Indian Banking System Unit 4 Recent Trends in Indian Banking, College and University Answer Bank for BA, B.com, B.sc, and Post Graduate Notes and Guide Available here, Indian Banking System Unit 4 Recent Trends in Indian Banking to each Unit are provided in the list of UG-CBCS Central University & State University Syllabus so that you can easily browse through different College and University Guide and Notes here. Indian Banking System Unit 4 Recent Trends in Indian Banking can be of great value to excel in the examination.

Indian Banking System Unit 4 Recent Trends in Indian Banking

Indian Banking System Unit 4 Recent Trends in Indian Banking Notes cover all the exercise questions in UGC Syllabus. Indian Banking System Unit 4 Recent Trends in Indian Banking provided here ensures a smooth and easy understanding of all the concepts. Understand the concepts behind every Unit and score well in the board exams.

Recent Trends in Indian Banking

INDIAN BANKING SYSTEM

| VERY SHORT TYPES QUESTION & ANSWERS |

A. Multiple choice questions and answers:

1. ATM password should be kept in-

(a) Personal diary.

(b) Office diary.

(c) Memory.

(d) All of above.

Ans: (c) Memory.

2. ATM password to be shared only with-

(a) Spouse.

(b) Obedient son.

(c) Obedient daughter.

(d) None of above.

Ans: (a) Spouse.

3. ATM means

(a) Any Time Money.

(b) Auto Truck of Mahindra.

(c) Automated Teller Machine.

(d) None of above.

Ans: (c) Automated Teller Machine.

4. Timely repayment of loans results

(a) Good reputation.

(b) No tension.

(c) Easily availability of loan in future.

(d) All of above.

Ans: (d) All of above.

5. Defaulter of loan means

(a) Not paying loan installments.

(b) Bad reputation.

(c) Illegal activities.

(d) None of above.

Ans: (a) Not paying loan installments.

6. Bank provides loans for

(a) Home.

(b) Car.

(c) Education.

(d) All of above.

Ans: (d) All of above.

7. Education Loans

(a) Cover tuition fee & expenses.

(b) Are repayable after completion of course.

(c) Granted for studies in India & abroad.

(d) All of above.

Ans: (d) All of above.

8. Internet banking refers to

(a) Operation of account through internet.

(b) Opening of account through ATM.

(c) Both (a) & (b).

(d) None of above.

Ans: (a) Operation of account through internet.

9. ATM can be used for

(a) Cash withdrawal.

(b) Account enquiry.

(c) Statement of account.

(d) All of above.

Ans: (d) All of above.

10. Contents of locker are

(a) only known to hirer.

(b) known to Bank.

(c) Both (a) & (b).

(d) None of above.

Ans: (c) Both (a) & (b).

11. What is RuPay Debit Card?

(a) Domestic debit card.

(b) Introduced by National Payments Corporation of India.

(c) Accepted at all ATMs & POS machines.

(d) All of above.

Ans: (a) Domestic debit card.

12. Which type of deposits earns higher interest rate?

(a) Current account.

(b) Savings Account.

(c) Fixed Deposits.

(d) None of above.

Ans: (c) Fixed Deposits.

13. Can illiterate person be issued Debit card?

(a) No.

(b) Yes.

(c) Only in case of joint account.

(d) Only in case he is head of family.

Ans: (b) Yes.

B. Fill in the blanks:

1. I ATM customer _____________ choose the denomination of the currency notes (can/cannot).

Ans: cannot.

2. Consortium approach to lending was introduced by the _____________ (commercial banks / RBI).

Ans: RBI.

3. Industrial banks gives _____________ loans (short-term/long term).

Ans: Long term.

4. Land Mortgage Banks extend _____________ loans (long term/short-term.

Ans: Long term.

5. Open market operations comes under the _____________ method (qualitative/quantitative).

Ans: Quantitative.

6. _____________ is the bailment of goods as security for payment of a debt or performance of a promise (lien/pledge).

Ans: Pledge.

7. In case of _____________ possession of goods is not given to the bank (Hypothecation/ pledge).

Ans: Hypothecation.

8. Participatory approach was introduced by _____________ (RBI/development banks).

Ans: RBI.

9. All the ATMs are open _____________ (12 hrs/24 hrs).

Ans: 24 hrs.

10. National Housing Bank has been set up in _____________ (1988/1989).

Ans: 1988.

C. Answer the following questions:

1. When the scheme of certificate of Deposits was started in India?

Ans: 1989.

2. When the Money Market Mutual Fund was set up by commercial banks in India.

Ans: 1991.

3. Where Euro Dollar Market is located.

Ans: Europe.

4. What is the functions of Exchange control department of RBI.

Ans: To conduct the business of sale and purchase of foreign exchange.

5. Who introduced the system of Net Liquidity Ratio?

Ans: The Reserve Bank of India.

6. When the banker’s Books Evidence Act was passed?

Ans: In the year 1891.

7. In which accounts overdraft facilities are allowed.

Ans: Current Account.

8. Can a married woman open a bank account?

Ans: Yes.

9. Letter of credit is useful in which trade?

Ans: Foreign Trade.

10. Cash credit is granted to the borrower against what type of asset.

Ans: Current assets.

D. Write “true” or “False”:

1. There are eight subsidiaries of the State Bank of India.

Ans: False.

2. State Bank of India is the biggest commercial bank, is in a class by itself.

Ans: True.

3. The motive of the development bank is to serve public interest rather than to make profits.

Ans: True.

4. The bank rate policy is a modern weapon of credit control used by a control bank.

Ans: False.

5. Calculate stock exchange is out of the developed stock exchange in the country.

Ans: True.

6. For a well organized money market, there should be a strong central Bank in the country.

Ans: True.

7. National Stock Exchange of India was in corporate in 1992.

Ans: True.

8. Over the counter Exchange of India is a company not incorporated under the companies Act 1956.

Ans: False.

9. Small scale industries include under priority sector.

Ans: True.

| SHORT TYPE QUESTIONS & ANSWERS |

1. Why choose a core banking solution?

Ans: Despite the few limitations mentioned earlier, your bank still needs a core banking platform to optimize operations and maximize ROI. With a vendor like SDK. finance, you’ll get a core banking solution that offers advanced analytics, customer relationship management, and support features. You will also get access to the source code for your back office and in-house teams. And above all, your neobank ecosystem will remain safe from unauthorized access.

2. What are IT core banking services?

Ans: The key core banking services include new accounts creation and customer relationship management, interest calculations, deposits and withdrawals processing, loans issuing and servicing etc.

3. What Is Financing?

Ans: Financing is the process of providing funds for business activities, making purchases, or investing. Financial institutions, such as banks, are in the business of providing capital to businesses, consumers, and investors to help them achieve their goals. The use of financing is vital in any economic system, as it allows companies to purchase products out of their immediate reach.

Put differently, financing is a way to leverage the time value of money (TVM) to put future expected money flows to use for projects started today. Financing also takes advantage of the fact that some individuals in an economy will have a surplus of money that they wish to put to work to generate returns, while others demand money to undertake investment (also with the hope of generating returns), creating a market for money.

4. Point out the functions of financial market.

Ans: The important functions of the financial markets are as follows:

(a) They create and allocate credit.

(b) They serve as intermediaries in the process of mobilization of saving.

(c) They provide convenience and benefits to lenders as well as borrowers.

(d) They enable economic units to exercise their time preference.

(e) They help in the separation, distribution, diversification and reduction of risk.

(f) They provide efficient payment mechanism.

(g) They increase liquidity of financial claims through securities trading.

(h) They provide efficient portfolio management.

5. Point out the functions of Financial Institutions.

Ans: The functions of financial institutions are mentioned below:

(a) They issue claims to their customers that have characteristics different from those of their own assets i.e. banks accept deposits as liability and convert term as assets such as loans.

(b) They choose and manage portfolios whose risk is low and return is high, and such a way can reduce transaction costs.

