: Pay-in-slips are used to deposit cash or cheques into the Bank account of the account holder.

4. Mention any one need of Bank.

Ans: Bank is needed to transfer funds from place to place by means of Bank drafts and cheques.

5. Name any one type of Bank account.

Ans: Savings Bank account.

6. Mention any one use of Core-Banking.

Ans: Core baking is useful to conduct banking business any where and at any time.

7. Give any one advantages of Tele Banking.

Ans: Tele banking is useful to get information about Bank balance available.

8. State any one facility under Anywhere Banking.

Ans: Any where banking facilitates to operate customers account from any branches of the bank at any place and at any time.

9. State any one services of Mobile Banking.

Ans: Mobile banking helps for easy transfer of funds from one branch to another branch within no time.

10. Give a difference between Current account and Savings Bank account.

Ans: Bank provides no interest to Current account holders. Bank provides 3% to 4% interest to Savings bank a/c holders.

11. State a difference between Current account and Fixed Deposit account.

Ans: Bank provides Overdraft facility to the Current account holders. Bank does not provide such overdraft facility to the Fixed Deposit account holders.

12. Mention a difference between Savings Bank account and Fixed Deposit account

Ans: S.B account is suitable for low and middle income group of people. F.D. account is suitable for wealthy people and small investors.

13. Expand EFT.

Ans: Electronic Fund Transfer.

14. Give expansion form of SMS.

Ans Short Messaging Services.

15. Expand ATM.

Ans: Automated Teller Machine.

| SHORT TYPE QUESTION & ANSWERS |

1. Write any two types of Bank account.

Ans: (a) Savings Bank account.

(b) Current account.

2. Give the meaning of Current account.

Ans: Current account is a type Demand Deposit Bank account opened with the object of operating business Bank transactions continuously. Usually, this type of account is opened by Business people so as to conduct their transactions smoothly.

3. Give the meaning of Savings bank account.

Ans: Savings Bank account is kind of demand deposit Bank account opened with the object of saving the money out of the earnings of the people. Usually, this type of account is opened by students, salaried people, agriculturists, lower and middle income groups.

4. Give the meaning of Fixed deposit account.

Ans: Fixed deposit account is a type of term deposit bank account opened with the object of investing money on bank deposits at higher rate of interest. Usually, this type of account is opened by wealthy people and small investors who want safety for their investments.

5. Give the meaning of Recurring deposit account.

Ans: Recurring deposit a/c is a type of term deposit bank account in which deposits are made every month regularly and withdrawn at the end of some period. In this account, account holder deposits fixed amount every month and withdrew entire amount in lump sum at the end of certain period.

6. Give a brief idea about the Reserve Bank of India.

Ans: At the head of the Indian banking structure is the Reserve Bank of India which is the central banking institution of the country, brought into existence by the Reserve Bank of India Act, 1934. The Reserve Bank was started as a shareholder’s bank with a paid-up capital of Rs. 5 crores. It was nationalized in 1948 on establishment, it took over the function of management of currency from the Government of India and power of credit control from the then Imperial Bank of India.

7. Define “Banker”.

Ans: Section 3 of the Negotiable Instrument Act merely says that a banker includes ‘any person acting as a banker’. Such persons may include even firms or individuals who accepts current deposits withdrawal on demand, collect cheques for credit of customer’s accounts, and lend by way of overdrafts or loans.

Again in terms of Section 2 (2) of the Bankers’ Books Evidence Act, any company or corporation carrying on the business of bankers can be regarded as a ‘bank’ or ‘banker.’

8. What are the main provisions of the Nationalizing Act?

Ans: The long title of the Act reads: “An Act to provide for the acquisition and transfer of undertaking of certain banking companies having regard to their size, resources, coverage and organization, in order to control the heights of economy and to meet progressively, and serve better, the needs of development of the economy in conformity with national policy and for objectives and matters connected therewith or incidental thereto”.

9. Write in brief about the organizational structure of the State Bank of India.

Ans: The organizational structure of the State Bank is highly systematic. The entire country has been divided into nine circles for the purpose of proper administration.

The Head offices of each circle is known as Local Head office comprising of Local Board of Directors. The Local Board of Directors have the statutory status. Again, each circle has be divided in a number of Regions. There is a chief General Manager for each circle and he is the Chief Executive for his circle. Under him there is the Regional Manager for the different regions in his circle. The Chief General Manager has the power to control entire branches and can take decisions regarding the matter of loans and advances.

10. Define customer.

Ans: A customer is a person who has the habit of resorting to the same place or person to do business.

According to Lord Davey, a customer is a person who has some sort of an account either deposit or current account or some similar relation with a banker and from this it follows that any person may become a customer by opening a deposit or credit current account or by accepting an advance on current or loan account, or even by accepting a deposit receipt in acknowledgment of money left with the banker.

According to Sir John Paget “If a man obtained from a bank an agreed overdraft never paying in but giving good security and paying interest and drawing cheques on the account, he would presumably become a customer.”

So, to be a customer of a bank, a person must have some sort of account with the bank or some similar relation with the banker.

11. What are the essential features of a Bank?

Ans: The essential features of Bank or banking business as defined in Section 5(b) of the Banking Regulation Act are:

(i) Acceptance of deposits from the public.

(ii) For the purpose of lending or investment.

(iii) Repayable on demand or otherwise and

(iv) Withdrawable by means of any instrument whether a cheque or otherwise.

This definition has Proved workable and flexible for the purposes of the Banking Regulation Act. It has never been challenged before any court.

In modern times also bank, can be referred to an institution having the following important features:

(i) Bank deals with money, it accepts deposits and advances loans.

(ii) Bank deals with credit and has the ability to create credit also.

(iii) Bank is a commercial institution, its main aim is to earn profit.

(iv) Bank can create demand deposits which serve as a medium of exchange and ultimately bank has to manage the payment system of the country.

So, a modern bank has to perform a variety of functions. Among the agency functions of banks, remittance of funds, Purchasing and Sale of Securities, Collection of Dividends on Shares, Acting as Trustee and Executor, Income Tax Consultancy are the main functions in recent times.

Sale deposits Locker facility, letter of Credit, collection of Statistics, Gift cheques and Foreign Exchange Business are also some of the important general utility functions of a modern commercial bank. So, no other institutions can be referred as bank as they do not posses. The above mentioned features which a modern bank can only posses.

12. Discuss the role of commercial bank in a developing economy.

Ans: Banks now-a-days provide a variety of services. Banks have been financing small borrowers in industry and agriculture for many years. However, small borrowers in other sector and fields did not receive much attention until the nationalisation. But after nationalisation, there has been a massive growth in banking facilities both in rural and urban areas and small borrowers. Traders received much attention from the banking institutions. So, a well developed banking system is extremely necessary for economic development a modern economy. Commercial banks have greater role to far.

The country’s economic development in the following way:

(i) Formation of capital-Banks can help to Promote capital formation: Capital formation can be done by, generating the saving, mobilising the saving and canalising the savings by productive uses. A modern commercial bank now-a-days Perform a greater role in capital formation and helps the economy as a social and financial institution.

(ii) Helps to influence Economic Activity: A modern bank has a greater role to play to influence economic activity. Bank determines the availability of credit and the rate of interest in a modern economy.

