Class 11 Finance Chapter 1 Nature And Organization of Bank Question answer to each chapter is provided in the list so that you can easily browse throughout different chapters Assam Board Class 11 Finance Chapter 1 Nature And Organization of Bank and select needs one.

Class 11 Finance Chapter 1 Nature And Organization of Bank

Also, you can read the SCERT book online in these sections Solutions by Expert Teachers as per SCERT (CBSE) Book guidelines. These solutions are part of SCERT All Subject Solutions. Here we have given Assam Board Class 11 Finance Chapter 1 Nature And Organization of Bank Solutions for All Subject, You can practice these here.

Nature And Organization of Bank

Chapter : 1

VERY SHORT TYPE QUESTIONS & ANSWERS

1. What is the nature of a bank?

Ans: Two views exist regarding the nature of the banking business. The dominant view defines banks as financial intermediaries — institutions in the business of transferring money from savers to borrowers. An alternative view advances that banks finance borrowers via money creation.

2. What do you mean by external Organisations of a bank?

Ans: External organisation of a business concern means legal and constitutional form of a business organisation.

3. What is the scope and nature of modern banking?

Ans: Bank is an institution which deals in money and credit. It accepts deposits from the public and grants loans and advances to those who are in need of funds for various purposes. The Banking Regulation Act, 1949 defines banking as an activity of accepting funds from the public for the purpose of lending or investment.

4. Give the definition of banking?

Ans: Banking is defined as the business activity of accepting and safeguarding money owned by other individuals and entities, and then lending out this money in order to conduct economic activities such as making profit or simply covering operating expenses.

5. What is credit creation and what are its limits?

Ans: The total amount of cash available to the banking system limits the volume of credit that can be created. Credit is based on cash. The total volume of credit cannot ordinarily be larger than the total amount of cash available multiplied by the customary reserve-ratio.

6. What is the creation of credit?

Ans: Credit creation separates a bank from other financial institutions. In simple terms, credit creation is the expansion of deposits. And, banks can expand their demand deposits as a multiple of their cash reserves because demand deposits serve as the principal medium of exchange.

7. What do you mean by credit creation by commercial banks?

Ans: In very simple terms, a bank is separated from other financial banks by credit creation. Credit Creation is basically the expansion of the deposits. Also, the banks can expand their demand deposits as a multiple of their cash reserves because the demand deposits serve as a principal medium of exchange.

8. What are the methods of credit creation?

Ans: Quantitative or traditional methods of credit control include banks rate policy, open market operations and variable reserve ratio. Qualitative or selective methods of credit control include regulation of margin requirement, credit rationing, regulation of consumer credit and direct action.

9. Who limits the power of credit creation by commercial banks?

Ans: Cash Reserve Ratio: The credit creation power of banks depends upon the amount of cash they possess. The larger the cash, the larger the amount of credit that can be created by banks. Thus, the bank’s power of creating credit is limited by the cash it possesses.

10. What is credit creation and control?

Ans: Credit control is an important tool used by the Reserve Bank of India, a major weapon of the monetary policy used to control the demand and supply of money (liquidity) in the economy. The Central Bank administers control over the credit that the commercial banks grant.

11. (a) What do you mean by the internal organisation of a bank?

Ans: An Internal Bank can help companies make substantial financial savings by eliminating intercompany flows, capturing cash pool movements and centralising payments. With an Internal Bank, corporations can create centres of excellence and enable shared services for the cash management processes.

(b) What do you mean by the internal organisation of a bank?

Ans: An Internal bank can help companies make substantial financial savings by eliminating intercompany flows, capturing cash pool movements and centralising payments. With an Internal Bank, corporations can create centres of excellence and enable shared services for the cash management processes.

12. What are the internal and external factors that affect a bank?

Ans: The influence of internal factors is under the control of bank management such as loan interest rates, third party funds and bad credit. Whereas external factors are those that are beyond the control of bank management such as inflation and economic growth (GDP).

13. What are the important departments of a commercial bank?

Ans: These divisions vary from bank to bank, but most include some form of the following: loan, credit, auditing, trust, consumer banking and business. Within each division, there is a president and various vice presidents.

14. What is an external organisation?

Ans: External Organisation means a legal entity other than the University, including but not limited to granting bodies, other academic or research institutions, and industry partners.

15. What is the Department of Commercial Bank?

Ans: Commercial banks offer the following products and services to corporations and other financial institutions: Loans and other credit products. Treasury and cash management services. Equipment lending.

16. Who can get a small finance bank licence?

Ans: Small finance banks must be enrolled as a public limited company under the Companies Act, 2013 and will be authorised under Section 22 of the Banking Regulation Act, 1949. Also, it is administered by the terms of the Banking Regulation Act, 1949 & Reserve Bank of India Act, 1934.

17. What is an RBI licence?

Ans: The Reserve Bank of India (RBI) issues licences to entities to carry on the business of banking and other businesses in which banking companies may engage, as defined and described in Sections 5 (b) and 6 (1) (a) to (o) of the Banking Regulation Act, 1949, respectively.

18. Do payment banks give loans?

Ans: As per RBI guidelines, payments banks can not accept fixed or recurring deposits. A payments bank is not allowed to give any form of loan or issue a credit card, which is also a form of unsecured personal loan.

19. Who can create credit money?

Ans: Bank deposits are sometimes referred to as ‘credit money’, because the majority of bank deposits were originally created by banks issuing new loans. A bank creates credit money when generating a bank deposit that is a consequence of fulfilling a loan agreement, extending an overdraft facility, or purchasing assets.