(c) They provide large amounts of finance on the basis of economies of scale in lending and borrowing.

(d) They distribute risk through diversification and thereby reduce if for savers as in the case of mutual funds.

6. Write a note on take out Financing.

Ans: Take out financing implies a commitment to provide permanent financing following construction of a planned project. The take out commitment is generally predicted upon specific conditions. Such as, a certain percentage of Unit sales or leases for the permanent loan to “takeout” the construction loan. Most construction lenders require takeout financing.

In other words, it is an agreement by a financial institution or another investor to make a long term loan at a certain, stated date in the future.

A take out commitment may be made in construction or other projects when short term financing is initially beneficial but the borrower anticipates long-term financing to become more advantageous at a later time.

It is a binding agreement by a lender to provide permanent financing at the expiration of the construction financing, it certain conditions have been met. These usually include minimum occupancy levels for an income producing property.

Take out finance is more useful from users point of view because users can use it for a much longer period without any difficulty.

It is also advantageous from lenders point of view. Lenders make an agreement with the users for a fixed period of time through which he can get good return in future. So, now a days most lenders are willing to in perform take out financing business.

7. What are the Need For Take-Out Financing Scheme?

Ans: Need For Take-Out Financing Scheme:

(i) Long-term infrastructure involves huge amounts as well as a long gestation period.

(ii) The Indian banking sector cannot go beyond a certain exposure limit, which refers to limits for arrangements for providing funds or credit including loans and advances, debt and equity securities, loan substitute securities, and financial leases.

(iii) The banking sector has limitations of the smaller balance sheets, as compared to the size of the Infrastructure Projects.

(iv) The exposure limit prescribed by the RBI can be crossed in the case of a few large projects.

(v) Financing done by commercial banks usually involves short-term liabilities.

(vi) Various financial institutions such as Insurance Firms and pension Funds provide long term finance, but they are subject to control by the IRDA and other regulators

8. What are the Objectives of Take-Out Financing?

Ans: Objectives of Take-Out Financing Scheme:

(i) It intends to boost the availability of longer-tenure debt finance for infrastructure projects.

(ii) It focuses to reduce sectoral/group/entity exposure issues and asset liability mismatches issues of lenders, who provide debt financing to infrastructure projects.

(iii) To diversify sources of finance for infrastructure projects by encouraging participation of new entities such as medium/small-sized banks, insurance companies, and pension funds.

9. What is Revolving credit?

Ans: Revolving credit is a line of credit where the customer pays a commitment fee and is then allowed to use the funds when they are needed. It is usually used for operating purposes, fluctuating each month depending on the customer’s current cash flow needs.

Revolving lines of credit can be taken out by both corporations and individuals. The bank that is in agreement with the customer of guarantees of maximum amount that can be loaned to the customer. Along with the commitment fee, there are also internet expenses for corporate borrowers and carry forward changes for consumer accounts.

Credit cards are the perfect examples of revolving credit, A bank allows to continuously borrow money up to a certain credit limit, Every time we buy something on credit, that amount is subtracted from our total credit limit and every time we pay off our balance, our credit limit goes back up.

Now, we have to consider interest. If we do not pay full credit card balance at the end of the month, the bank will charge us interest at the amount we still owe anywhere from 10 to 28 percent carrying a balance from month of months is called revolving our debt. If we keep revolving month after month, we could find ourselves in a serious debt mess.

10. Why Revolving Credit is Important?

Ans: (i) Revolving credit involves interest costs, bank charges, and loan processing charges.

(ii) Banks and financial institutions consider present income, credit score, and employment type before giving a revolving line of credit.

(iii) In the case of a corporation, the finances and cash flow statements are checked before granting a line of credit.

(iv) Revolving credit does not actually consider the repayment of the loan. It involves the payment of interest on the credit used.

11. How Does Revolving Credit Work?

Ans: If you’re approved for a revolving credit account, like a credit card, the lender will set a credit limit. The credit limit is the maximum amount you can charge to that account. When you make a purchase, you’ll have less available credit. And every time you make a payment, your available credit goes back up.

Revolving credit accounts are open ended, meaning they don’t have an end date. As long as the account remains open and in good standing, you can continue to use it. Keep in mind that your minimum payment might vary from month to month because it’s often calculated based on how much you owe at that time.

12. What are the Types of Revolving Credit Accounts?

Ans: Credit cards, personal lines of credit and home equity lines of credit are some common examples of revolving credit accounts.

(i) Credit cards: Many people use credit cards to make everyday purchases or pay for unexpected expenses. Some credit cards come with rewards and benefits you can use to your advantage.

(ii) Personal line of credit: A personal line of credit is similar to a credit card. But it’s not linked to a physical card. Instead, you might get the funds in the form of a check or a direct deposit into your bank account.

(iii) Home equity line of credit: According to the CFPB, a home equity line of credit (HELOC) is an open-ended credit account that lets you borrow money against the value of your home. And since it’s open ended, you can borrow and repay the money multiple times as long as you don’t exceed the credit limit. It’s important to note that a HELOC is different from a home equity loan, which is typically a lump sum of money with a fixed interest rate that you borrow once.

13. What are the stages of loan syndication process.

Ans: There are 3 stages of loan syndication process. We will list down each of them below:

Stage 1: The first stage of the loan syndication process is the pre-mandate stage which is initiated by the borrower. The stage involves the borrower either liaison with a single lender or inviting competitor bids from multiple lenders. The borrower has to mandate to the lead bank. After the lead lender has been chosen, they will start the appraisal process. The lead bank will see to the needs of the borrower and will design a loan structure for the borrower and develop a credit proposal.

Stage 2: The next stage involves the lender placing the loan and disbursement. The lead lender initiates selling the loan at the marketplace for which it will prepare an information memorandum, term sheet, and a legal documentation. The lead bank will then approach other banks for participation. Once the loan contract is finalized, the loan amount is disbursed.

Stage 3: The final stage is the post-closure stage which involves monitoring through an escrow account. Escrow account is nothing but the account in which the borrower will deposit the revenue. It’s the agent’s responsibility to ensure that the repayment of loan is the top priority and the payment is done before making payments to any other parties. In the post-closure stage, it’s the job of the agent to manage the operating and running of the loan facility on a regular basis.

14. Briefly write down about Bridge Loan.

Ans: Bridge loan is an important and useful short term loan that is used until a person or company secures permanent financing or removes an existing obligation. This type of financing allows the user to meet current obligations by providing immediate cash flow. The loans are short-term (upto one year) with relatively high rate of interest and are backed by some form of collateral such as real estate or inventory.

As the term implies these loans ‘bridge the gap” between times when financing is needed. They are used by both corporations and individuals and can be customized for many different situations.

So, this loan is also very much helpful to the users so that they may be relief of the temporary financial crisis and for that purpose, the lender generally takes a higher interest rate.

A bridge loan could be used to secure working capital until the round of funding goes through.

In the case of an individual bridge loans are common in the real estate market. As there can often be a time lag between the sale of one property and the purchase of another, a bridge loan allows a home owner more flexibility.

15. What are the Features of Bridge Loan?

Ans: The features of bridge loan are as follows:

(i) Short term loan.

(ii) The loan is backed by collateral security.

(iii) The loan amount depends on the repayment capacity. The cost includes stamp duty charges, registration fees and transfer fee subject to a maximum of Rs.50 lakh or four times the gross annual income, whichever is less.

(iv) The borrower will have to repay the loan by paying equated monthly instalments or paying interest till the entire loan is repaid within 2 years.

(v) The rate of interest depends on the loan amount and the capacity of the borrower to repay and the collateral that is being offered. The rate of interest also depends on the estimated sale price of your home.

16. How a Bridge Loan Works?

Ans: Also known as interim financing, gap financing, or swing loans, bridge loans bridge the gap during times when financing is needed but not yet available. Both corporations and individuals use bridge loans and lenders can customize these loans for many different situations.