(iii) Variation in Interest Rates: When banks reduce interest rate, the investment becomes high. An increase in the interest rate, on the other hand discourages investment and economic activity. So, at the time of deflationary situation, banks generally follow cheap money policy with low interest rates and at the time of inflation banks adopt dear money policy with higher rates of interest:

(iv) Implementation of proper Monetary Policy: A well developed banking system is very essential for the effective implementation of the monetary policy. Monetary authority of a country can control and regulate the credit only with the active cooperation of the banking system in the country.

(v) Remove Regional Imbalances: Banks help to remove regional imbalances. Banks can transfer surplus capital from the developed regions to the less-developed regions and try promote economic development in underdeveloped areas of the economy.

(vi) Helps to Promote Agriculture Sector: Rural economy is basically the agricultural one. Therefore banks have been paying more attention to the rural areas by providing various medium and short-term loans to the needy borrowers.

13. Write Notes on:

(a) Industrial Development Bank of India (IDBI).

Ans: The Industrial Development Bank of India: is the open financial institution in the field of development banking in the country the IDBI was established in 1964. At the time of its establishment it was a wholly owned subsidiary of the Reserve Bank of India. But in 1976, it was de-linked from the RBI.

Initially, the authorized capital of the bank was 50 crores. The IDBI has a Board of Directors appointed as follows:

(i) A Chairman and a Managing Director appointed by the Central Government.

(ii) One whole time director appointed by the Central Government on the recommendation of the board only.

(iii) Two directors shall be officially nominated by the central government.

(iv) Three directors nominated by the Central Government having knowledge and professional experience in economics, banking, marketing etc.

The main objective of IDBI is to provide term finance for industry in the country.

The bank makes plans, to promote and develop industries to fill the gaps in the industrial structure in India.

Bank also provides technical and administrative assistance for promotion, management or expansion of industries, moreover. The bank also undertakes market and investment research for the development of industries.

(b) National Bank for Agriculture and Rural Development (NABARD).

Ans: National Bank for Agriculture and Rural Development (NABARD): The national Bank for agriculture and Rural Development was established by an Act of Parliament and it came into existence on July 12. 1982. It is an apex refinancing agency provides financial assistance to agriculture, small scale industries, artisans cottage and village industries etc.

NABARD is managed by a Board of Directors, consisting of a chairman, a managing director, three Directors from the Reserve Bank, three Directors from the Government of India and two Directors representing the State Governments.

The paid UP capital of NABARD was 500 crores. The bank provides short term assistance to the state cooperative banks for seasonal agricultural operation. Decide this, the bank also provides medium term assistance to state and central cooperative banks for converting short term agricultural finance into medium term finance to the areas which are affected by natural calamities. The banks also provides financial assistance to less developed states like, Uttar Pradesh, Madhya Pradesh, Orissa and Rajasthan. Moreover the bank Provides financial help for production and marketing activities of cottage and small scale industries co-operative sugar mills, rural artisans etc.

(c) Industrial Finance corporation of India (IFCI).

Ans: Industrial finance corporation of India (FICI): The first of the development banks was the Industrial Finance Corporation of India brought into existence by the Industrial Finance corporation of India Act, 1948. It Provides financial assistance to large scale industrial concerns, organized as public limited companies or co-operative societies, when normal banking accommodation is inappropriate or recourse to the capital market is not Practicable.

The management of the corporation vests in a board of Directors appointed as follows:

(a) 3 No’s of Directors, nominated by the Central Government.

(b) 3 No’s of Directors, nominated by the Reserve Bank.

(c) 6 No’s of Directors, elected by banks, insurance companies, Investment trusts and cooperative banks.

The paid up capital of IFCI was 353 crores while resources and funds aggregated to Rs. 1283 crores.

The corporation undertakes the issue of stocks, bonds or debentures issued by industrial concerns.

The corporation also undertakes financing of projects with the Industrial Development Bank of India and other financial institutions.

IFCI Provides financial help for setting up new industrial Projects, renovation, modernization, diversification and expansion of existing ones the corporation also provides financial assistance on concessional basis for setting up industrial projects in industrially backward districts in the state and union territories.

(d) State Finance corporation (SFCs).

Ans: State Finance Corporations: In order to meet the various financial requirements of small and medium sized industries, the Government of India Passed the State Finance Corporations. Act in the year 1951.

The important functions of SFCs are:

(i) SFCs provide long term finance to small scale and medium sized industrial enterprises which organized as public or private companies, partnership, proprietary business or corporations etc.

(ii) SFCs underwrite the issue of shares, stocks, debentures and bonds by industrial concerns.

(iii) SFCs guarantee the deferred payments for the purchase of plant, machinery etc. within the country.

(iv) SFCs extend loans and advances to the industrial enterprises repayable within a period of 20 years.

(v) SFCs subscribe to the debentures of industrial enterprises repayable within 20 years.

(vi) SFC’s can act as an agent of the central or state Governments for sanctioning and disbursing loans to small industries.

The capital of SFCs has to be fixed up by the state Government within the minimum and maximum limits of Rs.50 lakhs to Rs 5 crores. The shares of SFC are held by the respective state governments, Rs. 1, scheduled banks insurance companies, investment trusts etc.

(e) State Industrial Development corporations (SIDCs).

Ans: State Industrial Development corporations: SIDCs were established during the period of 1960s and early 1970s under the companies Act. 1956. The corporations were basically established mainly for the promotion and development of medium and large scale industries.

SFCs Provide term finance to the industrial concerns: SFC’s also provide various promotional activities like entrepreneurship development programmes, preparation of feasibility reports and development of industrial areas the corporations also engaged in setting up of various medium and large sized industrial projects as wholly owned subsidiaries.

There are 18 Financial corporations in the country since their inception, till the end of March 1996, the sanctions and disbursements by all these SFCs amounted to Rs. 22,893 crores and Rs. 17,952 crores respectively.

The Special features of the lending operations of SFCs has been the provision of finance to industrial concerns of backward areas. Moreover, in order to encourage self employment, the SFCs have launched schemes of assistance to technician entrepreneurs.

14. Write a note on Monetary Policy of the Reserve Bank.

Ans: Monetary Policy is a policy which employ’s central bank’s control over the supply, cost and use of money as an instrument for achieving the certain given objectives of economic policy. Since the common objectives of economic policy are the attainment of full employment, price stability, balance of payments equilibrium and rapid economic growth. The effectiveness of monetary policy will depend upon the degree to which it succeeds in achieving these objectives. The Reserve Bank influences the total amount and cost of credit primarily by attesting the cash reserves position of commercial banks in the country.

In other words, Monetary Policy is the policy of the central bank of a country to regulate and control the volume, cost and allocation of money and credit with this aim if achieving the objectives of optimum level of output and employment, price stability, balance of payment equilibrium, or any other goal set by the government.

In a developing economy, monetary policy is highly indispensable and can play a positive role incentive conditions necessary for proper and rapid economic growth in India, the aim of the monetary policy of the Reserve Bank has been to meet the needs of the planned development of the economy basically during the planning period. The major aim of government,

(a) To accelerate the process of economic growth with a view to raise natural income. and

(b) To combat and reduce the inflationary pressures in the economy were the major objectives of the economic policy of the government.

At Present the monetary policy of the country has strictly followed the following objectives i.e. to enhance the supply of bank credit in adequate quantity to industry trade and agriculture and also to provide special financial help to the weaker sections of the society. Secondly the monetary policy of RBI is trying best to maintain price stability by controlling the credit supply to the optimum level.