20. Can you start a bank with no money?

Ans: Some banks allow you to open an account for free while others require a minimum opening balance. Other banks may charge you a small one-time or monthly fee to open and hold the account.

21. What is a branch for a bank?

Ans: A bank branch is a physical location of a banking corporation, such as Chase, Bank of America or Wells Fargo. These buildings are technically referred to as “brick-and-mortar” branches, and they provide face-to-face service for customers of a bank.

22. Why do we need to open a branch?

Ans: Opening a branch company can offer visibility and brand exposure which can positively influence a company’s profits. A branch office can also reduce the risk of doing business in the host country by allowing the opportunity to test products in new markets.

23. What is a branch network?

Ans: Branch networking refers to the elements used to distribute information to, from and among remote sites, stores, branch offices, and data centres. Multi-site companies of all sizes, school systems, retailers and other distributed organisations of all kinds are operating branch networks.

24. What is the role of branch banking?

Ans: Branch banking allows a financial institution to expand its services outside of its home location and into smaller storefronts that function as extensions of its greater operations.

25. What are the internal and external factors that affect a bank?

Ans: The influence of internal factors is under the control of bank management such as loan interest rates, third party funds and bad credit. Whereas external factors are those that are beyond the control of bank management such as inflation and economic growth (GDP).

26. What is the cash reserve ratio in RBI?

Ans: Cash Reserve Ratio (CRR) is the share of a bank’s total deposit that is mandated by the Reserve Bank of India (RBI) to be maintained with the latter as reserves in the form of liquid cash.

27. What is SLR and CRR?

Ans: CRR is the percentage of money, which a bank has to keep with RBI in the form of cash. On the other hand, SLR is the proportion of liquid assets to time and demand liabilities.

28. What is SLR in banks?

Ans: Statutory Liquidity Ratio or SLR is a minimum percentage of deposits that a commercial bank has to maintain in the form of liquid cash, gold or other securities. It is basically the reserve requirement that banks are expected to keep before offering credit to customers. The SLR is fixed by the RBI.

29. What is the most important department in a bank?

Ans: Modern banks are huge entities employing thousands of people in their workforce. However, amongst the various departments present at banks, the treasury department is the most important as well as the least understood.

30. What is cash credit?

Ans: A cash credit is an arrangement through which a banker permits his customer having current account to borrow money upto certain limit against an agreement supported by a bond of credit against securities.

31. What is Loan?

Ans: Loan is an advance in a lump sum amount the whole of which is withdrawn and is supposed to be repaid generally wholly at one time.

32. Give the meaning of Cash Reserve Ratio.

Ans: The Cash Reserve Ratio refers to the portion of total deposits of a commercial bank which it has to keep with the RBI, in the form of Cash Reserves, on 30th April, 2003 the CRR was reduced by 0.5% to bring it to 5%.

33. What is overdraft?

Ans: An overdraft is an arrangement by which the customer is allowed to overdraw his account. It is granted against some collateral securities. The facility to overdraw is allowed through a current account only. Interest is charged on the exact amount overdrawn subject to the payment of a minimum amount by way of interest.

SHORT & LONG TYPE QUESTIONS & ANSWERS

1. What are the features of Bank?

Ans: The features of a Bank are:

(a) A Bank is a profit seeking commercial enterprise.

(b) It deals in money, i.e., it accepts deposits from the public and advances loans to the needy borrowers.

(c) It deals with credit. It creates credit for the purposes of lending money.

(d) The deposits made with the bank are repayable on demand and can be withdrawn by the depositor by means of any instruments whether a cheque or otherwise.

2. What are the two types of bank deposits?

Ans: The two types of Bank deposits are:

(a) Primary deposits and

(b) Derivative deposits.

(a) Primary deposits: The money deposited by a depositor in different deposit accounts such as savings accounts etc. is known as Primary Deposits. These are also known as Passive deposit or cash deposits.

(b) Derivative deposits: Derivative deposits are those which are created by the bank while lending money. It is also called secondary deposit or passive deposit.

3. Give the meaning of SLR and CRR.

Ans: The cash reserve ratio (CRR) is a certain percentage of bank deposits which a commercial bank is required to keep as cash reserves with itself. The statutory liquidity ratio (SLR) refers to the ratio of deposits which the commercial banks have to maintain a certain percentage of their total deposits and time deposits with themselves in the form of liquid assets, as per the directions of RBI.

4. Give the meaning and definition of Bank.

Ans: A Bank is a financial institution which deals with money and credit. Different scholars have defined banks differently.

According to Dr. H. L. Hart “A banker is one who in the ordinary course of business honours cheques drawn upon him by persons from and for whom he receives money on current account.”

Section 5 of the Banking Regulations Act, 1949 defines banking as the “Accepting, for the purpose of buying and investment, of deposits of money from the Public repayable on demand or otherwise and withdrawable by cheque, draft, order or otherwise.

5. Discuss the general utility functions of a Bank.

Ans: Modern banks render various services for their customers.

The important utility services are:

(i) Safe custody services for the valuable documents, deeds, securities, ornament, gold etc.

(ii) Dealing in foreign exchanges.

(iii) Issuing letter of credit, circular notes, travellers cheques etc.

(iv) Acting as referee about financial standing, business reputations and respectability of customers.

(v) Underwriting loans raised by the government, public bodies etc.

(vi) Advisory services to customers.

(vii) Issuing credit cards etc.

(viii) ATM services.

6. What are the Secondary functions of a bank?

Ans: The secondary functions of a bank are:

(a) Agency functions: These functions are performed by the banker for its own customer. For these services, the bank charges certain commission from its customers.

These functions are:

(i) Remittance of funds.

(ii) Collection and payment of credit instruments.

(iii) Execution of standing orders.

(iv) Purchase and sale of securities.

(v) Collection of Dividend and interest.

(vi) Income tax consultancy.

(b) General Utility functions: These are certain utility functions performed by the modern commercial bank to its customer for the community.

These are:

(i) Safe custody of valuables.

(ii) Issuing letters of credit.

(iii) Gift Cheques.

(iv) Dealing in foreign exchange.

(v) Credit cards.

(vi) Collection of statistics.

7. Write a short note on the External organisation of Bank.

Ans: External organisation of a Commercial Bank is formed on the basis of Prevailing Banking laws. The structure of external organisation of Commercial Bank may either be Public, Private or Co-operative. Moreover, the organisation may either be sole-proprietorship, partnership or a joint stock company. It may also be established and managed either in the public or private sector.

The commercial banks are generally set up on joint stock company basis. So, setting up such companies has to comply with the formalities of Indian Companies Act. But with the Passing of Banking Regulation Act 1949, the banks are to follow the rules and regulation included in the Act. Hence, in order to form a bank the entrepreneurs must comply with both the Acts, namely, Indian Companies Act 1956 and the Banking Regulation Act 1949.

8. What are the functions of loan and advances?

Ans: These are not only very important functions but also the chief sources of profit to most of the banks in a modern economy. The bank gives loans and advances to businessmen, traders and others against documents of title to goods and marketable securities. Loans are also given against the personal security of the borrower with or without a surety. The bank selects such investments from where money can be easily called bank. Therefore, a bank is able to help not only merchants but also those who, in turn, may use funds not only to their advantage but also to the advantage of the community.

According to sec. 20 of the Banking Regulation Act 1949, there are some restrictions on loans and advances. According to this said sec. a banking company shall not –

(a) Grant any loans or advances on the security of its own shares, or

(b) Enter into any commitment for granting any loans or advances to on behalf of –

(i) Any of its director

(ii) Any firm in which any of its directors is interested as partner, manager, employee or guarantor or

(iii) Any company of which any of the director of the banking company is a director, manager, employee or guarantor or in which he holds substantial interest, or

(iv) Any individual in respect of whom any of its directors is a partner or guarantor.

9. What are the various forms of loans and advances granted by a bank to the drawer?

Ans: The various forms of loans and advances that the bank grants to a drawer are:

(a) Ordinary loans: The money or specific amount landed by a bank to a borrower with or without security is known as loan or Ordinary loan. It is given for a fixed period and interest is charged on the entire amount of loan from the date of sanction.

(b) Cash Credit: The agreement by which a bank allows his customer to borrow money up to a certain limit against some tangible securities is known as Cash Credit. Interest is charged on the actual amount utilised by the borrower and for the period of actual utilisation only.

(c) Overdrafts: The agreement with a bank by which a current account holder is allowed to withdraw money more than his balance up to a certain limit is known as Overdraft.The customer has to pay interest on the amount overdraw by him.

(d) Purchasing and discounting of bills: It is the most important function of the bank in which a bank lends money without any collateral security. In this case, the customer having a bill gets immediate finance from the bank and does not have to wait till the maturity of the bill.

10. Describe the origin and evolution of the Bank.

Ans: There seems to be no unanimity amongst the economists about the origin of the word ‘Bank.’ According to some economists, the word ‘Bank’ has been derived from the German work ‘BANC’ which means a joint stock firm, while others say that it has been derived from the Italian word ‘BANCO’ which means a heap. At the establishment of Bank of Venice in 1157, the Germans were influential and hence, perhaps the word ‘BANC’ or ‘BANCO’ was used by Italians to denote the accumulation of securities or money with a joint stock firm, which later on known as Bank.

Another group of people believe that the word ‘Bank’ has been derived from the Greek work ‘BANQUE’ which means a bench. In the olden days Jews entered into money transactions sitting on benches in a market place. When the bankers were not in a position to meet his obligations, the bench on which he was carrying on the money business was broken into pieces and he was taken an Bankrupt.

It is possible to trace the history of commercial banking to ancient times. The business of Banking is as old as the civilization itself. As early as 2000 B.C., the Babylonians had developed a system of banks. They used their temples for lending at higher rates of interest against gold and silver which had been left with them for safe custody. The Greek temples were used as depositories for people’s surplus funds and these were the centres of money lending transactions. The Priests of the temples acted as financial agents till they lost Public Confidence on account of people’s disbelief in religion.

Alfred Marshall in his book “Money, credit and commerce” writes that, “in Greece, the temples of Delphi and other safer places acted as store houses for the precious metals before the days of coinage in later times, they lent out money for public and private purposes at interest though they paid none themselves.” In ancient times, private money changers accepted deposits at lower rates of interest and loaned them out at higher rates of interest, even allowing drafts to be drawn on them. Banking was also known in ancient Rome and with the revival of trade and commerce in the middle ages, it became more prominent.

In India, the ancient Hindu scriptures refer to the money lending activities in the vedic period. During the era of Ramayana and Mahabharata, Banking had become a full-fledged activity. The reference to money lending business is found in the Manu Smriti also.

In the middle age, in Italy the first bank called the ‘Bank of Venice’ was established in 1157.

In England, the bankers of Lombardy had taken the initiative to start modern banking along with their trading activities in London. But commercial banking began there only after 1640, when goldsmiths started receiving deposits from the public for safe custody and issued receipts for the acknowledgement which were being used as bearer demand notes later on.

Crowther speaks about three ancestors of modern commercial bank viz. the merchant, the money lender and the goldsmith the merchants or traders issued documents like hundi to remit the funds. Modern banks introduced cheques or demand drafts for remittance purposes. Money lenders give loans. Bankers also gave loans, goldsmiths received deposits and created credit. Banks also received deposits and adopted the process of credit creation by issuing cheques and giving loans. All this goes to show that banking originated in the distant past.

11. Explain the function of Commercial Banks.

Ans: The functions of Commercial Banks can be explained by the following two categories:

(A) Primary function or services of Commercial Banks and

(B) Secondary functions or services of Commercial Banks.

(A) Primary functions: The primary functions of commercial banks are:

(i) Accepting of Deposits: Deposits are an important source of Bank’s funds. They can broadly be classified into three categories.

(a) Savings Deposits: These deposits are of small amounts and are accepted by banks to encourage persons of small means to make savings. Frequent withdrawals are not allowed.

(b) Fixed Deposits: Money in this account is accepted for a fixed period. Say one year or more. The money so deposited can not be withdrawn before the expiry of the fixed period. The rate of interest on this account is higher than that on other accounts. The longer the period, the higher is the interest.

(c) Current Account: The depositor can withdraw the money from this current account whenever he requires it. In general, the bank grants no interest on this account because it has to keep the cash ready at all times to meet the requirements of the depositor. This account is generally opened by businessmen who may have to withdraw money several times a day.

(ii) Lending of money: A major portion of the deposits received by a bank is lent by it. This is also the major source of a bank’s income. However, lending money is not without risk and therefore, a banker must take proper precautions in this process. The lending may be in any of the following forms.

(a) Loan: It is a kind of advance made with or without security. It is given for a fixed period at an agreed rate of interest. The amount of loan is usually credited to the credit of the customer’s account who may withdraw from there as per his/her requirements. The loan may be secured or unsecured.

(b) Cash credit: It is an arrangement by which a banker allows his customer to borrow money up to a certain limit against security of goods.

(c) Overdraft: It is an arrangement whereby a customer has been allowed temporarily to overdraw his current account. It is without any security.

(d) Discounting Bills of exchange: This is another type of lending done by the banks. If the holder of an exchange bill needs money immediately, he can get it discounted by the bank. After deducting its commission, the bank pays the present price of the bill to the holder when the exchange bill matures the bank can secure its payment from the party which had accepted the bill.

(B) Secondary functions/ services of commercial Banks: This function or services can be classified into the following two categories:

(a) Agency service: In many cases the commercial banks act as the agents of their customers. As agents they provide the following services.

(i) Collection of drafts, bills, cheques, dividends etc. on behalf of customers.

(ii) Execution of standing orders of the customers viz. payment of subscription, rent, bills, promissory notes, insurance premium etc.

(iii) Conducting stock exchange transactions, i.e. purchasing and selling of securities for the customers.

(iv) Acting as a correspondent or representative of customers, other banks and financial corporations.

(v) Functioning as an executor, trustee or administrator of an estate of a customer.

(vi) Preparation of income tax return, claiming of tax refunds and checking of assessments on behalf of the customers.

(b) General utility or Miscellaneous Services: Modern banks render various services for their customers.

The important utility services are:

(i) Safe custody services for the valuable documents, deeds, securities, ornament, gold etc.

(ii) Dealing in foreign exchanges.

(iii) Issuing letter of credit, circular notes, travellers cheques etc.

(iv) Acting as referee about financial standing, business reputations and respectability of customers.

(v) Underwriting loans raised by the government, public bodies etc.

(vi) Advisory services to customers.

(vii) Issuing credit cards etc.

(viii) A.T.M. services:

12. Explain the process of creation of credit by commercial Banks.

Ans: Credit creation is an important function of Commercial Banks. The power of commercial banks to expand deposit through expanding their loans and advances is known as credit creation. The famous economist Sayers has rightly said “Banks are not merely purveyors but also, important manufacturers of money.” A modern bank creates deposits in two ways.

Firstly in a passive way which results in primary or passive deposits and secondly in a more active way which results in active or derivative deposits. The primary deposit do not make any net addition to the stock of money in the economy. The derivative deposits are created by the bank by opening an account in the name of the person who borrows funds from the bank. In short the process of credit creation is as under.

When the borrower is granted a loan by the bank, an account is opened in the name of the loanee and the loan money is credited to his deposit account. The loan money is not paid to the borrower in cash. The borrower can withdraw the amount either in full or as per his needs. When the borrower pays to his creditors, a cheque is drawn upon his account with the bank. The creditor on receipt of the cheque may deposit in his account in another bank. The other bank which receives the primary deposit in the form of cheque drawn upon the first bank.

After keeping some cash, as per cash reserve ratio, the second bank can create a derivative deposit by giving a loan to some other borrower. The second borrower may make the payment out of his account to another creditors, who may have an account to another creditors, who may have an account with the third bank, which in turn will receive the primary deposit in the form of cheque drawn on the second bank.

This process goes on creating a multiple of the initial amount deposited with the first bank. In this way commercial banks are able to multiply loan and investments and thus multiply deposits. Credit creation can thus be defined as the expansion of bank deposits through the process of more loans and advances and investments.

A simple example is given below to illustrate the process by which multiple credit creation by a commercial bank takes place.

Suppose the cash reserve ratio is 20%. A new deposit of Rs. 1000/-has been made with Bank A. The bank’s balance sheet has the following position —

Balance sheet of Bank A

| Liabilities | Rs. | Assets | Rs. |

| Deposit | 1000 | Cash | 1000 |

| Total | 1000 | Total | 1000 |

Mr. ‘X’ approaches bank A for a loan. The bank keeps 20% of the initial deposit as reserves and advances the remaining 80% as loan to Mr. X. After having given the loan, the balance sheet of Bank A has the following position.

Balance sheet of Bank A

| Liabilities | Rs. | Assets | Rs. |

| Deposit | 1000 | Cash | 200 |

| Loans to X | 800 | ||

| Total | 1000 | Total | 1000 |

‘X’ who is indebted to Y gave him the cheque of Rs. 800 which Y deposits with his Bank ‘B’. The balance sheet of Bank ‘B’ appears as follows

Balance sheet of Bank B

| Liabilities | Rs. | Assets | Rs. |

| Deposit | 800 | Cash | 800 |

| Total | 800 | Total | 800 |

Z approaches bank ‘B’ for a loan, Bank ‘B’ keeps 20% as reserves and lends out 80% of its deposits. The balance sheet of Bank B now appears as follows —

Balance sheet of Bank B

| Liabilities | Rs. | Assets | Rs. |

| Deposit | 800 | Cash | 160 |

| Loan to Z | 640 | ||

| Total | 800 | Total | 800 |

Now Z pays Rs. 640 by cheque to P who deposits it with bank ‘C’ and so on.

13. Explain briefly the limitations of credit creation.

Ans: The limitation of credit creation are as follows:

(i) Availability of primary deposits: The bank can create credit only when it has necessary cash in the form of primary deposits. In other words the larger the amount of cash with the bank, the larger will be its capacity to create deposits and vice versa.

(ii) Banking habits of the people: The creation of credit also depends upon the popularity of banks among the general public. In case, the people lack banking habit, that is they like to hold more cash with them, the bank will have lower capacity to create credit.

(iii) Business conditions: In a depression period, there is a fall in business activities and therefore there is less demand for bank credit. Hence, the banks will be in a position to create less credit.

(iv) Use of credit instruments: Where credit instruments like cheque, bills etc. are frequently used by the people, the banks are required to keep a smaller amount of cash reserves. On the other hand, the countries where the people are using currency notes and coins to make all kinds of payments, the banks will have larger cash reserves, therefore, their power to create credit will be limited.

(v) Nature of security offered: The availability of good securities places a limit on the power of banks to create money. Every loan made by a bank is secured by some valuable form of wealth bills, shares, stocks etc. Thus, if approved securities are not available, the bank cannot create credit fearlessly.

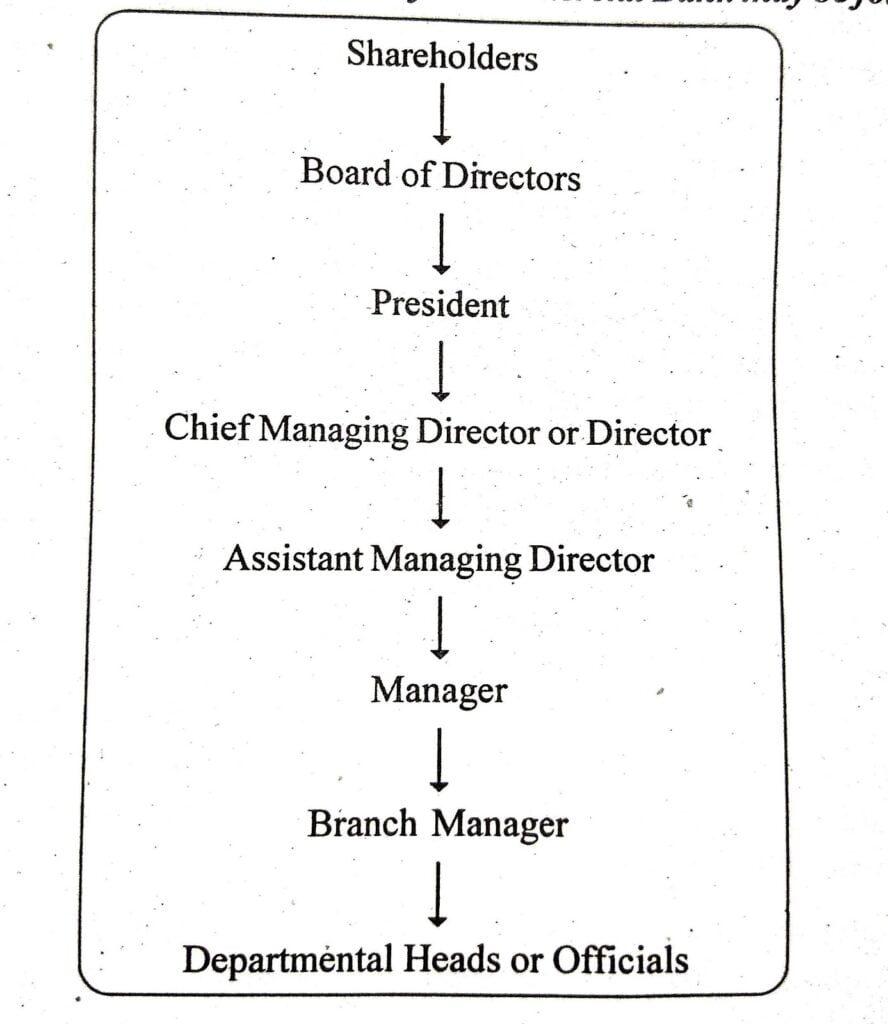

14. What do you mean by the internal organisation of a commercial bank?

Ans: Internal organisation of a Commercial Bank means functioning of Banking business by the management. In any company the shareholders are the true owners. But the company delegates their authority to a Board of Directors for its functioning. The Board of Directors appoint a President who is in the overall charge for the management, direction and proper control of the bank activities. He is appointed as a “whole-time President.”. Some other subordinate officials help him in discharging his duties.

The whole internal organisation of a Commercial Bank may be follows:

15. Describe the different departments of a Bank.

Ans: The various departments of Commercial Banks are:

(i) Secretary Department: It looks after the secretarial works within the department like taking necessary action for organising meetings, preparation of agenda etc.

(ii) Law Department: It looks after the matters relating to law. Such as payment of income tax on behalf of shareholders, payment of sales tax etc.

(iii) Accounts Department: The accounts department is responsible for maintaining the accounts books like Profit and Loss, income and expenditure.

(iv) Statistics Department: The statistics department is in charge of keeping statistical reports of the various activities of the bank. For example Systematic record of performance of various departments that may help in future comparison etc.

(v) Loan Department: Large commercial banks have a loan department which looks after the loan related policies. For example, whom to give loans to, how to give loans etc.

(vi) Inspection Department: The inspection department looks after the working of the various departments. On the basis of the reports by this department, future plans and programmes are formulated.

(vii) Regional or Branch Manager Department: The main function of the Regional or Branch manager department is to see whether the principle and procedure of the banks are functioning effectively.

(viii) Printing and Publishing Department: The printing and publishing department is to arrange for printing necessary forms. Such as counter file cheques, bank reports etc.

16. State about the formation of capital of a Bank.

Ans: According to sec. 11 of the Banking Regulation Act 1949 the requirement of capital for a Bank are given as follows:

For & Banking Company incorporated in India, the minimum aggregate value of its paid up capital and Reserves are:

(i) If it has places of business in more than one state Rs. 5 lakhs.

(ii) If any such place or places of Business is / are situated in Mumbai or Calcutta or both Rs. 10 lakhs.

(iii) If it has all its places of business in one state none of which is situated in the city of Mumbai or Kolkata.

(a) In respect of the Principal place of business Rs. 1 lakh Plus.

(b) In respect of each of its other places of business situated in the district of principal business Rs. 10,000 Plus.

(c) In respect of each place of business situated elsewhere in the state outside the same district subject to a total of Rs. 5 lakhs.

(iv) If it has only a place of business Rs. 50,000.

(v) If it has all its places of business in one state, one or more of which is/are situated in the city of Mumbai or Kolkata in respect of each place of business situated outside the city of Mumbai or Kolkata. Subject to a total of Rs. 10 lakhs Rs. 25000

In case of a banking company incorporated outside India, the aggregate value of its paid up capital reserves must not be less than Rs. 15 lakhs and if it has place of business in the city of Mumbai or Kolkata or both Rs. 20 lakhs.

Sec. 12 of Banking Regulation Act regulates the relationship between authorised, subscribed and paid up capital of banking companies. The paid up capital should be at least one half of the authorised capital of the bank. If the capital happens to be increased the rules must be complied with within a period not exceeding two years as the Reserve Bank may allow,

17. State the provision of issuing licence to commercial banks.

Ans: Under sec 22 every bank which wishes to commence banking business in India must obtain a license from the RBI. Before granting this licence, the Reserve Bank may require to be satisfied by inspection of the books of the company or otherwise, that all or any of the following conditions are fulfilled.

(a) That the company is or will be in a position to pay its depositors in full.

(b) That the affairs of the company do not go against the interest of its depositors.

(c) In the case of foreign companies that the carrying on the banking business by such a company in India will be in the public interest and that the government or law of the country where such a company is incorporated does not discriminate in any way against banking companies registered in India.

Cancellation of the licence: The RBI may cancel a licence in case —

(a) Where the company ceases to carry on banking in India.

(b) At any time fails to comply with any of the conditions imposed by the RBI. The Banking Company aggrieved by such decision may appeal to the central Govt. within 30 days of communication of the decision, whose decision in this regard shall be final.

18. Write short notes on Branch Expansion.

Ans: Under the provision of sec. 23 of the Banking Regulation Act 1919, the Reserve Bank has been empowered to control the opening of new and transfer of existing places of Business of Banking Companies as follows –

(i) Without obtaining the Prior Permission of the Reserve Bank:

(a) No banking company shall open a new place of Business in India or change otherwise than within the same city, town or village, the location of an existing place of business situated in India.

(b) No banking company incorporated in India shall open a new place of business outside India or change, otherwise than within the same city, town or village, the location of an existing place of business situated in that country or area, Provided no permission is required to open for a period of not exceeding one month of a temporary place of business within a city, town or village.

(ii) Before granting any permission under this section, the Reserve Bank may require to be satisfied by an inspection under sec. 35 regarding the financial condition and history of the company, management, the adequacy of capital structure, change of location, place of business etc.

(iii) The Reserve Bank may grant permission under subsection (i) subject to such conditions as it may think fit to impose either generally or with reference to any particular case.

(iv) Where a banking company has failed to comply with any of the conditions imposed on it, the Reserve Bank may take action and revoke any permission granted under this section.

(v) Any Regional Rural Bank requiring the permission of the Reserve Bank under this sec. shall forward its application to the Reserve Bank through the National Bank which shall give its comments on the merits of the application and send it to the RBI.

19. Discuss the nature of the Bank.

Ans: The Bank is a kind of financial institution. It transacts mainly money, financial papers, credit etc. In this regard its nature is separated from that of other institutions. Banks earn profit by transacting money and it exists on the basis of profit. The major portion of income of the Bank comes from accumulated profit. So from this point of view bank is a business institution in nature.

The main business of the Bank is to provide credit for the purpose of earning profit. On the other hand it accepts deposits from different persons, institutions of the society. The deposited money or collected money is also provided in the field of industry, trade and commercial institutions etc. to strengthen the economic position of a country. In this regard it takes the role both as debtor and creditor.

Bank mobilises the saving habit among the different parts of the society. The savings are invested in different productions as their capital. Bank acts as a mediator in between savers and investors. Profit of Bank comes from the difference of interest earned and the same are paid to customers.

The notable point is that the Bank Creates money by innovative techniques. The nature of deposit and credit facilities of Commercial Banks is different from other credit systems. The agricultural Bank, Industrial Banks etc. provide long term credit facilities and accept deposits also by the same manner, on the other hand the major portion of the credit of commercial Banks are provided on short period of time. They cannot provide long term credit facilities because they are bound to meet the customers demand.

The Banking System is an important part of the economy of a country. The economic conditions are influenced by the development of banks and vice-versa.

The Commercial Bank acts as a financial adviser. As an agent of the customer, the bank purchases and sales of shares, debentures etc. of the company and pay salary, pension etc.

20. Explain the primary functions of a Bank.

Ans: Deposits are an important source of Bank’s funds. They can broadly be classified into three categories.

(a) Savings Deposits: These deposits are of small amounts and are accepted by banks to encourage persons of small means to make savings. Frequent withdrawals are not allowed.

(b) Fixed Deposits: Money in this account is accepted for a fixed period. Say one year or more. The money so deposited can not be withdrawn before the expiry of the fixed period. The rate of interest on this account is higher than that on other accounts. The longer the period, the higher the interest.

(c) Current Account: The depositor can withdraw the money from this current account whenever he requires it. In general, the bank grants no interest on this account because it has to keep the cash ready at all times to meet the requirements of the depositor. This account is generally opened by businessmen who may have to withdraw money several times a day.

21. What do you mean by Commercial Bank? Explain the generally utility and agency services of Commercial Bank.

Ans: A Bank is a financial institution which deals with money and credit. Different scholars have defined banks differently.

Agency service: in many cases the commercial banks act as the agents of their customers. As agents they provide the following services.

(i) Collection of drafts, bills, cheques, dividends etc. on behalf of

(ii) Execution of standing orders of the customers viz. payment of subscription, rent, bills, promissory notes, insurance premium etc.

(iii) Conducting stock exchange transactions, i.e. purchasing and selling of securities for the customers.

(iv) Acting as a correspondent or representative of customers, other banks and financial corporations.

(v) Functioning as an executor, trustee or administrator of an estate of

(vi) Preparation of income tax return, claiming of tax refunds and checking of assessments on behalf of the customers.

General utility or Miscellaneous Services : Modern banks render various services for their customers.

The important utility services are:

(i) Safe custody services for the valuable documents, deeds, securities, ornament, gold etc.

(ii) Dealing in foreign exchanges.

(iii) Issuing letter of credit, circular notes, travellers cheques etc.

(iv) Acting as referee about financial standing, business reputations and respectability of customers.

(v) Underwriting loans raised by the government, public bodies etc.

(vi) Advisory services to customers.

(vii) Issuing credit cards etc.

(viii) ATM services.

22. What is credit control? Explain the objectives of credit control.

Ans: Credit control is the regulation of credit by the central bank for achieving some definite objectives. Modern economy is a credit economy because credit has come to play a major role in setting all kinds of monetary and business transactions in the modern economic system. Changes in the volume of credit influence the level of business activity and the price level in the economy.

Unrestricted credit creation by the commercial banks, by causing wide fluctuations in the purchasing power of money, may pose a serious threat to the national economy. Hence, it becomes necessary for the central bank to keep the creation of credit under control in order to maintain stability in the economic system.

Objectives of Credit Control: The important objectives of credit control are given below:

(a) Price Stability: Violent price fluctuations cause disturbances and maladjustments in the economic system and have serious social consequences. Hence, price stability is an important objective of credit control policy. The central bank, by regulating the supply of credit in accordance with the commercial needs of the people, can bring about price stability in the country.

(b) Economic Stability: Operation of the business cycle brings instability in a capitalist economy. The objective of the credit control policy of the central bank should be to eliminate cyclical fluctuations and ensure economic stability in the economy.

(c) Maximisation of Employment: Unemployment is economically wasteful and socially undesirable. Therefore economic stability with full employment and high per capita income has been considered as an important objective of credit control policy of a country.

(d) Economic Growth: The main objective of credit control policy in the underdeveloped countries should be the promotion of economic growth within the shortest possible time. These countries generally suffer from the deficiency of financial resources. Hence, the central banks in these countries should solve the problem of financial scarcity through planned expansion of bank credit.

(e) Stabilisation of the Money Market: Another objective of the central bank’s credit control policy is the stabilisation of the money market to reduce the fluctuations in the interest rates to the minimum. Credit control should be exercised in such a way that the equilibrium in the demand and supply of money should be achieved at all times.

(f) Exchange Rate Stability: Exchange rate stability can also be an objective of credit control policy. Instability in the exchange rates is harmful for the foreign trade of the country. Thus, the central bank, in countries largely dependent upon foreign trade, should attempt to eliminate the fluctuations in the foreign exchange rates through its credit control policy.

23. Briefly explain the agency services rendered by commercial banks.

Ans: The various agency services rendered by the commercial Banks are discussed below:

(a) Remittance of funds: Banks help their customers in transferring funds from one place to another through cheques, drafts etc.

(b) Collection and payment of Credit Instruments: Banks collect and pay various credit instruments like cheques, bills of exchange, promissory notes etc.

(c) Purchasing and Sale of securities: Banks undertake purchase and sale of various securities like shares, stocks, bonds, debentures etc. on behalf of their customers. Banks neither give any advice to their customers regarding these investments, nor levy any charge on them for their service, but simply perform the function of a broker.

(d) Income Tax Consultancy: Sometimes bankers also employ income tax experts not only to prepare income tax returns for their customers but to help them to get refund of income tax in appropriate cases.

(e) Acting as Trustee and Executor: Banks preserve the wills of their customers and executive them after their death.

(f) Acting as Representatives and correspondent: Sometimes the banks act as representatives and correspondents of their customers. They get passports, travellers, tickets, secure passages for their customers and receive letters on their behalf,

24. Discuss the evolution and growth of Commercial Banking in India.

Ans: Modern joint stock commercial banking in India started from the beginning of the 19th century. The earliest commercial banks were known as agency houses and they were started by the employees of the East India Company. The bank offices were confined largely to the Port Cities of Bombay, Calcutta and Madras (Now Mumbai, Kolkata and Chennai). The Agency houses were mainly trading concerns and they combined banking and trading functions together. Several banks were established on an unlimited liability basis mainly by the English Agency houses.

Alexander and Co. established the first joint stock, The Bank of Hindustan in 1770 at Calcutta. It was wound up in 1832. The Banks so established by the Agency houses failed due to mismanagement and speculation. So to revive the situation, the East India Company was established, The Bank of Bengal in 1809, The Bank of Bombay in 1840 and The Bank of Madras in 1843.

These Banks were known as Presidency Banks. In 1860, an Act was passed permitting the establishment of banks on limited liability basis. From 1865 till the end of the 19th century the creation of joint stock banks was very slow. A few banks were started during the last Quarter of the 19th century such as the Allahabad Bank. The Oudh Commercial Bank and floatation was followed by a banking crisis during 1913-17.

In 1920, the “Imperial Bank of India Act” was passed to amalgamate the three Presidency Banks. The Imperial Bank of India was established in 1921 by amalgamating the three Presidency Banks. The Bank was empowered to hold government funds and manage the public debt.

The second world war brought about a revolutionary change in the Indian banking system. The deposits of the banks increased as a result of heavy wartime expenditure. The banking scene in India changed completely after independence. The system as whole recorded rapid progress. The change became possible with passing of the Banking Regulations Act 1949. It is considered to be a big landmark in the history of commercial banking in India. The Act was passed with the object of consolidating and regulating the banking system in India.

The State Bank of India was established by nationalising the Imperial Bank of India in 1955. In 1959 the State Bank India and its associates Act was passed and accordingly public sector Banks were extended. In 1969 fourteen (14) major Indian Commercial Banks were nationalised and in 1980 six more Banks were nationalised. The National Bank for Agriculture and Rural Development (NABARD) was established in 1982 to develop the agricultural sector.

Another development of banking institutions in India has the establishment of various industrial development banks to facilitate industrial growth and balanced economic development. Such institutions are IDBI, IFCI, LIC ICICI, IDBI, SFC, etc.

The EXIM Bank was set up in 1982 for the purpose of financing and promoting foreign trade in India.

25. Discuss the performance of Commercial Banks after nationalisation.

Or

Discuss the progress / achievements of nationalisation of Commercial Banks.

Ans: Various progress or achievements of nationalisation of commercial bank are discussed below:

(i) Expansion of Bank Branches: There has been a rapid expansion of bank branches mainly the commercial bank not only in urban or city areas but also in rural areas which were neglected by commercial banks before nationalisation. At the end of June 1969, there were only 8262 branches whether in June 2003 the number of branches increased upto 32,643. Thus, we can say that after nationalisation the branch expansion was very speedy in different parts of the country.

(ii) Growth of Deposit: The mobilisation of deposit was another significant achievement of public sector banks after nationalisation. The main cause of deposit mobilisation was the expansion of branches in various places. Modern techniques of deposit were adopted by the bank and the number of deposit accounts increased.

(iii) Expansion of credit: After the nationalisation of banks there has been an extension of banking facilities in rural areas for which deposits were increased remarkably among the people of rural areas. There was an improvement in the banking habits among the rural people in terms of deposit and credit.

(iv) Priority Sector Lending: The priority sector which include agriculture, small scale industry, small business, small business, etc. there has been greater emphasis on disbursing credit.

(v) Development of Management: The commercial banks have undertaken management development programmes to meet the new techniques of banking system through the nationalisation of commercial banks. All the management structures have been changed of all commercial banks providing new techniques of management and better decision making through a process of delegation down the line.

(vi) New Scheme: Bank nationalization have provided As vital role in the implementation of Government’s various anti-poverty programmed such as Integrated Rural Development Programmed (IRDP). Besides it Regional imbalances were reduced comparatively through the nationalization of banks.