Bridge loans can help homeowners purchase a new home while they wait for their current home to sell. Borrowers use the equity in their current home for the down payment on the purchase of a new home. This happens while they wait for their current home to sell. This gives the homeowner some extra time and, therefore, some peace of mind while they wait.

These loans normally come at a higher interest rate than other credit facilities such as a home equity line of credit (HELOC). And people who still haven’t paid off their mortgage end up having to make two payments- one for the bridge loan and for the mortgage until the old home is sold.

17. What is the Bridge Loan interest rate?

Ans: If you have taken a bridge loan in India, then the existing home has to be sold within a year and the loan must be cleared off. The EMI is based on the outstanding amount in the account. The bridge loan rate of interest is extremely high. If you are getting a lower rate of interest on the home loan, then you might as well take the home loan as it accompanies other offers such as refinancing and online account access, etc.

18. What is Consortium finance? Also mention its merits.

Ans: Consortium approach to lending was introduced by the Reserve Bank of India. An experienced banker knows that of the bank investment its resources in one particular type of business enterprise, then it may find itself in a difficult situation, because it this type of enterprise meets with failure due to certain reasons, then it will be very difficult for the banks to recover the sum. So, the banker prefers to finance two or more enterprises rather than a single enterprise, because he knows from his well experience that all the projects will not suffer losses. Not only this, but this approach is also fruitful because of the following reasons.

(a) This approach helps to diversify the risks of lending as the entire lending to a single borrower is going to be financed by several banks.

(b) It breaks the monopoly of big banks to have larger spread risk of accounts.

(c) It enables banks to share experience and expertise.

(d) It introduces uniformity in approaches to lending.

(e) It enables banks to pool their resources. and

(f) Checks multiple financing of the same account.

Because of the above mentioned reasons this approach has gained importance and almost every modern banking institutions are willing to provide finance under this approach.

19. Give an Example of a Consortium Bank.

Ans: In 2018 in Grand Rapids, Michigan, the non-profit, Start Garden, developed a project to provide $1,000 mini-grants as part of their 100 Days/$100,000 initiative to foster entrepreneurship among neighborhood businesses. The project was funded in partnership with a consortium bank, which formed for the purpose of this project. Over several years the aim is for the consortium to invest millions of dollars in the local ecosystem in order to help alleviate poverty. Given the large sum of money involved in the project, various banks pooled their resources to create a consortium bank to provide this investment.

20. Write a note on Preferred finance.

Ans: Now a days preferred finance has become much more popular among different users because of its modern and efficient services. It helps the cash flow position of the users.

So, preferred finance is a modern, professional finance broking firm based in and working for, the Adelaide Hills and Peninsula communities.

Preferred finance not only arrange finance to suit our cash flow but also helps to know exactly the tax position of the users, and fulfill the dreams, all with a minimum of fuss.

The first round of financing undergone for a new business venture after seed capital. Generally, this is the first time that company ownership is offered to external investors. Services a financing may be provided in the form of preferred stock and may offer anti-dilution provisions in the event that further financing through preferred or common stock occurs in the future.

As an enterprise grows and requires additional capital, the subsequent round of preferred stock issued to investors are called series B, series, C, and so on. This allows investors in those subsequent rounds of financing to know where they stand in the hierarchy of claims to future profits.

21. What is a Service Guarantee?

Ans: A service guarantee is a marketing tool service firms have increasingly been using to reduce consumer risk perceptions, signal quality, differentiate a service offering, and to institutionalize and professionalize their internal management of customer complaint and service recovery. By delivering service guarantees, companies entitle customers with one or more forms of compensation, namely easy-to-claim replacement, refund or credit, under the circumstances of service delivery failure. Conditions are often put on these compensations; however, some companies provide them unconditionally.

22. Explain in details about Factoring.

Ans: Factoring is the sole of commercial accounts receivable invoices. To a buyer, or factor, at a discount, in order to obtain cash on the invoices, with the factor assuming full responsibility for credit analyses, payment collection and credit losses on the new accounts. There are usually three parties involved when a invoice is factored such as.

(a) The seller of the product or service who originates the invoice.

(b) The debtor, is the recipient of the invoice for services rendered who promises to pay the balance within the agreed payment terms. and

(c) The factor.

The accounts receivable and the responsibility for the collection are sold, rather than provided as loan collateral and the client must notify all of its customers of the new arrangement. This can involve very substantial payment being made right at the start, with most factors paying 70% to 90% through initial advance of the invoice amount followed by a small additional payment, through reserve release, once they collect the invoice over the course of time, factors may offer the liable individual or entity a discount from 2% to 5% or more on the outstanding debt.

Factoring allows a buyer to purchase the accounts for around 25% less than what they are actually worth. Setting up a factoring deal can be done more quickly than most other forms of finance. The staff at factoring companies are more commercial than at other lending institutions and will work to find a solution for potential client companies.

There are some possible disadvantages, the main one being cost and the fact that clients have to deal with the factoring companies.

Factoring can also be a gamble for the factor, because there may be bad debits or other obstacles to collecting the funds.

23. Write in details about Guarantee services.

Ans: A guarantee services is a promise that a service or product will meet certain consumer expectations or standard. Many times it is provided to the consumer in writing. If the product fails to perform as promised, the vendor may other replacement of the item, refund the purchase price, or offer other forms of reimbursement, a store credit. The purchase of it is to instill consumer confidence.

The type of promise that a merchant makes may differ, depending on the product or service. It is not uncommon for a service guarantee to be predicted on the consumer meeting specific terms and conditions. This places some of the responsibility on the consumer.

Stipulation to a service guarantee may prohibit tampering with a product or require that certain maintenance schedules are followed.

It may also outline what the consumer is required to do in order to prevent the malfunction of a product. If the specified conditions are not met, the guarantee service may be voided.

Conditional agreements often apply to automobile warranties. For example, a guarantee service for an engine may require scheduled maintenance at regular intervals, such as changing the oil change every three months. If the engine were to malfunction as a result of the oil not being changed, on schedule, the service guarantee could be canceled. It is important for a customer to follow the provisions provided.

24. Explain clearly the Repayment Method and its principles.

Ans: Repayment method is the method of repayment of loan by the users under different principles.

Money borrowed for long-term capital investments usually is repaid in a series of annual, semi-annual or monthly payments. There are several ways to calculate the amount of these payments such as-

(i) Equal total payments per time periods (amortization).

(ii) Equal Principal payments per time period. or

(iii) Equal Payments over a specified time period with a balloon payment due at the end to repay the balance.

When the equal total payment method is used, each payment includes the accrued interest on the unpaid balance, Plus an equal amount of the principal. The total payments decline over time. As the remaining principal balance declines, the amount of interest accrued also declines.

In case of long term repayment method, there are some quick facts which are as follows:

(a) Long term loan repayment loans can be repaid in a series of annual, semi-annual or monthly payments.

(b) Payments can be equal total payments, equal principal payments or equal payments with a balloon payment.

(c) The Farmers Home Administration usually requires equal payments for intermediate and long term loans.

(d) Use an amortization table to determine the annual payment when the amount of money borrowed, the interest rate and the length of the loan are known.

Repayment Principles: To calculate the principal amount all terms o the loan must be known i.e. interest rate, timing of payments (e.g. monthly, quarterly, annually) length of loan and amount of loan. Borrowers should understand how loans are amortized, how to calculate payments and remaining balances as of a particular date, and how to calculate the principal and interest portion of the next payment.

Lenders use different methods to calculate loan repayment schedule depending on their needs, borrowed needs, the institutions interest rate policy (fixed or variable), the length of the loan, and the purpose of the borrowed money. Typically home mortgage loans, automobile and truck loans and consumer instruments loans are amortized using the equal total payment method.

25. What are the Features of Internet Banking?

Ans Features of Internet Banking are:

(i) Review the online statement.

(ii) Open a time deposit account.

(iii) Pay utility bills, such as water bills and utility bills.