15. What were the basic reasons for nationalization of the Reserve Bank of India.

Ans: The basic reason for nationalization of the Reserve Bank of India after independence in the year 1948 were as follows:

(a) After the end of the second world war a trend began for nationalization of the central Bank of the country in all parts of the world. Even the bank of England was also nationalized in the year 1946. So, this trend towards the nationalization of central bank of the country an all parts of the world was can be supposed as the main reasons for nationalization of the Reserve Bank of India.

(b) Starting of inflationary tendencies just after second world war was also another cause of nationalization of the Reserve Bank as the central bank of the country is fully responsible for credit and currency management.

(c) Country had to prepare a planned economic programme after independence. Nationalization of the Reserve Bank India was necessary to use it as an effective instrument for economic development of the country.

16. Write a note on the State Bank of India.

Ans: The State Bank of India, which is the biggest commercial bank is in a class by itself. Prior to the inauguration of the Reserve Bank of India, it performed certain central banking functions, in particular, acting as banker to Government. It was then known as the Imperial Bank of India, having been formed in 1921 by the amalgamation of the Bank of Bombay, Bank of Madras and Bank of Bengal, which were known as Presidency Banks.

The Imperial Bank nationalized be the passing of the State Bank of India Act, 1955 which was brought into force with effect from the 1st July 1955. Over 90% of the shares of the State Bank of India are held by the Reserve Bank of India and rest by private shareholders.

Subsidiaries of the State bank of India.

There are 7 subsidiaries of the State Bank of India, Whose names are as follows:

(a) State Bank of Bikaner Jaipur.

(b) State Bank of Hyderabad.

(c) State Bank of Indore.

(d) State Bank of Mysore.

(e) State Bank of Patiala.

(f) State Bank of Saurashtra.

(g) State Bank of Travancore.

The subsidiaries of the State Bank of India are now referred to as “Associate Banks”. These Bank are governed by the State Bank of India (Subsidiaries) Act, 1959 which was passed in order to provide for the formation of certain Government and Government – Associated banks out of those constituted by the forever Governments of the bigger Princely states of India. Their operations are mainly concentrated in the area denoted by their names. As these are the subsidiaries of the State Bank of India, The latter has the power to give directions and instructions to them in regard to any of their affairs or business and they are bound to comply with the directions and instruct one so given.

17. What is the meaning of “Transfer of the undertakings of the 14 banking companies”?

Ans: Under Section 3 of the Act as on 19-07-1969 14 new banks with all the legal characteristics of body corporate are established. Each of the new banks has common Seal and perpetual succession and subject to the Provisions of the Act is empowered to acquire, had and dispose of the property, to contract, and to sue and be sued in its own name. The undertakings of each of the 14 major banking companies stands vested in and transferred to each of the 14 corresponding new banks from 19-07-1969. Each of the 14 new bank bear the same name as the corresponding old bank except that the words “The” and “Limited” of the corresponding old banks are removed.

The paid-up capital of each new bank shall be equal to the paid up capital of the corresponding banks company and it shall stand vested in and allotted to the Central Government on 19-07-1970. Each new bank shall have a reserve fund to which shall be transferred the share premium and the balance, if any, standing to the credit of the Reserve Fund of the corresponding banking company and such further same as may be transferred under Sec. 17 of the Banking Regulation Act.

18. Give the definition of “Undertaking”.

Ans: Section 5 (1) of the Banking Companies (Acquisition and Transfer of Undertakings) Act, 1970 reads.

“The undertaking of each existing bank shall be deemed to include all assets, rights, powers, authorities and privileges and all property movable and immovable, cash balance, reserve funds, investments and all other rights and interests in or arising out of such property as were immediately before the commencement of the Act in the ownership, possession, power or control of the existing bank in relation to the undertaking whether within or without India, and all books of accounts, registers, records and all other documents of whatever nature relating thereto and shall also be deemed to include all borrowings, liabilities and obligations of whether kind then subsisting of the existing bank in relation to the Undertaking”.

Anything and everything the 14 banking companies were doing and all the tools, instruments, ways and means by which they were functioning are taken over. The banking companies have now nothing which Previously belonged to them. They are given compensation of specified amounts in consideration of the take over.

19. List the Constituents of the Indian banking system.

Ans: The constituents of the Indian Banking System can be broadly listed as under:

(a) Commercial Banks:

(i) Public Sector Banks.

(ii) Private Sector Banks.

(iii) Foreign Banks.

(b) Cooperative Banks:

(i) Short term agricultural institutions.

(ii) Long term agricultural credit institutions.

(iii) Non-agricultural credit institutions.

(c) Development Banks:

(i) National Bank for Agriculture and Rural Development (NABARD).

(ii) Small Industries Development Bank of India (SIDBI).

(iii) EXIM Bank.

(iv) National Housing Bank.

20. Write the Functions of Indigenous Bankers.

Ans: The following are their functions:

(a) They receive deposits for a fixed period at a higher rate of interest.

(b) They advance loans against security of and, jewelry, crops, goods promissory notes etc.

(c) They write, sell and buy hundis, which are bills of exchange.

(d) They finance both wholesale, and retail traders.

(e) They engage in speculation of food and non-food. crops and other articles of consumption.

(f) They act as commission agents to firms.

(g) Some non-professional indigenous bankers run their own manufacturing or service firms.

(h) Some indigenous bankers provide long-term finance by subscribing shares and debentures of large companies.

The borrowers find it easy to get finance from indigenous bankers because of the following reasons:

(i) Less formality.

(ii) No fixed banking hours.

(iii) Borrowers approach them directly and informally.

(iv) These types of bankers insist on punctuality of repayment.

22. What are the objectives of RBI?

Ans: Reserve Bank of India was established in 1935. It is the central bank of India.

The following are the main objectives of RBI:

(a) To manage and regulate foreign exchange.

(b) To build a sound and adequate banking and credit structure.

(c) To promote specialized institutions to increase the term finance to industry.

(d) To give support to government and planning authorities for the economic development of the country.

(e) To control and manage the banking system in India.

(f) To execute the monetary policy of the country.

| LONG TYPE QUESTIONS & ANSWERS |

1. Give the meaning of Bank. Explain the Features of a bank or banking system.

Or

Define ‘Bank’/ ‘Banking’. Explain the Features of a bank or banking system.

Ans: A bank is a social and financial institution which deals with money and credit. It also accepts deposits from the public, and makes the funds available to those who need them. A modern bank performs variety of functions, so it is very difficult to give a clear definition of it.

Prof. Sayers defines bank as “an institution whose debts (bank deposits) are widely accepted in settlement of other people’s debts to each other.” Again according to him “ordinary banking business consists cash for bank deposits and bank deposits for cash, transferring bank deposits from one person or corporation to another, giving bank deposits in exchange for bills of exchange, government bonds, the secured promises of businessmen to repay and so forth.”

According to Sec 5 (b) of the Banking Regulation Act 1949 banking means “the accepting for the Purpose of Lending or investment, of deposits of money from the public, repayable on demand or otherwise, and withdrawable by cheque, draft order or otherwise.

According to Sir John Paget, “Nobody can be a banker who does not

(i) take deposit accounts.

(ii) take current accounts.

(iii) issue and pay cheques. and

(iv) collects cheques-crossed and uncrossed for its customers”.

Again according to Crowther, a bank “collects money from those who have it to spare or who are saving it out of their incomes and it lends this money to those who require it.

So from the above definitions, it is clear to us that a bank deals with money and credit and also provides a variety of services to the society.

The different features of a bank in detail to establish a better understanding of the banking system :

(i) Deals with money: The Main Features of a bank is that it deals with all the money-related transactions. For example, you can deposit your money in a bank account to save it securely, and you will also get interested in the money that you will save in the account. Therefore, it is the easiest way to increase your money without putting it at any risk. Moreover, if you need the money, then you can borrow it from the bank at a certain interest. For example, you can borrow money from the bank to pay your tuition fees as well as you can also borrow money from the bank you want to buy a car. However, you are supposed to pay the money back to the bank with interest.

(ii) Provide loans: Banks make extra money by providing loans for different products to the loan. The bank makes the extra money by lending money to the eligible person at certain rates. Nowadays, banks provide loans for various requirements such as study loan, car loan, home loan, personal loans, etc. Different banks provide different loans at different interest rates. You can compare the interest rates of different banks to get a loan at minimum interest rates.

(iii) Identity: As I told you, there are various banks which provide loans at different interest rates. Therefore, each bank has a different name which helps the people to identify it easily and to differentiate with other banks. Even though the basic services provided by all banks are the same, but each bank tries to provide different interest rates and better services to attract more and more customers. Therefore, each bank uses a unique bank name and unique tag line to sell their services.

(iv) Withdrawal and payment facilities: A Bank provides various payment and withdrawal services to customers so that they can receive their money hassle-free. Customers can withdraw money using cheques and drafts and also from the ATMs installed by the banks at different locations in the city. They can withdraw money using the debit cards provided by the bank the card is directly linked with the bank and customers can withdraw money anywhere in the world without going to the bank and even without carrying their passbook.

(v) Internet services: Another feature of a Bank is that modern banks are also providing internet services. The development of the internet and its inclusion in the banking sector has made it even more easy for people to carry out various transactions. Banks are providing online services through their apps. You can pay bills, buy food, go shopping without having cash with you. With the help of banking apps, you can pay for everything online.

Nowadays, more and more banks are taking their business online. It helps in making safe and risks free transactions, and there are fewer chances of stealing taxes. There are specific terms for these types of transactions, such as internet banking and mobile banking.

(vi) Business: The only work of banking is not to provide banking services to customers. All banks are involved in the subsidiary businesses to make more money. Their sole responsibility to provide maximum satisfaction to their customers and to provide them maximum interest rates so that more customers do banking with them. The money is passed from one hand to another to make a profit.

(vii) Increasing functionality: Like other industries banking sector is also focused on enhancing their functionality. Banks have developed from just providing money lending and cash deposit and withdrawal services to providing loans and credit to cashless bank services to internet and mobile banking. It is one of the fields which are growing fastest. It will not be wrong to assume that banks will be providing more services in the future in addition to internet banking and mobile banking and people’s dependency on the cash will reduce to almost zero percent.

(viii) Branches at different locations: Also, the features of a bank include services to its customers wherever they live in the whole world. Most banks are opening their branches the rural part of the country to connect people with the banks and to gain more profit. People are not required to travel miles like the old times to do banking. They can visit the nearest branch to them. Each bank is opening more and more branches. with the increase in the population so that they can-satisfy their customers properly by being near to them.

(ix) Bank can be a company or an individual providing banking services: Usually, when you hear about the word bank, you think about a large place where many people are working and dealing with the money transactions. But it is not wrong to say that a bank can be large organization consist of hundreds of people or it can be a unit managed by a single person.

(x) Commercialized: All the banking services are taking place with a single AIM to make money. You might feel perplexed how bank money by managing others money. But this is the key. We hand over our money for a small interest on the money deposited by us. The bank uses our money to lend it to others or by investing it in profitable businesses to make profits. If you think your money is sitting in a banks locker, then you are wrong.

2. Explain the procedure of opening a new bank account. What are the Types of Banks in India? Explain.

Ans: Following procedure is followed to open a new Bank account:

(a) Filling up of account opening form: First of all the banker asks the applicant to fill up the account opening form. The prospective customer should fill up all details such as name, address, type of a/c he wants to open, nominee details, pan card no. etc. He should also give address proof and pan card xerox copy and passport size photograph to open a new bank a/c.

(b) Obtaining introduction or reference: Secondly, the bank asks for proper introduction of respectable person known to the banker. This introduction is necessary to open S.B. a/c and Current a/c only and not for F.D. a/c and R.D. a/c. This introduction helps the banker to open a/c in the name of genuine persons and prevents to open falls a/c.

(c) Obtaining Specimen signature: If the banker is satisfied with introduction, he permits the prospective customer to open an a/c by obtaining 3 specimen signature on a specimen signature card. This specimen signature helps banker for cross verification of customer signature at the time of withdrawal of cash by cheque.

(d) Obtaining Mandate: If the customer wants to operate his a/c through his representative (agent), the bank take written authority from the customer which is known as ‘Mandate’. The banker should also obtain specimen signature of that agent.

(e) Receiving initial Deposit and open a/c in the ledger: After observing all above formalities the banker receives initial deposits from the customer and opens an a/c in the name of customer by writing details in the ledger of the bank.

(f) Supply of pay-in-slips, cheque book and pass book: Finally, the banks supplies pay-in-slip book for deposit of cash or cheque into bank, cheque book for withdrawal of cash from the bank and pass book showing the details of deposits, withdrawals and available balance: At the time opening a new bank a/c, the customer may request the bank for supply of ATM card and online transaction facility.

In India, there are many ways, through which banking may be done. To facilitate this, there are different types of banks on the market in India. Below is the list of types of banks in India:

(a) Central Bank: RBI is the central bank in India that governs and regulates the other banks working throughout the country. Central Bank guides the other banks, issue currency, implement the monetary policies and supervise the financial system. It is also called the banker’s bank.

(b) Commercial Bank: Commercial banks were regulated under the Banking Regulation Act, 1949 to operate on a commercial basis and earn a profit. These banks have a unified structure and can be run by any government or private entity and tend to all sectors whether rural or urban.

Types of Commercial Bank are:

(i) Public Sector Banks: In public sector banks, Government or the RBI are the major stake owners. These banks are nationalized and a large part of the Indian banking system revolved around this sector. These nationalized banks cover about 75 percent of the total banking business in India. Indian government holds the majority of its stakes in these banks. The largest bank in the public sector is SBI (State Bank of India). India has now 12 nationalized banks.

(ii) Private Sector Bank: In these banks, private organization or the group of people owns the stakes. These banks also have to follow the rules and regulations set by RBI.

(iii) Foreign Sector Banks: Some of the foreign banks have branches In India and headquarters abroad. These types of banks are included in this sector. These banks follow the rules and regulations of their country’s central bank as well as RBI. The number of foreign banks in India is more than 40.

(iv) Regional Rural Banks (RRB): These banks work for the agriculture and rural sectors. These Banks were established in 1975 and registered under Regional Rural Bank Act, 1976. The stakes of these banks are owned by the Central bank (50%), State Government (15%), and Commercial Bank (35%).

(c) Co-operative Banks: All those banks which run by an elected managing committee working on no-gain no-loss and are registered under the Co-operative Societies Act 1912, are known as Co-operative banks. These banks finance agricultural activities like farming, hatcheries, etc. in rural areas and small businesses, self-employment, and industries in nonrural areas. These banks are divided into three types.

Those are:

(i) Urban Co-operative Banks: and urban, which finance small businesses. banks located in semi-urban

(ii) State Co-operative Banks: The bank is an association of central co-operative bank and acts as a protector of the collaborative banking system in the state. Its funds are gained from the overdrafts, social capital, loans, etc.