(iv) Make payments for merchants.

(v) Transfer money.

(vi) Checkbook request.

(vii) Buy general insurance.

(viii) Recharge prepaid / DTH cell phone.

| LONG TYPE QUESTIONS & ANSWER |

1. Explain clearly about Syndicated loan. What are the advantages of Loan Syndication? 20. Who are Participants in a Syndicated Loan?

Ans: A loan offered by a group of lenders (called a syndicate) who work together to provide funds for a single borrower. The borrower could be a corporation, a large project, or a sovereignty (such as a government). The loan may involve fixed amount, a credit line or a combination of the two. Interest rates can be fixed for the term of the loan or floating based on a benchmark rate such as the London Interbank offered Rate (LIBOR) Typically, there is a lead bank or underwriter of the loan Known as the “arranger”, agent, or “lead lender”, This lender may be putting up a proportionally, bigger share of the loan, or perform duties like dispersing cash flows amongst the other syndicate members and administrative tasks.

The main goal of syndicated lending is to spread the risk of a borrowed default across multiple lenders (such as banks) or institutional investors like pensions funds and ledge funds. Because syndicated loans tend to be much larger than standard bank loans, the risk of even one borrower defaulting could. cripple a single lender.

Syndicated loans are also used in the leveraged buyout community to fund large corporate takeovers with primarily debt funding. Syndicated loans can be made on a ‘best efforts” basis, which means that if enough investors can’t be found, the amount the borrower receives will be lower than originally anticipated fund standard revolvers or lines of credit) and institutional investors (Who fund fixed rate term loans).

The advantages of Loan Syndication:

(i) Best prices are available for business.

(ii) You have the option of reducing your term loans.

(iii) The syndicate banks will also share feedback on issues related to your business.

(iv) Loan syndication allows the lenders to have a greater visibility of the borrowers in the open market.

(v) Borrowers have the option of choosing among multi currency options, prepayment rights, and risk management techniques.

Those who participate in loan syndication may vary from one deal to another, but the typical participants include the following:

(i) Arranging bank: The arranging bank is also known as the lead manager and is mandated by the borrower to organize the funding based on specific agreed terms of the loan. The bank must acquire other lending parties who are willing to participate in the lending syndicate and share the lending risks involved. The financial terms negotiated between the arranging bank and the borrower are contained in the term sheet.

The term sheet details the amount of the loan, repayment schedule, interest rate, duration of the loan and any other fees related to the loan. The arranging bank holds a large proportion of the loan and will be responsible for distributing cash flows among the other participating lenders.

(ii) Agent: The agent in a syndicated loan serves as a link between the borrower and the lenders and owes a contractual obligation to both the borrower and the lenders. The role of the agent to the lenders is to provide them with information that allows them to exercise their rights under the syndicated loan agreement. However, the agent has no fiduciary duty and is not required to advise the borrower or the lenders. The agent’s duty is mainly administrative.

(iii) Trustee: The trustee is responsible for holding the security of the assets of the borrower on behalf of the lenders. Syndicated loan structures avoid granting the security to the individual lenders separately since the practice would be costly to the syndicate. In the event of default, the trustee is responsible for enforcing the security under instructions by the lenders. Therefore, the trustee only has a fiduciary duty to the lenders in the syndicate.

2. Write a detailed note on the new trends in commercial banking.

Ans: Drastic changes have been experienced in both theory and practice of Indian commercial banking specially in the post-war period.

Major changes are as follows:

(a) New Development in Banking Theory: Traditional commercial loan theory has now been completely discarded and has given place to the modern suitability and anticipated income theories. All the theories attempt to resolve the liquidity earning problem of the bank.

According to commercial loan theory, the banks can ensure sufficient liquidity by granting only short term self liquidating loans secured by goods. in the process of production or goods in transit. The suitability theory requires the banks to solve their liquidity problem by purchasing highly liquid assets which can be easily shifted to other banks in times of need for liquidity. According to the recent anticipated income theory the banks can solve their liquidity problem even by advancing long term loans if the borrowers repay the loans in series of continuous income theory has enabled the commercial banks to adopt medium-term and long term lending business along with providing sufficient liquidity.

(b) Term lending: In the post-war period, the liquidity of banks increased enormously. In order to improve their earnings, many banks decided to extend the term of their loans. The term loans which were virtually non-existent until 1930 s now constitute more than one third of all commercial bank loans in the USA and UK term loan not only increase earnings of the banks, but also improve their liquidity because such loans are almost always repaid on an installment basis.

(c) Hire Purchase Finance: Hire Purchase Finance which refers to the credit facilities for the Purchase of durable goods on instrument basis, is another post war development in Indian Commercial Banking. HirePurchase facilities help the small entrepreneurs to start new business and the exiting small producers to purchase new tools and equipment.

(d) Personal Loans: Commercial banks started granting personal loans for meeting expenditures to purchase motor cars, household appliances, professional equipment, house repairs and decorations etc.

Now a days banks have introduced several innovative means to enhance their base and make their service accessible. Some of the facilities and service provided are-

Credit card: This is a popular means for providing retail card. A credit card is an instrument issued by a bank is the name of their customer providing for credit. Upto a specific amount.

Another facility and service provided by the banks is the ATM card. Customers can withdraw cash by help of the ATM facility from their respective accounts.

3. What are the Core banking system advantages?

Ans: With a better understanding of the working principle and features of the core banking platforms, let’s explore their key benefits:

(i) Enhanced productivity: Core banking platforms increase operational efficiency by reducing the time it takes to connect with multiple branches. As a result, banks can process transactions faster, regardless of the client’s physical location.

(ii) Improved security Core banking systems use advanced encryption modules to protect the infrastructure from hackers and malware. On the client’s side, bio-verification and two-factor authentication also provide additional layers of security to the platform. These features help banks maintain KYC standards and comply with other banking regulations.

(iii) 24/7 access to banking services: In this era of contactless payments, access to round-the-clock bank services is vital. Users can conduct financial operations anywhere and anytime since the core banking platform never goes offline. Clients can also contact customer support for assistance at any time.

(iv) Lower operational costs: Banks can rely on their core platforms to reduce operational costs since these systems require fewer human resources to function. Besides, the Al-powered infrastructure increases the completion rate of operations and reduces the chances of errors in documentation.

(v) Multiple currencies: Users can trade in multiple currencies instantly without needing to change large amounts at a currency exchange.

4. What are the Advantages of Core Banking? What are the disadvantages of Core banking?

Ans: Advantages of Core Banking:

(a) Limited Professional Manpower to be utilized more effectively.

(b) Customer can have anywhere, more convenient and easier banking.

(c) ATM, Interest Banking, Mobile Banking, Payment Gateways etc. are available.

(d) More strong and economical way of management information system.

(e) Reduction in branch manpower.

(f) Additional manpower can be available for marketing, recovery and personalized banking.

(g) Instant information available for decision support.

(h) Quick and accurate implementation of policies.

(i) Improved Recovery Process causing reduction on recovery costs, NPA provisions.

(j) Innovative, redefined or improved processes i.e. Inter Branch Reconciliation causing reduction in manpower at Head Office.

(k) Reduction in software maintenance at branch and Head office.

(I) Centralized printing and backup resulting in reduction in capital and revenue expenditure on printing and backup devices and media at branches.

(m) Electronic Transactions with other Financial Institutions.

(n) Increased speed in working resulting in more business opportunities and reduction in penalties and legal expenses.

Disadvantages of core banking:

(i) Excessive reliance on era

(ii) Any failure in pc structures can cause whole community to head down.

(iii) If records isn’t included nicely and if right care isn’t always taken, hackers can advantage get admission to the data.

(iv) Computer failure is the one of the disadvantages of core banking. If any failure in computer system occur, it can cause entire network go down.

(v) In core banking, if data is not protected, hacker can go access to the sensitive data.