(iii) Primary Agricultural Credit Society (PACS): A Primary Agricultural Credit Society (PACS) is a basic unit and smallest cooperative credit institutions, which works on the grassroots level (gram panchayat and village level).

(d) Local Area Banks (LAB): These banks were introduced in India in 1996 and registered under the Companies Act 1956. These are organized by the private sector and there are only 4 local area banks in India (South India). List of Local Area Banks.

(i) Coastal Local Area Bank Ltd.

(ii) Capital Local Area Bank Ltd.

(iii) Krishna Bhima Samruddhi Local Area Bank Ltd.

(iv) Subhadra Local Area Bank Ltd.

(e) Specialized Banks: These banks are established for a specific purpose only.

These are:

(i) Small Industries Development Bank of India (SIDBI): These banks are set up to provide loan facilities to small-scale industries and businesses. This bank is also responsible for providing modern technology equipment to small-scale industries.

(ii) EXIM Bank (Export And Import Bank)- EXIM bank is responsible for providing loans or any financial assistance with the export or import of the goods.

(iii) National Bank of Agricultural and Rural Development (NBARD) – This bank is responsible for providing financial assistance to the rural, Handicraft, village, and Agricultural development.

(f) Small Finance Banks: These banks provide loans and financial support to the small farmers, Micro industries, and other unorganized sectors of society. RBI Governs these Banks also.

(g) Payments Banks: The payment banks are conceptualized by the RBI but customers of these banks cannot avail loans or credit cards and the deposit limit is Rs. 1 lacs only. Customers can get the facilities like online banking, ATMs, Debit cards, etc.

3. Write note on the history and development of banking in India. Briefly explain the recent developments in Banking.

Ans: In India, indigenous bankers have existed in the society since very ancient period and have been carrying on their age old banking operations in different areas of the country.

In our country, we have two sectors in the field of banking operations they are:

(a) Organized. and

(b) Unorganized sector.

The activities of the organized sector is Satisfactory as compared to the unorganized sector. The Reserve Bank of India tried to regulate and provide facilities to the indigenous bankers. But, despite its best efforts, the reserve Bank has not been able to integrate the indigenous bankers with the modern banking system.

So, still in our country, the unorganized sectors have occupied a prominent role mainly in the rural and semi-urban areas. Beside this some loan offices, nidhis and money lenders are found to be very popular in some parts of the country.

The history of development in Indian Banking System can be studied as follows:

(a) Pre-Independence period. and

(b) Post-Independence period.

Pre-Independence history of Indian commercial banking is marked by slower growth and during this period, banking institutions primarily consisted of indigenous banks, money lenders, nidhis, loan offices etc., as mentioned above.

Commercial banking in India mainly began with the establishment of the first joint stock bank known as the Bank of Hindustan. But, this bank was unable to perform its functions due to mismanagement and ultimately, the bank failed in 1832.

In, 1806, the Bank of Bengal was established. Which was the real beginning of the modern commercial banking in the country. Gradually the Bank of Bombay and Bank of Madras were established in 1840 and 1843 respectively. All these banks were established under the charter of East India company, known as the Presidency Bank.

In the last part of the 18th century, many English agency houses established the commercial banks on modern pattern.

Again, in the year 1850, the passing of the joint stock companies Act encouraged the companies to establish money commercial banks. In 1863, 25 banks were established in the metropolitan city Bombay, but due to the inefficient management, the banks could not survival.

In 1865 the Allahabad Bank, and in 1874 the Alliance Bank of Simla were established, but in 1923 the bank of Simla also could not survive.

Again in the year 1881 oudh commercial Bank was established as a Pure Indian bank and it was followed by the setting up both Punjab National Bank and Peoples Bank in 1894 and 1901 respectively.

The great Swadeshi Movement in the year 1905 gave great stimulus to. the starting of Indian Banks and many banks were established such as the Bank of India Ltd. in 1960. The Bank of Baroda Ltd. and the central Bank of India Ltd. in the year 1908 and 1911 respectively. Then came the period of banking crises during the period from 1913-17. and as a result several banks failed. Though the Banking Industry faced a series of crisis and consequent bank failures, the Situation changed after independence of the country.

Prior to independence in the year 1921, the Imperial Bank was established in the country by amalgamating. The Presidency bank of Bengal, Bombay and Madras. The Imperial Bank was nationalized by passing of the state Bank of India Act, 1955 which was brought into force with effect from the 1st July 1955.

Again, there was a strong recommendation in the year 1926 from the Hilton young commission for the establishment of a separate central Bank in the country. Ultimately, the introduction of the bill in the Legislative Assembly in the year 1933 resulted in establishment of Reserve Bank of India in April, 1935.

The development of banking system after independence was more impressive. The first step of nationalization of the Reserve Bank changed in the outlook of the bank as the Central Bank of the country. Again for smooth, efficient and balanced growth of the banking business in the country, the Banking Regulation Act. 1949 was passed.

In the year 1967, the government initiated the scheme of social control over banks for proper allocation of institutional credit over unbanked and under banked areas, and to ensure that the neglected sectors and the small borrowers, who depended on non-institutional finance, also get credit from banks on reasonable terms.

Though social control gave certain directions and guidelines to commercial banks. The multifarious needs of the community became very slow, so, the Government nationalized 14 major commercial banks on July 19, 1969 and after 11 years of 1st phase of bank nationalization, government nationalized 6 more banks on 31st March 1980.

Nationalized banks were expected to give priority to the scheme of the neglected sectors and exports to meet some of the demands of the Public Sector undertaking, and to use the balance of the available sources for organized industries on the basis that new enterprises and those in backward areas will be preferred to the big business houses.

Again in order to expand branch network in all parts of the country, the Lead Bank scheme was introduced. Under this scheme, the lead bank was required to concentrate on the banking business and resources development in the districts assigned to it in collaboration with other development agencies.

Recent developments in Banking (Technological development) are:

(i) Core Banking: Core banking is one of the technological developments in banking system. Core banking is type of banking in which a person, who opens a bank a/c in a branch of a bank, will become a customer not only of that branch, but he becomes a customer of all branches of that bank and can conduct banking transactions anywhere and at anytime. Thus he can deposit and withdraw cash from any where with the branches of same bank.

(ii) Electronic Fund Transfer (EFT): EFT is a scheme introduce by RBI as per the recommendations of SHARE Committee. EFT is a system by which money can be transfer from one a/c to another a/c at any time from any where electronically. The use of pay-in-slips, cheques and drafts are converted into electronic form and there by amount can easily be either debited or credited to the customer a/c within no time.

(iii) Tele Banking: Tele banking is one of the popular technological developments in banking systems. Tele-banking refers to telephone banking under which a number of banking services or facilities offered by bank to the customers by using telephone.

(iv) Anywhere Banking: It is one of the banking facilities extended under core banking system. Under this facility, a bank customer can operate his a/c from any branches of the bank at any place and at any time. It is considered as 24×7 services. In this system customer can operate his a/c from any branches of the bank in one city (intercity) between different cities (intra-city). It includes Tele-banking, Mobile banking, ATM, etc.)

(v) Mobile Banking: Mobile banking is a latest development in banking service. Mobile banking is a type of banking facility under which a customer can conduct banking transactions with his bank by using his mobile phone. Mobile banking works through SMS (Short Messaging Service) technology. Mobile banking works through a set of text messages appears on the mobile phone screen.

4. Explain the Functions of Bank in details. Explain in brief the structure of Indian Commercial Banking System.

Ans: The bank is the organization that accepts deposits from the public which can be withdrawn when needed. This enables people to manage their finances in their bank accounts. Banks give two assurances to the public-Safe deposit and on-demand withdrawal. The additional interest on the deposited amount gives extra benefits to the account holders. Along with the saving facility, Banks also grant loans to the public.

A. Primary Functions of Banks are:

(i) Accepting Deposits: Accepting deposits from the public is the basic function of banks in India. This helps people to develop a habit of saving money. There are different kinds of money depositing accounts for different purposes.

(a) Saving Accounts: This is the best deposit for salary earners as it has no limit on the number of withdrawals. The account holder also gets a small amount of interest on the deposit. This can be opened in the name of a single account holder or a joint account. Banks provide ATM cum debit card, cheque book, and internet banking services to the saving account holders. There is a minimum limit that the account holder has to maintain in the deposit.

(b) Fixed Deposit: Fixed Deposit or Term Deposit enables people to deposit money for a fixed tenure and no can be withdrawn during this period. In case, if a depositor withdraws money before the completion of tenure, the bank puts a penalty. If depositors complete the tenure, banks will provide them the promised amount. The rate of interest is very high in this kind of deposit and varies according to the period.

(c) Current Deposit: These bank accounts are the best for Business purposes. The account holders get the overdraft facility and these deposits work like short-term loans for fulfilling urgent needs. The high-interest rates are charged by the banks along with overdraft charges in order to maintain the reserve for unknown demands for overdraft.

Recurring Deposit – The account holders are required to deposit a fixed amount of money at regular intervals and money can be withdrawn after the completion of tenure. The rate of interest is very high in this deposit as the account holders get the compound interest. A big amount of money is provided at the end. Small merchants and salaried persons use this.

(ii) Granting Loans: Bank uses the public’s money for lending loans to the businessmen or people to meet their emergencies. The bank charges a very high rate of interest on loans. The banks get profit from the difference between the rate of interest for deposits and the rate of interest on loans.

Following types of loans are granted by the Banks:

(a) Bank Overdraft: These loans are provided to the businessmen. They can withdrawal more money than the amount in their accounts and have to deposit it back before a certain limit. The rate of interest is charged on the amount borrowed.

(b) Cash Credits: Banks grant these loans to all types of account holders and even to those also who don’t have an account with the bank. These loans are granted against a mortgage of any property in the name of the borrower. Cash credits are short-term loans with a very high rate of interest is charged on the money withdrawn.

(c) Loans: Banks lend these loans for a longer period like 1 to 5 years or more against any tangible asset. The borrower has to pay installments on a regular basis as decided by the bank during lending the loan. The rate of interest is charged on the total amount whether withdrawn or not.

(d) Discounting the bills of Exchange: In these short-term loans, sellers discount the bill from the bank for certain fees. Banks advance money by discounting the bills of exchange. The bill is directly paid to the seller on behalf of the buyer and discount charges are deducted. At the end of the fixed tenure, the bank presents the bill to the seller or buyer to collect the amount.

B. Secondary Functions of Banks are:

(i) Agency Functions of Banks: Banks also work as agents for their customers. Let’s have at the Agency functions of banks are:

(a) Transfer of Funds- Banks help their customers to transfer money from one bank to another.

(b) Periodic Payments- Banks also pay the electricity bills, water bills, etc. on behalf of the customer. These are called periodic payments.

(c) Periodic Collections- Banks collect periodic payments on behalf of the customer. These include salaries, Pensions, etc.

(d) Cheque collections- The banks collect the cheque’s money through the clearing section of the customers same as collecting money from the bill of exchange.

(e) Portfolio Management- The banks manage the activities of their customers regarding sales and purchase of shares and debentures, etc. Other Agency functions- The banks are the executors, trustees, advisors, etc. for their customers.

(ii) Utility Functions of Banks:

(a) Issuing letters of credits, traveler’s cheques, etc.

(b) Locker facilities for important documents, valuable assets, etc.

(c) Foreign exchange dealing.

(d) Shares and debentures underwriting.

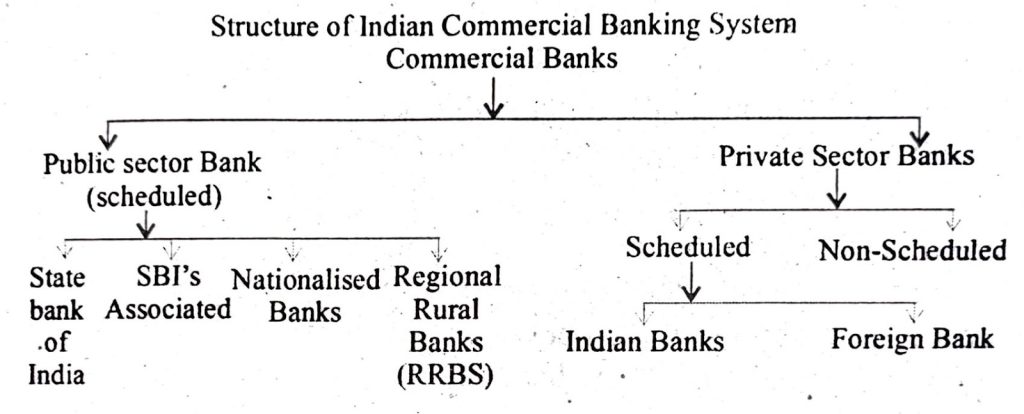

Commercial banking in India mainly divided into two groups:

(i) Public sector banks (all of them are scheduled banks). and

(ii) Private sector banks.

The public sector banks in India have developed in four phases:

(i) Firstly the state banks in India (nationalizing the Imperial Banks of India).

(ii) Secondly, The subsidiaries of the State Bank of India.

(iii) Thirdly on July 19,1969, 14 major commercial banks were nationalized. Again, on April 15, 1980,6 more commercial banks were nationalized.

(iv) Fourthly, establishment of Regional Rural Bank (R.R.B) in 1975.

The private sector banks in India can be classified into two groups. They are:

(i) Indian Banks. and

(ii) Foreign Banks.

Indian Banks are the banks other than nationalized banks owned and controlled by the Indian entrepreneurs.

Foreign banks are the banks which are incorporated outside India but having a place of business in India.

5. Describe in brief the Evolution of Banking Institutions. Explain the Stages in the Evolution of Banking in India.

Ans: The evolution of banking institutions can be Traceable in the early period of human history when the metallic coins were used as a medium of goods and services in the society.

As early as 2,000 B.C. The Babylonians had developed a system of banks. In the ancient Greece and Rome, the practice of storing precious coins and metals at sale custody and loaning out money to the public on high interest was prevalent. At that time, people deposited their surplus funds in the Greek temples and these temples become the money lending institutions.

In the very early stages of banking business, it largely meant for money lending which was restricted to some selected numbers of families basically who looked after their business as a sole proprietorship. Bank of Venice was founded to be the first public enterprise in Italy in 1157. The Bank of Bareilona in Spain was established in 1401 followed by Bank of Geneva in 1407. Again in 1609 the Bank of Amesterden was established.

According to Goefrey crowther. The present day banking has three ancestors. They are-the percent, the Gold-Smith and the Money Lender. Because of the higher reputation or credit, the mercent could able to collect money from his customers and issue documents that were accepted as title of money. The goldsmith performed business activities mainly in England. Because of the danger of theft, people kept there precious coins in the safe custody of goldsmith notes. Money-lender performed his business activities with his own money. Finally, he started accepting money from his clients and found it profitable to borrow at a minimum rates of interest and again lend it at maximum rates of interest.