5. What are the recent developments of Indian Banking?

Ans: The following are some of the recent developments which will help for reaching effect in meeting strengthening the Indian banking system.

The Central Government appointed a high level “committee on financial system”. Under the chairmanship of Sri Narasimham to examine all aspect relating to the structure, organizations functions and procedures of the financial system. The following are some of the major recommendations made by the committee regarding banking system.

(a) Increasing profitability of Banks: In order to increase the profitability of the banks, the following recommendations have been made.

(i) SLR to be brought down in a phased manner over a period of five years.

(ii) Interest on SLR and CRR should be increased.

(iii) Priority sectors should be refined and credit target should be strictly followed.

(b) Uniform Accounting policies: These are particularly related to income recognition and making provisions for loan losses. Moreover, sound practice with regard to valuation of investments should be adopted. The following points are important in this regard.

(i) No income should be recognized on non-performing assets.

(ii) Assets should be classified into four categories, viz standard, substandard, doubtful and less assets, for the purpose of provisioning. Specific provisions should be made for loss and doubtful assets and general provision should be made for sub standard assets.

(iii) A three year period should be allowed for achieving income recognition norms and a four-year period to achieve provisioning norms.

(iv) Provisions made by banks should be allowed as deduction for income tax purposes.

(c) Speedy Recovery: In order to speed up the process of recovery of lank’s debts, the committee suggested that special tribunals should be set up. Moreover, the committee recommended for the establishment of an assets Reconstruction fund for taking over the bad and doubtful debts of the banks at a discount.

(d) Reconstructing of the Banking system: The following recommendations are made in this connection:

(i) The system should evolve towards a broad pattern consisting of-

(a) Three or four large banks (including the State Bank of India) international in character.

(b) 8 to 10 national banks with a network of branches throughout the country engaged in universal banking.

(c) Local banks whose operations would be generally confined of specific regions. and

(d) Rural Banks (Including RRBs) whose operations would be confined to the rural areas and whose business would be predominantly financing of agriculture and allied activities.

(ii) The Government should indicate that there would be no further nationalization of banks, to remove the existing disincentive for the more dynamic among the private banks to grow.

(iii) There should be no difference in Treatment between the Public and Private sector banks.

(iv) There should be no bar to new banks in the private sector provided. They conform to the start-up capital and other requirements/norms relating to accounting, provisioning and other aspects of operations.

(v) Branch licensing be abolished and the matter of opening closing branches be left to the commercial judgement of individual banks.

(vi) Policy with regard to allowing foreign banks to open branches / subsidiaries in India should be more liberal subject to such requirements as may be prescribed by the RBI and subject to same requirements as are applicable to domestic banks.

6. What are the remarkable progress made by banks in India.

Ans: Banking in India has made a remarkable progress is its growth and expansion, as well as business with social perspective in the fulfillment of national objectives.

Indian banking has developed, but its perfection is yet to be seen. There still remain many tasks to be fulfilled.

(a) Still there are villages left without banking facilities, so many more rural bank branches need to be opened.

(b) More lending should be made in favour of priority sectors.

(c) Banks should give more technical assistance to the small industrialists.

(d) Operational costs of banks should be reduced to the minimum and profitability and working results must be maximized.

(e) Banking staff should be adequately trained.

(f) Malpractices, frond, corruption and red-tapism must be done away with.

(g) More attention should be paid to the development of exports.

(h) Banks should give more technical assistance to the small scale industrialists.

Banks have formulated various schemes to provide credit to the small borrowers in the priority sectors like agriculture, small scale industry, road and water transport, retail trade, small business etc. considering the necessity of meeting specific credit requirements of the weaker sections, consumption credit has been included in the priority sector. Similarly, small housing loans to scheduled castes/tribes and weaker sections have also been considered as priority sector loans.

So, the commercial banks in India have really formulated these scheme for the greater welfare of the weaker sections of the nation. But, still the banking facilities are found to be available only in the big cities and towns. Commercial banks should take more and more practical steps to provide required banking facilities to the neglected sectors of the country.

7. What are the important features of credit card facility.

Ans: Commercial banks introduced credit card facility in the early 1980’s though at that time people had no idea about its facility but, gradually this facility was become much more popular among the banks as well as the public.

Important features of credit card facility are as follows:

(a) The credit card is a document of card holders credit worthiness on the one hand and minimizes the use of hard cash in the day to day transactions.

(b) It is a convenient medium of exchange which enables its holder to buy goods and services without using money.

(c) Credit card helps its holder to buy when he wants and to pay when he can. The banks can meets the costs of this facility from increased sales which results from the VSC of credit cards.

(d) The card issuing banks pay to the seller as soon as the goods are sold, but changes the price from the buyer after 30 to 45 days.

(e) The bank also bears the risk of default on the part of card holder.

(f) The net gain of the bank is the amount of commission from the seller wins interest factors and administrative and advertisement costs.

(g) In addition, the bank also earns by way of initial, annual, add-on, and re-issue fees from the prospective card holders.

(h) Credit card are mostly used by elite corporate executives business men, middle income groups etc.

(i) Credit cards are normally use to purchase consumer durables and certain services from the establishment, such as shops, departmental stores, hospitals, railways, hotels, etc.

8. What are the different types of financing with its advantages and disadvantages?

Ans: There are mainly two sources of financing:

(i) Equity financing: Equity finance is a classic way of raising capital for businesses by issues or offering shares of the company. This is one of the major differences in equity finance from debt finance. This finance is generally applied for seed funding for start-ups and new businesses. Well-known companies apply this finance to raise additional capital for the expansion of their business.

Equity finance is generally raised by issues or offering equity shares of the business. Basically, each share is an owner’s unit for that specific company. For instance, if the company has offered 10,000 equity shares to public investors. An investor buys 1000 equity shares of that company, means s/he holds 10% of ownership in the company.

Advantages of Equity Financing : Funding your business through investors has several advantages, including the following:

(i) The biggest advantage is that you do not have to pay back the money. If your business enters bankruptcy, your investor or investors are not creditors. They are part-owners in your company, and because of that, their money is lost along with your company.

(ii) You do not have to make monthly payments, so there is often more cash on hand for operating expenses.

(iii) Investors understand that it takes time to build a business. You will get the money you need without the pressure of having to see your product or business thriving within a short amount of time.

Disadvantages of Equity Financing: Similarly, there are a number of disadvantages that come with equity financing, including the following:

(i) How do you feel about having a new partner? When you raise equity financing, it involves giving up ownership of a portion of your company. The riskier the investment, the more of a stake the investor will want. You might have to give up 50% or more of your company, and unless you later construct a deal to buy the investor’s stake, that partner will take 50% of your profits indefinitely.

(ii) You will also have to consult with your investors before making decisions. Your company is no longer solely yours, and if the investor has more than 50% of your company, you have a boss to whom you have to answer.

(iii) Debt financing: Basically, the cash which you acquire to maintain or run your business is known as debt finance. Debt finance does not provide ownership control to the moneylender; the borrower must repay the principal amount along with the agreed upon interest rate. Mostly, the interest rate is determined based on the loan amount, duration, the purpose for borrowing the specific type of finance and inflation rate.

Advantages of Debt Financing: There are several advantages to financing your business through debt:

(i) The lending institution has no control over how you run your company, and it has no ownership.

(ii) Once you pay back the loan, your relationship with the lender ends. That is especially important as your business becomes more valuable.

(iii) The interest you pay on debt financing is tax deductible as a business expense.

(iv) The monthly payment, as well as the breakdown of the payments, is a known expense that can be accurately included in your forecasting models.

Disadvantages of Debt Financing: Debt financing for your business does come with some downsides:

(i) Adding a debt payment to your monthly expenses assumes that you will always have the capital inflow to meet all business expenses, including the debt payment. For small or early-stage companies, that is often far from certain.

(ii) Small business lending can be slowed substantially during recessions. In tougher times for the economy, it’s more difficult to receive debt financing unless you are overwhelmingly qualified.

The other types of finance are discussed below:

(i) Public Finance: Public finance deals with the study of the state’s expenditure and income. It considers only the government’s finances. The scope of public finance includes the fund’s collection and its allocation among different sectors of state activities that are considered as essential functions or duties of the government.

(ii) Public Finance: Public finance deals with the study of the state’s expenditure and income. It considers only the government’s finances. The scope of public finance includes the fund’s collection and its allocation among different sectors of state activities that are considered as essential functions or duties of the government.

(iii) Corporate Finance: Corporate finance includes financial activities pertaining to running a corporation. It is a department or division which oversees the financial functions of a company. The primary concern of corporate finance is the maximization of shareholder value through short term and long-term financial planning and different strategies’ implementation.

(iv) Private Finance: Private finance denotes an alternative method of corporate finance helping a company raise fund to avoid monetary problems with a limited time frame. Basically, this method helps a company which is not listed on a securities exchange or is incapable to obtain finance on such markets. A private financial plan can also be suitable for a nonprofit organization.

9. What is Core banking? How does Core banking work? What are the Features of Core Banking?

Ans: Core banking is a general term used to describe the services provided by a group of networked bank branches. Bank customers may access their funds and other simple transactions from any of the member branch office at real time. There are several advantages of core banking, the core banking is the set of basic software components that manage the services provided by a bank to its customers through its branches (branch network). The bank’s customers can make their transactions (deposits and withdrawals) from any agency on the ATM at their disposal.

In the long term, the problem that banks faces is to maintain their competitive advantage. They mast change their business plans, know the market trends and reposition in itself in a niche. This applies on both central Banks. The private banks, the retail banks and investment banks. The issue of software publishers of core banking is to develop new products and services while reducing total cost of ownership while remaining affordable for consumers.

A core banking system comprises back-end servers that handle standard operations like interest calculation, passbook maintenance, and withdrawal. When a customer withdraws money from a branch or an ATM, the application sends a request to the centralized data center, which then processes the request and authenticates the operation. The data center contains the database, an application server, a web server, and a firewall to protect the system from malware attacks. Banks can host their data center locally or on the cloud.

Features of Core Banking:

(a) Customer relationship management features including a 360 degree customer view.

(b) The ability to originate new products and customers.

(c) Banking analytics including risk analysis, profitability analysis and provisions for capital reserve allocation and collateral management.

(d) Banking finance including general ledger and reporting.

(e) Banking channels such as teller systems, side counter applications, mobile banking and online banking solutions.

(f) Best practice workflow process.

(g) Content management facilities.

(h) Governance and compliance capabilities such as internal controls management and auditing.

(i) Security control and audit capabilities.

(j) Core banking solutions to help maximize growth, increase productivity and mitigate risk.

10. What is Non-Fund Based Credit?

Ans: Non-Fund Based Credit is where the Fund is not transferred directly to the borrower. It is offered to a third-party as agreed upon by the borrower, on behalf of the Borrower. The bank usually acts as a guarantee provider to the seller on the behalf of the buyer. If the payment is not received by the seller within pre-agreed time, The bank pays the amount to the seller. For e.g. Bank Guarantee, Buyer Credit, Letter of Credit, Supplier Credit.

Following are the advantages of Non-Fund Based Credits:

(i) It offers financial security to the seller if the buyer defaults due to any reason.

(ii) It offers Business expansion opportunities to the exporters.

The different types of non-fund based credit are:

1. Letter Of Credit: A letter of credit is an assurance provided by the Bank to the seller on behalf of the buyer that the seller will receive the buyer’s payment at regular intervals. It also states that if the buyer fails to pay the seller for any reason, the Bank will be responsible for the remaining or full payment.

Letter of Credit is offered based on the collateral of cash or certain securities. With the rising international trading, Letter of Credit is becoming a crucial tool to manage the payments between parties that hardly know each other and live in different countries with different laws. The bank charges a certain percentage from the buyer as the fees for offering the Letter of Security.

The Letter of Credit can be divided into the following parts:

(A) Sight Credit: This letter of Credit is quicker than others. Here the Borrower can take the lender’s funds by showing a bill of exchange and sight letter of Credit.

(B) Revocable & Irrevocable Credit: Revocable Letter of Credits is the one that can be revoked or canceled by the issuing bank without prior notice to any party. Irrevocable Letter of Credit cannot be revoked or canceled by the issuing Bank. So once the LOC is generated, Bank will have to honor the letter.

(C) Confirmed Credit: In this type of Credit, a bank other than the issuing Bank confirms the Letter of Credit by adding its confirmation. Only Irrevocable Letter of Credit is eligible for confirmation.

(D) Back-to-Back Credit: Under this type of Credit, the exporter requests the Bank to offer an LC to his/her local supplier. The request is based on the export LC received by the exporter from an overseas buyer. Here, an LC is issued based on an export LC and hence the name, Back to-Back Credit.

The advantages of a letter of credit to the buyer is as follows:

(i) Allows the buyer to trade with the parties from any corner of the world.

(ii) The buyer can edit the terms and conditions that fit him/her after consulting the seller.

(iii) It acts as a credit certificate for the buyer, and he/she can perform multiple trades as a major financial institution like Bank backs him/her.

(iv) Letter of Credit offers better Cash flow to the buyer.

The advantages of a Letter Of Credit To seller is as follows:

(i) The seller receives the money on fulfilling the terms mentioned In the Letter of Credit.

(ii) There is no risk of losing money for the seller if the buyer fails to pay the money. Seller gets his/her dues from the Bank that has issued the Letter of Credit.

(iii) The letter of Credit is easy to quick to avail based on good credit. If there is a dispute in trading, the seller can withdraw funds from the Bank even when the case is pending.

2. Bank Guarantee: Under this type of Credit, Bank offers assurance that under any circumstances, the Guarantee issuing Bank will fulfill any financial losses incurred by the protected party as mentioned in the Contract.

Let’s take a look at different guarantees:

(A) Financial Guarantee: In this type of Guarantee, the Guarantor takes responsibility for the Borrower. This means, if the Borrower fails to repay the debt, Guarantor will be liable to pay the unpaid amount.

(B) Performance Guarantee: The Guarantor issued a security bond that assures the lender that the Contractor will complete the work satisfactorily in the stipulated time.

(C) Deferred Payment Guarantee: This type of Guarantee is usually given on deferred or postponed payments. The banks generally offer DPG on the purchase of certain machinery and goods.

3. Letters Of Comfort For Availing Buyers Credit: Letter of Comfort can be understood as the Guarantee offered by the Bank of Importer or buyer. The Importer can use this Letter of Comfort to avail Buyer’s Credit from the Overseas banks. The Importer or Buyer’s Bank charges certain fees for offering the Letter of Comfort.

4. Derivative Products: Derivatives are a type of financial security or financial contracts that are backed by some underlying securities. These underlying securities can be anything, ranging from currencies, bonds, commodities to stocks.

5. Buyer Credit: It is a short-term funding option, offered to the Indian Buyers or Importers by the Bank to manage their import Business. Using Buyer’s Credit, the Importers can avail loans from foreign financial institutions which offer Credit at comparatively lower rates. Buyer’s Credit can be availed for importing almost all types of capital and non-capital goods.

6. Supplier Credit: This type of Credit is used to support the importers financially in India. Here any overseas Financial Institute or Supplier offers the Credit to the Importer on the Libor rates, which are comparatively low. Such Credit is backed by the Letter of Credit offered to the Importer via Importer’s Bank.

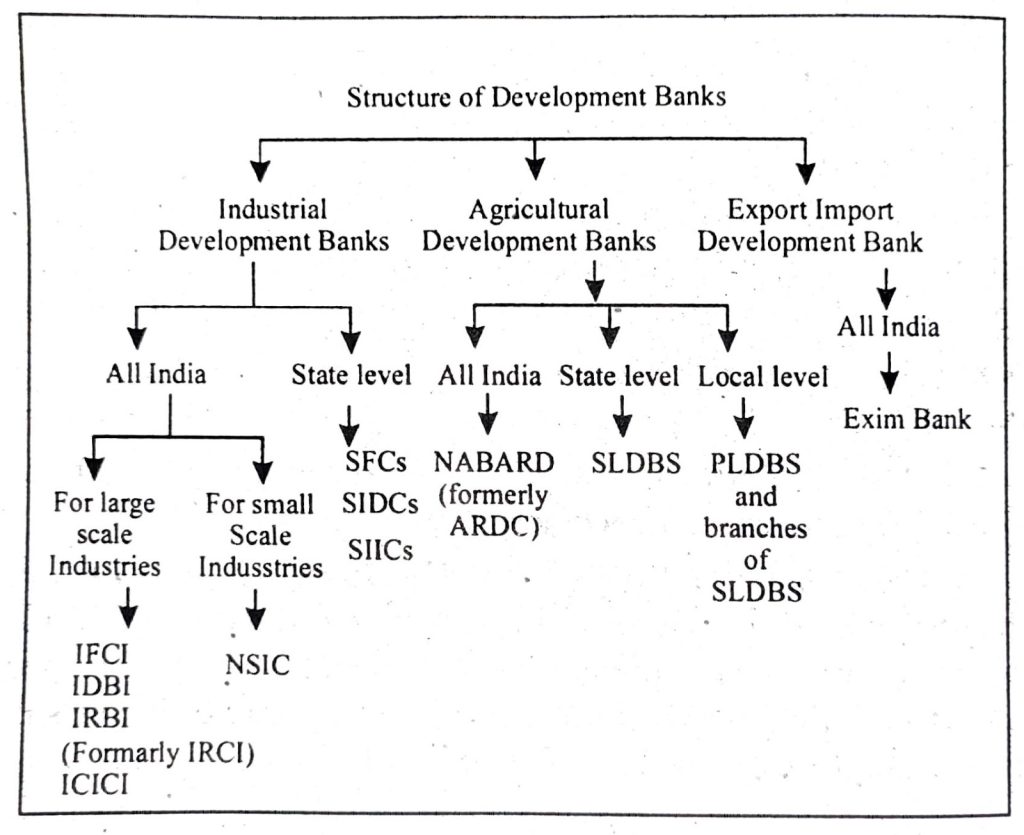

11. Draw a chart of the structure of Development Banks and briefly mention about them.

Ans:

The structure of development banks can be grouped under three wings i.e. Industrial development Banks, Agricultural development Banks and Export Import Development Bank.

Industrial Development Banks are again sub-divided into National and state level. For large scale industrials there are Industrial Finance corporation, Industrial Development Bank of India. Industrial credit and Investment corporation of India and the Reconstruction Bank etc. For small scale industries, NSIC has been taking a leading part. Under State Level, there are SFC s, SIDCs, IICs etc. Under State Level, which play an import part for providing finance to the industrial sectors.

Agricultural Development Banks also sub-divided into all India and state level. Under all India Level NABARD Provide refinance credit to rural sectors. On the loans to agriculture. Further, at the local level, there are Primary land development banks and the branches of SLDBS.

For promoting and developing Exports and imports in all India level institution called the export and Imports Bank of India (EXIM.BANK) was established.

12. Explain the Benefits of Service Guarantee. What are the Types of Service Guarantees? Explain.

Ans: The benefits to the company of an effective service guarantee are as follows:

(i) Sets Clear Standards for the Organisation – It prompts the company to clearly define what it expects of its employees and to communicate that to them. The guarantee gives employees service oriented goals that can quickly align employee behaviours around customer strategies.

(ii) Forces the Company to Focus on its Customers – To develop a meaningful guarantee, the company must know what is important to its customers ― what they expect and value. In many cases “satisfaction” is guaranteed, but in order for the guarantee to work effectively, the company must clearly understand what satisfaction means for its customers (what they value and expect).

(iii) A Good Service Guarantee Studies the Impact on Employee Morale and Loyalty – A Guarantee generates pride among employees.

Through feedback from the guarantee, improvements can be made in the service that benefits customers, and indirectly employees.

(iv) Immediate and Relevant Feedback from Customers – It provides an incentive for customers to complain and, thereby, provides more representative feedback to the company than simply relying on the relatively few customers who typically voice their concerns. The guarantee communicates to customers that they have the right to complain.

(v) Reduces their Sense of Risk and Builds Confidence in the Organisation for Customers – Because services are intangible and often highly personal or ego involving, customers seek information and cues that will help reduce their sense of uncertainty.

Further, previous research has identified four types of service guarantees:

(i) A Specific Guarantee: Signals firm commitment on specific attribute performance such as delivery time or price. Specific guarantees allow customers to evaluate service by disconfirming attribute performance expectations. From the firm’s perspective, a specific guarantee can serve not only as a benchmark to guide employee efforts and firm process design, but also as a performance measure. However, the narrow focus on some attributes may not be highly valued or appreciated by a heterogeneous customer base, although it may appeal to certain segments.

(ii) An Unconditional Guarantee: Promises performance on all aspects of service, and “in its pure form, promises complete customer satisfaction, and at a minimum, a full refund or complete, no cost problem resolution for the payout.” Unconditional guarantees require a slightly different firm approach since variables that determine customer satisfaction such as effect and cognitive evaluations of attribute performance (Oliver) are not within the firm’s control.

(iii) Implicit Guarantee: As the term suggests, it is an unwritten, unspoken guarantee that establishes an understanding between the firm and its customers. Customers may infer that an implicit guarantee is in place when a firm has an outstanding reputation for service quality. The focus of an implicit guarantee is customer satisfaction. Previous research suggests that customers are more likely to rely on explicit firm promises instead of implicit cues to make inferences about the firm.

(iv) An Internal Guarantee: Is “a promise or commitment by one part of the organization to another to deliver its products or services in a specified way or incur a meaningful penalty, monetary or otherwise.” Since implicit guarantees are unconditional guarantees (without formal expression of explicit commitment) and the focus of internal guarantees is limited to coordinating functions and employees, the subsequent discussion includes only specific and unconditional guarantees.

13. Explain the different methods for repayment of loan.

Ans: There are five different methods for repaying a housing loan:

(i) Equal payments: Equal payments is a good option if you want to know exactly when the loan period ends and if your repayment ability allows a possible rise in the interest rate level.

(a) The repayments (instalment + interest) are of equal size at the beginning of the loan period.

(b) The repayment only changes if the interest rate changes.

(c) Initially, the proportion of the installment is small, but it increases during the loan period as the proportion of interest decreases.

(ii) Equal instalments: Equal instalments is your choice if you want to make larger payments at the beginning.

(a) The instalment is always the same, but the repayment amount varies in accordance with the interest: if the reference rate rises, the repayment increases; if the reference rate decreases, the repayment decreases.

(b) If the interest rate remains the same, the proportion of interest decreases as the loan principal decreases.

(iii) Fixed annuity loan: This is a handy repayment method if you want to know exactly how much your repayments will be well into the future, and the duration of the loan period is not as important.

(a) All repayments are of equal amount throughout the loan period.

(b) If the reference rate rises, the loan period is extended; if the reference rate falls, the loan period shortens. The repayment is always at least equal to the amount of interest.

(c) If the interest rate level is very low at the time you draw down the loan, a rise in the interest rate may extend the loan period unreasonably, hindering the amortization of the loan. In such an event you should contact the bank and agree on a new repayment plan.

(iv) Bullet repayment: This option is usually used for temporary financing. The entire principal of a bullet loan is repaid in one go, but there can be several interest payments.

(v) Instalment-free period: During the instalment-free period you only pay interest, not the principal. This extends the loan period or increases future instalments. Read more about the` instalment-free period for a housing loan.

14. What are the Characteristics of Factoring? What are the Types of Factoring? Explain.

Ans: Characteristics of Factoring:

(i) Usually the period for factoring is 90 to 150 days. Some factoring companies allow even more than 150 days.

(ii) Factoring is considered to be a costly source of finance compared to other sources of shoft term borrowings.

(iii) Factoring receiwbles is an ideal financial solution for new and, emerging firms. This is because credit worthiness is evaluated based on the financial strength of the customer (debtor). Hence these companies can leverage on the financial strength of their customers.

(iv) Bad debts will not be considered for factoring.

(v) Credit rating is not mandatory. But the factoring companies usually out credit risk analysis before entering into the agreement.

(vi) Factoring is a method of off balance sheet financing.

(vii) Cost of factoring = finance cost + operating cost. Factoring cost vary according to the transactiOn size, financial strength of the customer etc. The cost of factoring varies from 1.5% to 3% pd month depending upon the financial sffiengrth of client’s customer.

(viii) Indian firms oftr factoring for invoies as low as Rs. 1000. For delayed payments, beyond the approved credit period, a penal charge of around 1-2% per month over and above the normal cost is charged (it varies tike 1% for the first month and 2% afterwards).

Types of Factoring:

(i) Recourse and Non-recourse Factoring: In this type of arrangement, the financial institution, can resort to the firm, when the debts are not recoverable. So, the credit risk associated with the trade debts are not assumed by the factor. On the other hand, in non-recourse factoring, the factor cannot recourse to the firm, in case the debt turn out to be irrecoverable.

(ii) Disclosed and Undisclosed Factoring: The factoring in which the factor’s name is indicated in the invoice by the supplier of the goods or services asking the purchaser to pay the factor, is called disclosed factoring.

Conversely, the form of factoring in which the name of the factor is not mentioned in the invoice issued by the manufacturer. In such a case, the factor maintains sales ledger of the client and the debt is realized in the name of the firm. However, the control is in the hands of the factor.

(iii) Domestic and Export Factoring: When the three parties to factoring, i.e. customer, client, and factor, reside in the same country, then this is called as domestic factoring.

Export factoring, or otherwise known as cross-border factoring is one in which there are four parties involved, i.e. exporter (client), the importer (customer), export factor and import factor. This is also termed as the two-factor system.

(iv) Advance and Maturity Factoring: In advance factoring, the factor gives an advance to the client, against the uncollected receivables.

In maturity factoring, the factoring agency does not provide any advance to the firm. Instead, the bank collects the sum from the customer and pays to the firm, either on the date on which the amount is collected from the customers or on a guaranteed payment date.

15. Explain the Advantages and disadvantages of Factoring.

Ans: Following are advantages of factoring:

(i) Factoring cover the risk arising from a potential customers insolvency, the risk being taken over by the factor, while taking into account that the factor does not cover risks arising from commercial or technical disputes.

(ii) It is provided the treasury supply of the company, the factor paying immediately the claims ceded, after deduction of interest, fee and possibly a collateral deposit created by the factor, elements clearly known when the contract is signed.

(iii) The factoring companies do not provide new funding, but can accelerate the cash conversion cycle for client companies, enabling them to gain the value from debtor, much faster than if they expected to pass the normal period of trade credit, that means it transforms a sale on term within a cash sales, reducing the short-term indebtedness of the company.

(iv) The engagement of factor is similar to a trade receivables collection to the delivery of goods without this funding to appear on the liability side. So, the factoring reduces operating cycle length and the need for working capital, helping to improve the company liquidity.

(v) Unlike traditional bank loans, factoring doesn’t require you to risk your home or other property as collateral. So there is no collateral required.

Following are disadvantages of factoring:

(i) Relatively high cost due to the multiple services they provide. Factoring costs are usually higher than the costs of the bank loans.

(ii) The use of factoring gives the impression of a delicate financial situation of the customer company, but this observation is unfounded because factoring companies do not accept, in principle, than the companies with a very good financial situation. Also, factoring is contracted only when a certain factor knows that client is solvent.

(iii) Client of the factoring may suffer a substantial loss of income, taking into account all fees and risk of loss which is involved.

(iv) By remission of a portion of the commercial relations to a factoring company, the beneficiary company might also lose some contracts, whether with customers because the factor is more exigent with debtors as regards the compliance of maturities, or banks because the factoring exclude the recourse to banks for mobilization of trade receivables. That means some customers do not want the involvement of third parties.

16. Explain core banking growth and development in India. Explain it features.

Ans: Core banking systems are aimed at empowering existing and probable customers to have a greater freedom of their account transactions. With technological evolutions, transactions are now safer, faster and less cumbersome. The fact that these transactions can be executed remotely, from any part of the world has made core banking systems a significant aspect of banking these days.

Core banking always brings down operational costs considerably, ensuring lesser manpower requirement for execution. It also enables greater accountability of the customers. Software application based platforms make core banking systems user-friendly and more efficient. The benefits of core banking systems are multi-faceted – keeping pace with fast-evolving market, simplifying banking processes and making it more convenient for the customers, and expanding the outreach of the banks to remote places.

Features of core banking:

(i) Centralized dashboard: Bankers need a single-view dashboard

to visualize the system in real time. Also, bankers and clients should have access to the same dashboard view; this will help diagnose and solve issues faster.

(ii) Onboarding (with KYC features): Before using the dashboard, the client must sign in to their account with a unique username and password. With KYC features, banks can verify identities of prospective customers when they register. The onboarding process should also be simple enough for users to complete without stress.

(iii) Two-factor authentication: The solution needs to offer two-factor verification to boost security and protect clients’ sensitive data.

(iv) Push notifications: When building a core banking solution for mobile, use push notifications to deliver timely account updates to clients.

(v) Loan management: The core banking solution must allow customers to monitor their loans and schedule payments according to the specified plan.

(vi) Interest calculators: For loan and mortgage payments, users need access to real-time calculators to help them make informed decisions.

17. Give a detailed descriptions of ATM services provided by banks.

Ans: ATM are mini bank without employees. The full meaning of ATM is Automatic Teller Machine that disburses cash. Customers can withdraw cash from the account and get statements on their bank balance using such machines. This is a personalized plastic card bearing a number for each customer. It not only disburses cash but also gives details of the -balance, deposit, cash and cheques and accept mail. It gives accessibility for 24 hrs a day and 365 days in a year. ATM’s facilities are provided inside a bank branch.

The individual banks have their own ATMs and this service is being offered as an additional service on a best effort basis. The customer can withdraw up to a certain specified percentage of his credit limit subject to maximum of some specified amount.

Customer cannot choose the denomination of the currency notes. Machines issue either Rs 1000, Rs. 500, Rs. 100.

To use ATM, customers must know some procedures, otherwise it is very difficult to withdraw money which also consumes unnecessary time.

The procedures are:

(a) Insert the card into the machine where given and wait till the machine indicates to key in the PIN.

(b) Wait for a few seconds till the machine processes the PIN.

(c) Key in the amount of cash needed.

(d) Wait for a few seconds till the ATM card comes out, count the cash and always remember to collect the card before leaving the ATM.

The customers should be very careful while using the ATM The PIN should not be disclosed anyone and handover the card to any unauthorized person or even representative of the bank and should not write down the PIN on the card or anywhere else.

The ATM has several advantages, First, the customers need not go to the bank and have to collect token and make a queues to withdraw money because of the ATMs facility.

18. What are the Advantages and disadvantages of ATM. What are the Facilities provide by ATM?

Ans: There are several advantages of ATM which are discussed below:

(i) Quick and prompt service is possible with less human errors.

(ii) It is beneficial for travelers.

(iii) It provides 24 hrs services without any staff and reduces the work load on bank staff.

(iv) Withdraw cash at any time or in urgent without the help of bank.

(v) It ensures privacy to the customers.

(vi) The withdrawal of rupees is faster than bank, no need of standing long lines.

(vii) Maintenance cost is less as no bank staff is involved in transaction.