In India during the Vedic period money lending activities were found in Hindu scriptures. During the Period of Ramayana and Mahabharata, the banking had become a full-fledged activities.

In medieval Europe, Lombardie’s performed banking activities for a long time. But, because of the wars in that period many famous Lambardian families migrated to some other countries like England, France, Belgium etc. Lambardians could not mix-up with the people of England. So, the king Henry Forth give them a separate area for their Settlement. Lambardian constructed a street in that particular area and performed their business activities, which is known as the famous Lambard street.

In Barcilona the public sector bank was established in 1401, Bank of Grana was established in 1407. Again in 1556 the Bank of Sweden was established. These banks performed. The general banking business in that time.

India is a country depending on agriculture. So for financing agriculture and allied activities in the rural areas central co-operative and state cooperative banks have been established to fulfill the various needs of the agriculturists and village people in different areas of the country. The cooperative banks and commercial banks are unable to Provide long-term loans. So, to fulfill the needs to the agriculturists Land Development Banks (LDB’s) has been established in the country both in the National and state level. Another apex institution in the field of agriculture and rural development was set up in the year 1982 known as National Bank for Agriculture and Rural Developments (NABARD).

Another scheduled bank known as the Regional Rural Bank came into existence on 2nd October 1975 when 5 regional rural banks were established under an ordinance entitled Regional Rural Banks ordinance, 1975. The ordinance was later replaced by the Regional Rural Banks Act, 1976. The bank was established with a view to provide necessary help to the agriculture, trade, commerce, industry and other productive activities in the rural areas credit and other facilities, Particularly to the small and marginal farmers, agricultured labourers, artisans and small entrepreneurs, etc.

After independence, The Banking Regulation, 1949 was enacted, to play a vital role for sound and balance growth of banking business in the country.

Some important stages in the evolution of modern banking in India are as follows:

(i) Agency Houses: When the English traders came to India, they had problem of raising working capital due to the language barrier. Therefore, they established Agency Houses which combined trading with banking. One agency house established the first bank in India called the Bank of Hindustan in 1770. Later on, many banks were established. But they disappeared as fast as they were born. Anybody could then start a bank. The field was free for all.

(ii) Presidency Banks: The East India Co., the ruler of India, took initiative in establishing Presidency Banks by contributing 20% of their share capital to meet its own demand for funds. Accordingly, Bank of Bengal, Bank of Bombay and Bank of Madras were established in 1806, 1840 and 1943 respectively.

(iii) Joint Stock Banks: In 1884, banks were allowed to be established on the principle of limited liability. In due course, this encouraged establishment of banks. By the turn of the century, many banks with the initiative of Indians were established. Punjab National Bank, Allahabad Bank, Bank of Baroda are some of the banks then established. Many foreigners also came in the field of Indian banking.

(iv) Imperial Bank of India: To meet the competition of foreign banks, the three Presidency Banks were amalgamated and a powerful Imperial Bank of India was established in 1921 with its network of branches all over the country. This bank was later nationalised in 1955 and it is today’s State Bank of India. This is a prestigious bank as the Government is its customer.

(v) Establishment of the Reserve Bank of India: Though there was boom in banking, due to absence of any regulation and facility of timely assistance there were recurrent bank failures. This resulted in suspicion about banks in the minds of the people. They stayed away from banks. The need for a separate Central Bank was emphasised by the Hilton Young Commission. Accordingly, the RBI was established in 1935 to perform all the functions of a Central Bank. It was modeled on the pattern of the Bank of England. But it did not have much power of regulation. The period was also critical one due to the great depression and the subsequent Second World War. The RBI could not do much about banking.

(vi) Nationalisation of the RBI and the Banking Regulation Act: These two important steps were taken in 1949. Immediately after independence wide powers of regulation and control were given to the RBI and by making use of those powers the RBI was successful in making Indian banking trustworthy. Soon, bank failures became a thing of the past and India’s banks progressed under the guidance of the RBI. Many malpractices, deficiencies and drawbacks were sought to be removed by the RBI.

(vii) Nationalisation of Banks in 1969 and 1980: Another significant step was taken in 1969 by nationalising 14 big Indian banks. Then six more banks were nationalised in 1980. The nationalisation of banks brought about a sea-change in the policies, attitudes, procedures, functions and age of banks. Indian banks are now being prepared to become international players. These are the stages through which Indian banking developed.

(viii) Discuss the classification of banks in India: The banking institutions form an indispensable part in a modern developing society. They perform varied functions to meet the demands of various sections of the society. On the basis of the functions performed and its ownership, the banks can be classified into the following types:

(a) On the Basis of Functions:

1. Commercial Bank: Banks, which help for the development of trade and commerce, are called Commercial Banks. The commercial banks may be owned by government or owned by private sector. For e.g.: Canara Bank, Punjab National Bank, Lakshmi Vilas Bank, Karur Visya Bank etc., are called as commercial banks.

2. Industrial Bank: These banks assist to promote industrial development by providing medium and long term loans, underwrites the shares and debentures, assisting in the preparation of project reports, providing technical advice and managerial service to the industries. For · e.g.: Industrial Development Bank of India (IDBI), Industrial Credit and Investment Corporation of India (ICICI), are known as industrial banks.

3. Regional Rural Bank: These banks are established in rural areas. Its object is to develop the rural economy by providing credit and other facilities for agriculture, trade, commerce, industry and other productive activities in the rural areas.

4. Exchange bank: Exchange banks deal in foreign exchange and specialize in foreign trade. It plays an important role in promoting international trade. It encourages flow of foreign investments into India. and helps in capturing international capital markets.

5. Central bank: Every country has a central bank of its own which is called as central bank. It is the apex bank and the statutory institution in the money market of a country. The central bank occupies a central position in the monetary and banking system of the country and is the superior financial authority. In India, the Reserve Bank of India is the central bank of our country.

(b) On the Basis of Ownership: On the basis of ownership banks can be classified as:

1. Public Sector Banks: These types of banks are owned and controlled by the government. The nationalized banks and regional rural banks come under this category.

2. Private sector Banks: These Banks are owned by private individuals and corporations.

3. Cooperative Banks: These banks are operated on cooperative principles. It is a voluntary association of members for self-help and caters to their financial needs on a mutual basis. These banks are also subject to control and inspection by Reserve Bank of India. The main function of co-operative banking is to link the farmers with the money markets of the country.

(c) On the Basis of Schedules of RBI:

1. Scheduled banks: These types of banks are included in the second schedule of the Reserve bank of India Act 1934. The banks, which fulfill the following conditions, are classified into scheduled banks.

(i) Its paid up capital and reserves are at least Rs. 5 Lakhs.

(ii) Its operations are not detrimental to the interest of the depositors.

(iii) It is a corporation or co-operative society and not a partnership or a single owner firm.

2. Non-Scheduled banks: The banks, which are not covered by the second schedule of Reserve Bank of India, are called as non-scheduled banks.

6. Make classifications of Indian Banking institutions.

Ans: Banking institution can be classified in the following ways:

I. Apex Banking Institutions:

(i) Industrial Development Bank of India.

(ii) National Bank for Agriculture Rural Development.

(iii) Export Import Bank of India.

(iv) Industrial Reconstruction Bank of India.

(v) National Housing Bank.

II. Banking Institutions:

(a) Commercial Banks.

(i) Public sector Banks.

(a) State Bank Group.

(b) Nationalised Banks.

(ii) Private Sector Banks.

(a) Indian Banks.

(b) Foreign Banks.

III. Regional Rural Banks.

IV. Co-operative Banks.

V. Development Banks.

(i) Industrial Development Banks

A. National Level Development Banks:

(a) Industrial Finance Corporation of India.

(b) Industrial credit and investment corporation of India.

(c) Small Industries Development Bank of India.

B. State Level Development Banks:

(a) State Financial Corporations.

(b) State Industrial Development Corporation.

(c) North Eastern Development Finance Corporation LTD.

(i) Land Development Banks.

(a) Primary Land Development Bank.

(b) State Level Land Development Bank.

(ii) Investment Institutions.

(a) Life Insurance Corporation of India.

(b) Unit Trust of India.

(c) General Insurance Corporation of India.

VI. Credit Guarantee corporations.

(a) Export Credit Guarantee corporation of India.

(b) Deposit Insurance and Credit Guarantee corporation of India.

VII. Money Market Institutions.

(a) Discount and Finance House of India LTD.

(b) Stock Holding corporation of India LTD.

(c) Securities Trading corporation of India LTD.

VIII. Credit Rating Institutions.

(a) Credit Rating Information services of India LTD.

(b) Investment Information and Credit Rating Agency of India.

(c) Credit Analysis and Research LTD.

7. Write in brief about the supervisory and promotional functions of the Reserve Bank of India. What are the functions of the Reserve Bank of India? Discuss.

Ans: The Reserve Bank of India is entrusted with the following supervisory powers for smooth efficient system of banking in India.

They are mentioned below:

(a) The bank has the power to give licenses to the commercial banks.

(b) The bank also possesses the power for expansion of branches.

(c) The bank has the right and power of amalgamation, reconstruction and liquidation of commercial and co-operative banks.

The Reserve Bank of India has greater role to play for the promotion of the entire banking institutions of the country. The bank not only controls the credit and currency in the economy, but also acts as a Promoter of entire financial institutions and looks after for fulfilling the financial needs of the banking institutions of the country.

The steps taken to fulfill the Promotional functions by the Bank are:

(i) The R.B.I established the Bill Market Scheme in 1952 with a view to extend loans to the commercial banks against their demand Promissory notes.

(ii) The R.B.I has taken greater interest in setting up and for development of many specialised financial institutions like Industrial Finance Corporation of India, Industrial Development Bank of India, State Financial Corporations, Unit Trust of India, National Bank for Agriculture & Rural Development and Deposit insurance and credit Guarantee Corporation of India etc.

(iii) The R.B.I. took keen interest in setting up Regional Rural Banks to Provide banking facilities in the rural areas of the country.

(iv) It also Promoted in 1988, the National Housing Banks to provide refinance to institutions engaged in housing finance.

(v) The Bank has taken interest in establishment of Export Import Bank of India (EXIM) to provide finance to exporters.

(vi) The Bank tries to encourages and promotes research work in banking areas of the country.

Following are the important functions of the Reserve Bank of India:

(a) Monopoly Power of Notes Issue: The Reserve Bank has the monopoly power of note issue. The bank has the sole right to issue currency notes of all denominations except one rupee notes. One rupee notes are issued by the Ministry of Finance of the Government of India. The Bank has a separate ‘Issue Department’ which is fully entrusted with the job of issuing currency notes. The bank follows the ‘Minimum Reserve System’ for issue of bank notes maintains gold and foreign exchange reserves of Rs. 200 crore, of which at least Rs. 115 crore must be in the form of gold.

(b) Banker to Government: The Reserve Bank act as a banker to Government of India. It accepts money for the account of union and State Governments in the Country. So it also acts as an agent to the Government and advices the Government on all financial and banking matters.

(c) Acts as the Banker’s Bank: The Reserve Bank of India acts as the bankers bank. The scheduled banks are required to maintain with the Reserve Bank as cash balance a certain percentage of their time and liabilities. If acts as a lender of the last resort to them. All the scheduled banks can borrow money from the Reserve Bank on the basis of eligible securities.

(d) Custodian of Foreign Exchange Reserves: The Reserve Bank is the custodian of Indias foreign exchange reserves. It maintains the external value of the rupee and for that purpose the Reserves Bank has to holds most of the foreign exchange reserves. As India is the member of IMF, the Reserve Bank has to maintain fixed exchange rates with all other member countries of the IMF, so, the bank. Sells and buys foreign exchange to/from authorized persons at rates fixed by the Government.

(e) Controller of credit: Controller of credit is also one of the important functions performed by the Reserve Bank. The Reserve Bank controls credit to ensure internal price stability and Promote economic growth. Reserve Bank tries to control the inflationary and deflationary pressure in the country. Through this function; and makes extensive use of various quantitative and quantitative techniques to control and regulate credit in the country.

(f) Ordinary Banking Functions: The Reserve Bank also performs variety of ordinary functions related to banking sector like-

(a) accepting deposits from central and State Governments and private individuals without interest.

(b) granting loans and advances to the central and state government, local authorities, scheduled and state co-operative banks repayable within 90 days.

(c) It can open account in the world bank or in some foreign central bank.

(g) Miscellaneous Functions: The Reserve Bank also performs the miscellaneous functions like-

(a) Collecting and Publishing statistical information relating to banking, finance, credit, agricultural and industrial production etc.

(b) Setting up to Bankers Training college for extending training facilities to supervisory staff of commercial bank.

(h) Promotional and Development Functions: The Reserve Bank also performs promotional and development functional-

(a) By encouraging the commercial banks to expand their branches in the rural and semi urban areas.

(b) Helping to promote the process of industrialization in the country by setting up specialized institutions for industrial finance.

8. Discuss the development of banking sector in India after Independence.

Ans: At the time when India got independence, all the major banks of the country were led privately which was a cause of concern as the people belonging to rural areas were still dependent on money lenders for financial assistance.

With an aim to solve this problem, the then Government decided to nationalise the Banks. These banks were nationalised under the Banking Regulation Act, 1949. Whereas, the Reserve Bank of India was nationalised in 1949.

Given below is the list of these 14 Banks nationalised in 1969:

(a) Allahabad Bank.

(b) Bank of India.

(c) Bank of Baroda.

(d) Bank of Maharashtra.

(e) Central Bank of India.

(f) Canara Bank.

(g) Dena Bank.

(h) Indian Overseas Bank.

(i) Indian Bank.

(j) Punjab National Bank.

(k) Syndicate Bank.

(l) Union Bank of India.

(n) United Bank.

(o) UCO Bank.

Impact of Nationalisation

There were various reasons why the Government chose to nationalize the banks.

Given below is the impact of Nationalising Banks in India:

(i) This lead to an increase in funds and thereby increasing the economic condition of the country.

(ii) Increased efficiency.

(iii) Helped in boosting the rural and agricultural sector of the country.

(iv) It opened up a major employment opportunity for the people.

(v) The Government used profit gained by Banks for the betterment of the people.

(vi) The competition decreased, which resulted in increased work efficiency

This post Independence phase was the one that led to major developments in the banking sector of India and also in the evolution of the banking sector.

9. Explain the various methods of credit control adopted by the Reserve Bank of India.

Ans: Control over creation of credit by the commercial banks is one of the important functions of the Reserve Bank. Though the credit is essential for trade and industry, but excessive credit may be harmful for the economy.

So the Reserve Bank adopts various methods of credit control from time to time which are explained below: