Advance Financial Accounting Unit 4 Investment Account, College and University Answer Bank for BA, B.com, B.sc, and Post Graduate Notes and Guide Available here, Advance Financial Accounting Unit 4 Investment Account to each Unit are provided in the list of UG-CBCS Central University & State University Syllabus so that you can easily browse through different College and University Guide and Notes here. Advance Financial Accounting Unit 4 Investment Account can be of great value to excel in the examination.

Advance Financial Accounting Unit 4 Investment Account

Advance Financial Accounting Unit 4 Investment Account Notes cover all the exercise questions in UGC Syllabus. Advance Financial Accounting Unit 4 Investment Account provided here ensures a smooth and easy understanding of all the concepts. Understand the concepts behind every Unit and score well in the board exams.

Investment Account

ADVANCE FINANCIAL ACCOUNTING

| VERY SHORT TYPES QUESTION & ANSWERS |

A. Multiple choice question and answers:

1. Investment account is a:

(a) Personal Account.

(b) Real Account.

(c) Nominal Account.

(d) None of these.

Ans: (b) Real Account.

2. Accounting for Investments is done as per:

(a) AS-12

(b) AS-13

(c) AS-14

(d) AS-15

Ans: (b) AS-13

3. Current investments are valued at:

(a) Cost.

(b) Fair value.

(c) Cost or fair value whichever is lower.

(d) None of these.

Ans: (c) Cost or fair value whichever is lower.

4. Long term or non-current investments are valued at:

(a) Cost.

(c) Cost or fair value whichever is lower.

(b) Fair value.

(d) None of these.

Ans: (a) Cost.

5. When investments are reclassified from current to long-term, transfers are made at:

(a) Cost.

(b) Fair value.

(c) Cost or fair value whichever is lower.

(d) None of these.

Ans: (c) Cost or fair value whichever is lower.

6. Cost of bonus shares is:

(a) Fair market value.

(b) Nil.

(c) Cost of original investment.

(d) None of these.

Ans: (b) Nil.

7. Investments hold for more than one year is known as:

(a) Trade investment.

(b) Marketable securities.

(c) Both a & b.

(d) None of the above.

Ans: (a) Trade investment.

8. Investment hold for less than or up to one year is called:

(a) Temporary Investments.

(b) Current investments.

(c) Marketable securities.

(d) All of the above.

Ans: (d) All of the above.

9. Which of the following investments is not true?

(a) Current investments are in the nature of current assets.

(b) Trade investments are in the nature of non-current assets.

(c) Cost of investment includes brokerage at the time of purchase.

(d) Cost of investment includes brokerage paid at the time of sale.

Ans: (d) Cost of investment includes brokerage paid at the time of sale.

10. Income-tax on interest, dividends and rent should be

(a) Debited to provision for taxation.

(b) Credited to provision for taxation.

(c) Deducted from interest, dividends and rents.

(d) None of these.

Ans: (c) Deducted from interest, dividends and rents.

A. State whether the following statements are True or False:

1. A current investment by its very nature is readily realisable.

Ans: True.

2. Cost of investment includes brokerage and acquisition fees.

Ans: True.

3. Bonus shares are issued only to the equity share holders.

Ans: True.

4. The carrying amount of non-current investment is cost or fair value whichever is lower.

Ans: False.

5. The carrying amount of current investment is cost.

Ans: False.

6. Brokerage on disposal of investment is excluded while calculating cost of investment.

Ans: True.

7. Current investments and non-current investments are disclosed distinctly in the financial statements.

Ans: True.

8. Market value or net realisable value provides an evidence of fair value.

Ans: True.

9. When the investment is a fixed asset, any profit or loss made on the sale is capital profit.

Ans: True.

10. Right shares are first offered to the existing shareholders of the company.

Ans: True.

C. Fill in the Blanks:

1. Investments hold for more than one year to earn continuous income or to control business is called ___________.

Ans: trade investments.

2. Investment held with a view to buy or sale is known as ___________.

Ans: temporary investments or current investments or marketable securities.

3. Current investments are valued at ___________ value whichever is lower and fixed investments are valued at cost.

Ans: cost or Fair.

4. Investment account is ___________.

Ans: real account.

5. ___________ held as stock-in-trade are not investments.

Ans : Assets.

6. ___________ is a capital receipt in case of a right issue.

Ans: Sale of right.

7. Brokerage is included in the cost of investment in case of purchase and brokerage are deducted with the cost of investment in case of ___________.

Ans: sale.

8. ___________ method is used to calculate cost of closing balance of investment.

Ans: FIFO and average cost.

9. Cost of Bonus shares is ___________.

Ans: nil.

10. Accounting for investments ___________.

Ans: AS-13

11. ___________ of investment is Ex-interest/dividend price.

Ans: Real price.

| SHORT & LONG TYPE QUESTIONS & ANSWERS |

1. What is cum-interest?

Ans: The word ‘cum’ is Latin word cum mean with cum-interest mean inclusive of interest when an investment is sold or purchased, the price quoted of the securities includes, both the cost of securities and the interest accused for the period from the last due date of interest to the date of sale.

2. What is ex-interest?

Ans: “Ex” is Latin word which means “without” interest means exclusive of interest, when investment is sold or purchased, the price quoted ex- interest of securities mean the buyer pays an amount which includes and only the cost price of the investment but also the interest accrued up to the date of purchase.

3. What is cum-dividend transaction?

Ans: The term cum-dividend in respect of equity shares means that the price of the shares includes the dividend of the shares which has not yet been declined and the purchase of such shares is given the right to receive from the company the dividend on the shares when it is declared.

4. What is an ex-dividend transaction?

Ans. The term ex-dividend in respect of equity shares means that the quoted price is meant for the cost of the share only and it does not include the dividend on the shares which has not yet been declared.

5. What is a Dividend?

Ans: A dividend is basically the distribution of a portion of a company’s earnings. It is probably the best benefits you can get from owning a prosperous business as a shareholder. Dividend payout amounts are. decided by the board of directors and can be issued in the form of cash payments, as shares of stock, or other property.

6. Write the Difference between Cum-dividend and Ex- Dividend.

Ans: Major differences between them are given as hereunder –

(i) Cum interest or dividend prices are inclusive of the interest or dividend accrued at the date of purchase, whereas in case of the ex- dividend, prices are excluding value of the dividend or interest.

(ii) The purchase price is higher than normal purchase price in case of Cum-dividend, whereas purchase price is the real price in case of ex- dividend.

(iii) Nothing is payable additional in case of Cum-Interest, whereas separate amount of the dividend or interest has to be paid in case of the ex-dividend or ex-interest.

7. What are the distinction between Cum-interest and Ex- interest?

Ans: The following are the points of distinction between cum-Interest and Ex-interest:

| Cum-interest | Ex-interest |

| (a) In case of cum-interest, the purchase price includes cost of investment and accrued interest up to the date of purchase. | (a) In case of Ex-Interest purchase, the buyer has to pay the accrued interest separately because it is not included the cost of investment only. |

| (b) In case of cum-interest, the buyer need not pay the accrued interest separately because it is already included is the price itself. | (b) In case of ex-interest purchase the buyer has to pay the accrued interest separately because it is not included in the quoted price. |

| (c) In case of cum-Interest the purchase price is more than the real price of securities. | (c) In case of ex interest the purchase price is the real price of the securities. |

| (d) In case of shares, the buyer is entitled to the dividend for the whole accounting period in case of cum-interest. | (d) The seller is entitled to dividend for the whole accounting period in case of ex-dividend purchase of shares. |

8. How to balance the investment Account? What are the special features of Investment Account?

Ans: When the whole of an investment has been sold, the difference between the two sides of an Investment Account will be profit or loss on the sale. Where only part of an investment has been sold during the year, the cost of the remaining investment will be brought down as a balance in the Investment Account and the difference between its two sides will be profit or loss on the investments sold. When the investment is a fixed asset, any profit or loss made on the sale thereof will be of a capital nature and should be treated accordingly.

Following are the features of Investment Account:

(a) An Investment Account contains three columns on either side. i.e “Nominal”, “Capital” and “Interest”, “Income” columns.

(b) When investments are purchased or sold not only the cost price or sale prices is recorded in the investment Account but also the nominal value of the investment and accrued interest dividend is also recorded.

(c) Profit on loss on the sale of investments is disclosed by the capital column and net income earned on investments is disclosed by the Income column.

(d) The Investment Account shows the nominal value and cost of investments is hand at the close of the year.

(e) Income or Interest column shows the interest accruing but not due on the date of closing of the account as accrued interest.

(f) The balance of Nominal column and capital column are carried forward but the balance of Income/Interest column is transferred to the profit and loss Account.

(g) A separate Investment Account is prepared for each type of investment containing the details there of at the top of the account.

9. What do you mean by investment account? What are the objectives of preparing an Investment Account?

Ans: The accounts of investments are kept in the same way as the accounts of any other asset. A separate investment account should be opened for each kind of security and on the head of the account particulars regarding the nature of the security, dates when interest or dividend is due, the date of redemption etc. should be stated. When the number of investments carried is large, a separate investment Ledger is employed for recording all investment accounts.

Objectives of preparing Investment Account are:

(i) Recording of detailed information: Primary objectives of preparing investment account is to get detailed information of the transactions relating to each type of security. It discloses the information such as nominal values, capital values, due dates of interest and amount of interest due and received etc.

(ii) Profit or Loss in dealings: Determination of the profit or loss made on the sale of each security is another objective of preparing Investment Account.

(ii) Determine the value of each security: Another objective of preparing investment account is to determine the value of each security at the end of the accounting period.

10. What is the process of closing of an Investment Account?

Ans: At the end of an accounting period. The balance in the “Nominal Column” shows the nominal value of the investment remaining in hand.

When the investments are considered as fixed assets, not meant for the purpose of dealing such investments are valued at cost price on the closing day of the period. However, if the investments are current assets which are meant for dealing. Such investment are valued at cost price or market price whichever is lower. The value of the investments are then entered in the capital column. On the credit side and is carried forward to the next period. The price may be mean the average cost, cost on FIFO basis or cost on LIFO basis. When the market price is lower than the cost price, it indicates a depreciation in the value of investments and is treated as a loss and is entered is the Capital column on the credit side. The loss is again transferred to the profit and loss account.

In case of fixed interest bearing investments such as, debentures, bonus etc. if the date of closing the account does not coincide with the dates on which the interest become due, the accrued interest from the date of last interest to the date of closing the account is credited in the income/interest column and is carried forward to the next period “Income Column” is then balanced and it represents profit and is to be transferred to the credit of the profit and loss account.

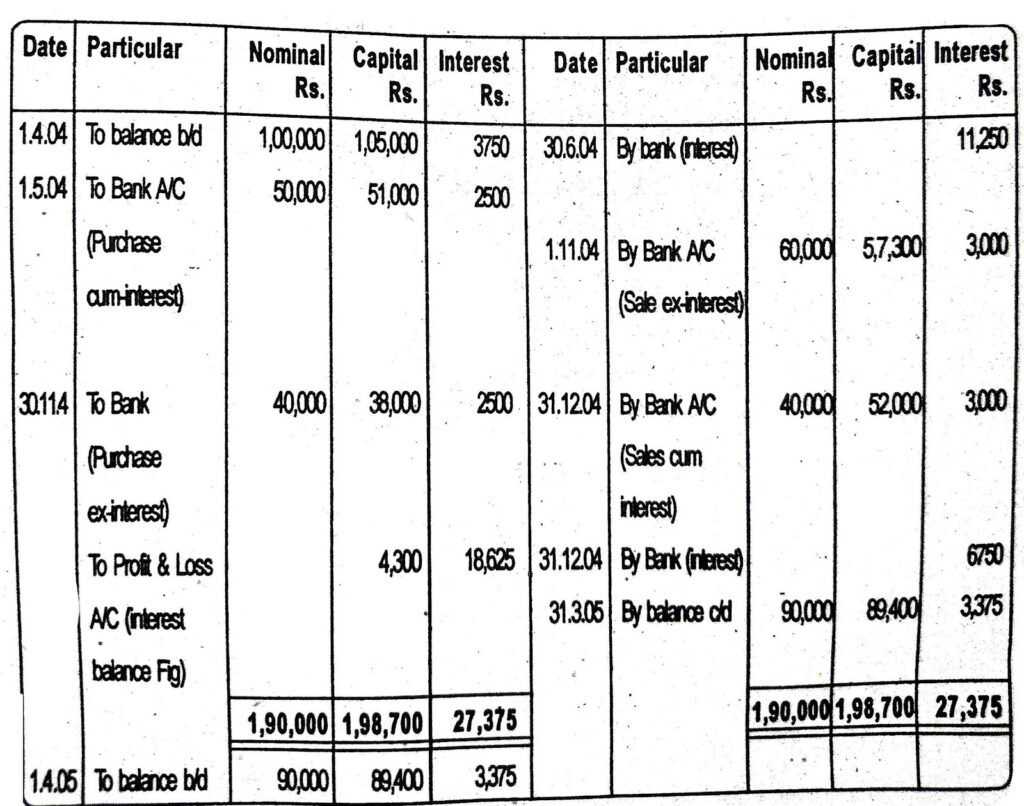

11. Jaipur investments Ltd. holds 1,000. 15% Debentures of Rs. 100 each in Udaipur Industries Ltd. as on 1st April 2004, at a cost of Rs. 1,05,000 being interest payable on 30th June and 31st December every year on 1st May, 2004, 500 Debentures are purchased cum-interest at Rs. 58,500. On 1st November 2004, 600 debentures are sold ex-interest at Rs. 57,300. On 30th November 2004, 400 debentures are purchased ex-interest at Rs. 38,400. On 31st December 2004, 400 Debentures are sold cum-interest for Rs. 55,000.

Prepare Investment Account holding on 31st March 2005 at cost (applying FIFO method)

Soln:

| 1 | 1.4.2004: Opening Balance: Nominal Value: 1,000 x Rs. 100 Cost: Rs. 1,05,000 Accrued interest: on Rs. 1,00,000 for 3 months. (1.1.04 to 31.3.04) = Rs. 3,750 (1,00,000 × 15/100 × 3/12) | = Rs. 1,00,000 |

| 2 | 1.5.2004: Purchase cum-interest Nominal value: 500xRs. 100 Cost: Less: Accrued interest include therein on Rs. 50,000 for 4 months (50,000 × 15/100 × 4/12) (1.1.04 to 30.4.04) Effective cost: | = Rs. 50,000 = Rs. 53,500 = Rs. 2,500 = Rs. 51,000 |

| 3 | 30.6.2004: Half yearly interest received: on Rs. 1,50,000 × 15/100 × 6/12 | = Rs. 11,250 |

| 4 | 1.11.2004: Sale ex-interest: Nominal value: 600 × Rs. 100 Sale Proceeds: Accrued interest receivable in addition on Rs. 60,000 for 4 months (60,000 × 15/100 × 4/12) Total amount received 57,300 + 3000 | = Rs. 60,300 = Rs. 57,300 = Rs. 3,000 = Rs. 60,000 |

| 5 | 30.11.2004: Purchase ex-interest: Nominal value: 400 × Rs. 100 Cost: Accrued interest payable in addition on Rs. 40,000 for 5 months (1.7.04 to 30.11.04) (40,000×15/100 x 5/12) | = Rs. 40,000 = Rs. 38,000 = Rs. 2,500 |

| 6 | 31.12.2004: Sales cum-interest: Nominal value: 400 x Rs. 100 = Rs. 40,000 Sale: proceeds Less Accrued interest include therein: on Rs. 40,000 for 6 months (as 40,000 × 15/100×6/12) (1.7.04 to 30.12.04) Effective sale proceeds: | = Rs. 55,000 = Rs. 3,000 52,000 |

| 7 | 31.12.2004: Half yearly interest received: (1,00,000 + 50,000 + 40,000-60,000-40,000) on Rs. 90,000 × 15/100 × 6/12 | = Rs. 6,750 |

| 8 | 31.3.2005: Accrued interest: On Rs. 90,000 for 3 months (90,000 × 15/100 × 3/12) (1.1.05 to 31.3.05) | = Rs. 3,375 |

| 9 | Calculation of profit and loss on sale: Net proceeds (57,300 + 52,000) Less: cost of Debentures sold(on FIFO basis) Profit on sale | = Rs. 1,09,300 = Rs. 1,05,000 = Rs. 4,300 |

Books of Jaipur investments Ltd.

Debentures (in Udaipur Industries Ltd.) Account Interest payable on 30th June and 31st December)

Dr.

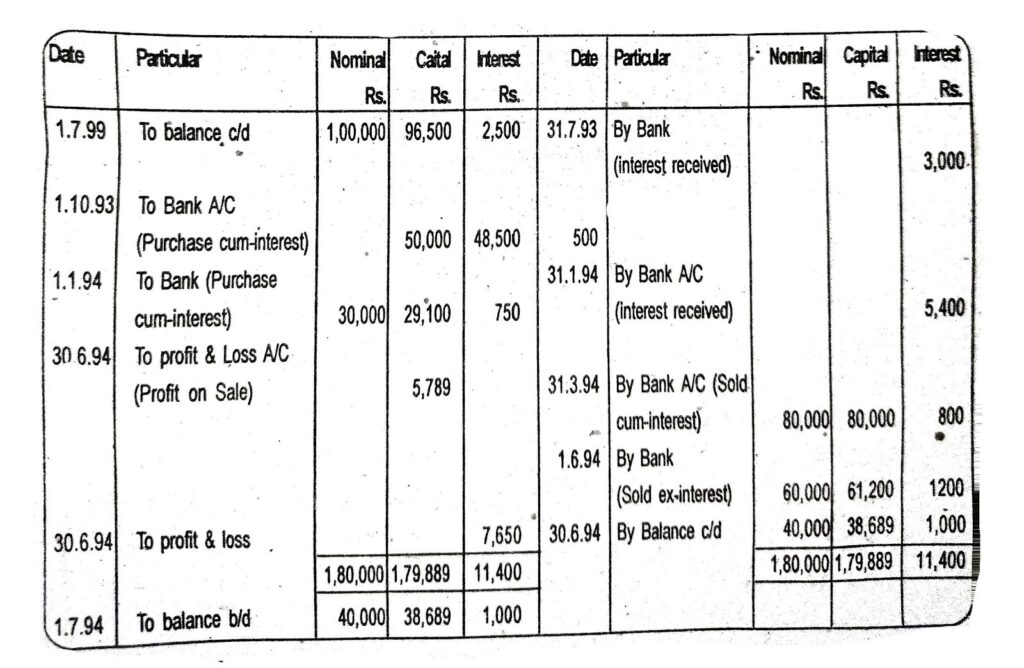

12. On July 1, 1993 Gauhati Investments Ltd. held Rs. 1,00,000 6% debentures of Industrial Development Bank which appeared in the books at Rs. 96,500/- Interest is payable on July 31 and January 31 on October 1, 1993 a further Rs. 50,000 debentures in Industrial Development Bank were bought at 98 cum-interest and on January 1, 1994 a further Rs. 30,000 debentures were bought at Rs. 97 ex-interest. On March 31, 1994 Rs. 80,000 debentures were sold at Rs. 101 cum-interest and June 1, Rs. 60,000 debentures were sold at Rs. 102/- ex-interest. Show the Investment Account for the period ending on June 30.1994.

Soln:

Working:

| 1 | 1.7.93: Opening balance: Nominal Value: Rs. 1,00,000 Cost: Rs. 96,500 Accrued interest for 5 months (1,00,000 × 6/100 × 5/12) (1.2.93 to 31.6.93) | = Rs. 2,500 |

| 2 | 31.7.93: Half yearly interest received: on Rs. 1,00,000 (1,00,000 × 6/100×6/12) | = Rs. 3,000 |

| 3 | 1.1.93: Purchase cum-interest: Nominal value Rs. 50,000 Cost: (50,000/100 × 8) Less: Accrued interest include there in on Rs. 50,000 for 2 months (1.8.93 to 1.10.93) Effective Cost: Total payment: = Rs. 49,000 | = Rs.49,000 = Rs. 500 |

| = Rs. 48,500 | ||

| 4 | 1.1.94: Purchase ex-interest: Nominal value: Rs. 30,000 Cost: (30,000/100×97) Accrued interest payable in addition on Rs. 30,000 for 5 months (30,000 × 6/100 × 5/12) Total payments = Rs. 29,100+Rs. 750 | = Rs. 29,100 = Rs. 750 |

| = Rs. 29,850 | ||

| 5 | 31.1.94: Half yearly interest received: On Rs. 1,80,000 [(1,00,000 + 50,000 + 30,000) 6/100 × 6/12] | = Rs. 5,400 |

| 6 | 31.03.94: Sales Cum-interest: Nominal Value: Rs. 80,000 Sale proceeds: (80,000/100 × 101) Less: Accrued interest include therein: on Rs. 80,000 for 2 months (1.2.94 upto 31.3.94) Effective sales proceeds: Total amount received = Rs. 80,800 | = Rs. 80,800 = Rs. 800 = Rs. 80,000 |

| 7 | 1.6.94: Sale ex-interest: Nominal Value: Rs. 60,000 Sale proceeds: (60,000/100 × 102) Accrued interest receivable on Rs. 60,000 for 4 months (60,000 × 6/100 × 4/12) Total amount received Rs. 61,200 + 1200 | = Rs. 61,200 = Rs. 1200 = Rs. 62,400 |

| 8 | 30.6.94: Accrued interest: on Rs. 40,000 for 5 months | = Rs. 1,000 |

| 9 | Calculation of profit and loss on sale: Net proceeds (80,000 + 61,200) Less: Cost (Assuming average cost) [(96,500 + 48,500 + 29,100)/(1,00,000 + 50,000 + 30,000) × (80,000 + 60,0000)} = 1,74,100/1,80,000 × 1,40,000 Profit on sale | = Rs. 1,41,200 |

| = Rs. 1,35,411 | ||

| = Rs. 5,789 |

Books of Gauhati Investment Ltd.

Investment Account

(Debenture of Industrial Development Bank) Interest payable on July 31 and January 31

Dr.

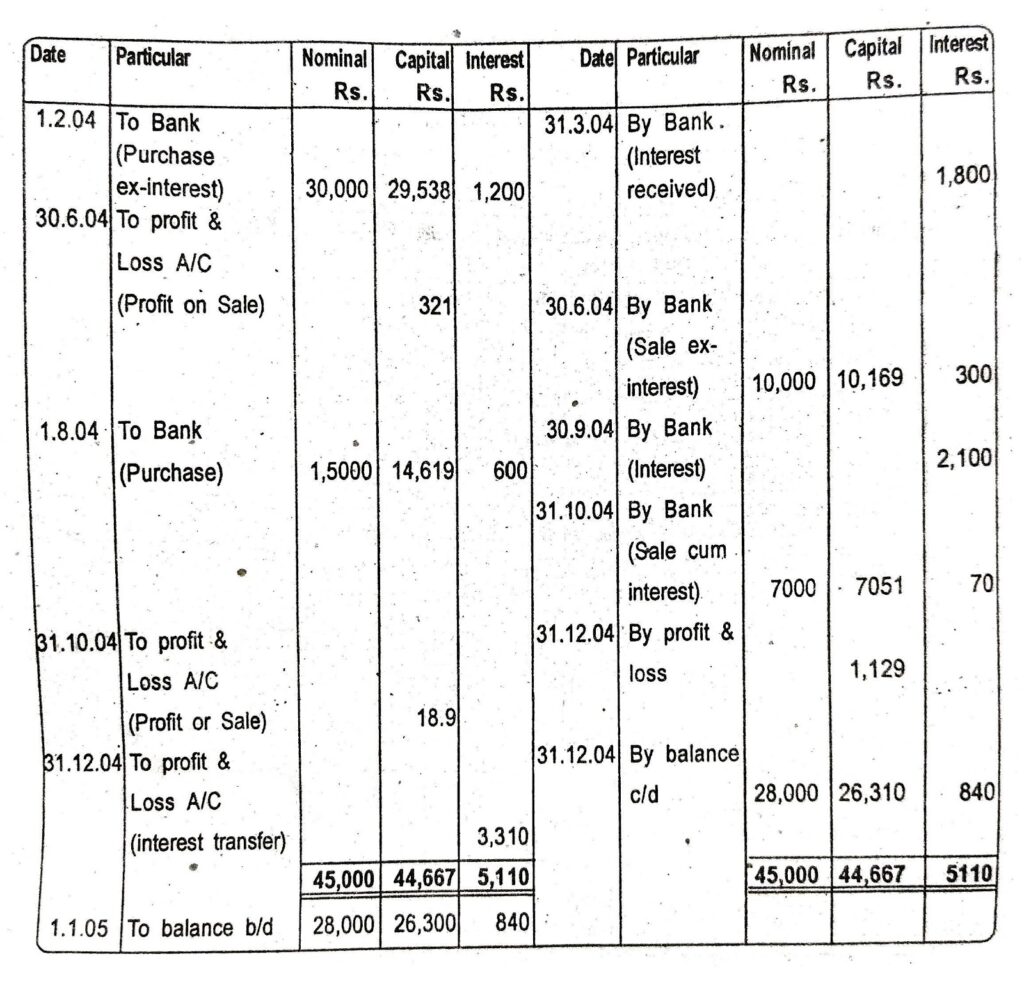

13. Sunrise Finance Ltd. purchased on 1st February 2004 Rs. 30,000. 12% Debentures of Hindustan Lever Ltd. at 98 ex- interest, plus brokerage 1/8% and expenses on purchase including stamp duty Rs. 100.

On 30th June 2004. Rs. 10,000 Debenture were sold at 102 ex- interest less brokerage at 1/8% and expensed on sale Rs. 20. On 1st August 2004 Rs. 15,000 Debentures were purchased 101 cum-interest plus brokerage at 1/8% and expenses on purchase Rs. 50.

On 31st October, 2004 Rs. 7000 Debentures were sold at 102 cum-interest less brokerage at 1/8% and expenses on sale Rs. 10. Market price of the debentures on 31st December 2004 was Rs. 94. Interest on Debenture is payable on 31st March and 30th September each year.

Accounts are closed on 31st December each year. Make out an investment account for the year ended 31st December 2004 in the books of Sunrise Finance Ltd. Calculating profit or Loss on sale of investment on the basis of average cost on the date of sale. Investments are valued at the end of the year at cost price or market price which ever is lower.

Soln:

| 1 | 1.2.04: Purchase ex-interest: Nominal value: Rs. 30,000 Cost: Rs. 30,000/100 × 98 Add: Brokerage (30,000 x 1/8%) Expenses: Effective Cost: Accrued interest payable in addition on Rs. 30,000 for 4 months (1.10.03 to 1.2.04) Total payment = Rs. 29,538 + Rs. 1200 | = Rs. 29,400 = Rs. 38 = Rs. 100 |

| = Rs. 29,538 | ||

| = Rs. 1,200 = Rs. 30,738 | ||

| 2 | 31.3.04: Half yearly interest received: on Rs. 30,000 = Rs. 1,800 | |

| 3 | 30.6.04 Sale ex-interest: Nominal Value Rs. 10,000 Sale proceeds: (10,000/100 x 102) Less. Brokerage (10,000 x 1/8%) = Rs.13. Expenses: = Rs. 20 Effective sales proceeds Accrued interest receivable in addition on Rs. 10,000 for 3 months (1.4.04 to 30.6.04) Total receipt: Rs. 10,167 + Rs. 300 | = Rs. 10,200 = Rs. 33 |

| = Rs. 10,167 = Rs. 300 | ||

| = Rs.10,467 | ||

| 4 | 1.8.04: Purchase cum-interest Nominal Value Rs. 15,000 Cost (15000/100×101) Add: Brokerage (15,000 x 1/8%) Expenses: Less: Accrued interest include therein on Rs. 15,000 for 4 months (1.4.04 to 1.8.04) Effective Cost Total payment Rs. 15,219 | = Rs.15,150 = Rs. 19= Rs. 50 = Rs. 15,219 = Rs. 600 = Rs.14,619 |

| 5 | 30.9.04 : Half yearly interest received: on Rs. 35,000 | = Rs. 2,100 |

| 6 | 31.10.04 : Sales cum-interest: Nominal value: as 7,000 Sales proceeds: (700/100 × 102) Less: Brokerage (7000 × 1/8%) Rs. 9 Expenses: = Rs. 10 Less: Accrued interest include therein on Rs. 7,000 for 1 months. Effective sale proceeds: Total amount received = Rs. 7,121 | = Rs. 7,140 = Rs. 19 |

| = Rs. 7,121 | ||

| = Rs. 70 | ||

| = Rs. 7,051 | ||

| 7 | 31.12.04: Accrued interest: On Rs. 28,000 for 3 months | = Rs. 840 |

| 8 | Calculation of profit/Loss on sale and value of closing balance on the basis of average cost: |

| Date | Transactions | Nominal | Cost | Sale price | Profit/Lose |

| 1.2.04 30.6.04 Balance | Purchase Less sale | 30,000 10,000 | 29,538 9,846 | 10,167 | (+) 321 |

| 20,000 | 196,92 | ||||

| 1.8.04 31.10.04 Closingbalance | Purchase Less sale | 15,000 35,000 7000 | 14,619 34,311 6862 | 7,051 | (+) 189 |

28,000 | 27,449 |

Notes:

| (a) Average cost | = 29,538/30,000 × 10,000 | = Rs. 9,846 |

| (b) Average cost | = 34,311/35,000 × 7000 | = Rs. 6,862 |

The market value of Rs. 28,000 Debenture on 31st December Rs. (28,000/100 × 94) or Rs. 36,320

Market price bring lower then the cost price Debentures will be carried forward at Market price. Depreciation in value (Rs. 27449-Rs. 26,320 or Rs. 1,129 will be written off to profit & Loss A/C.

Books of Sunrise Ltd.

Investment Account

(12% Debentures of Hindustan Ltd.)

Interest payable on 31st March and 30th September

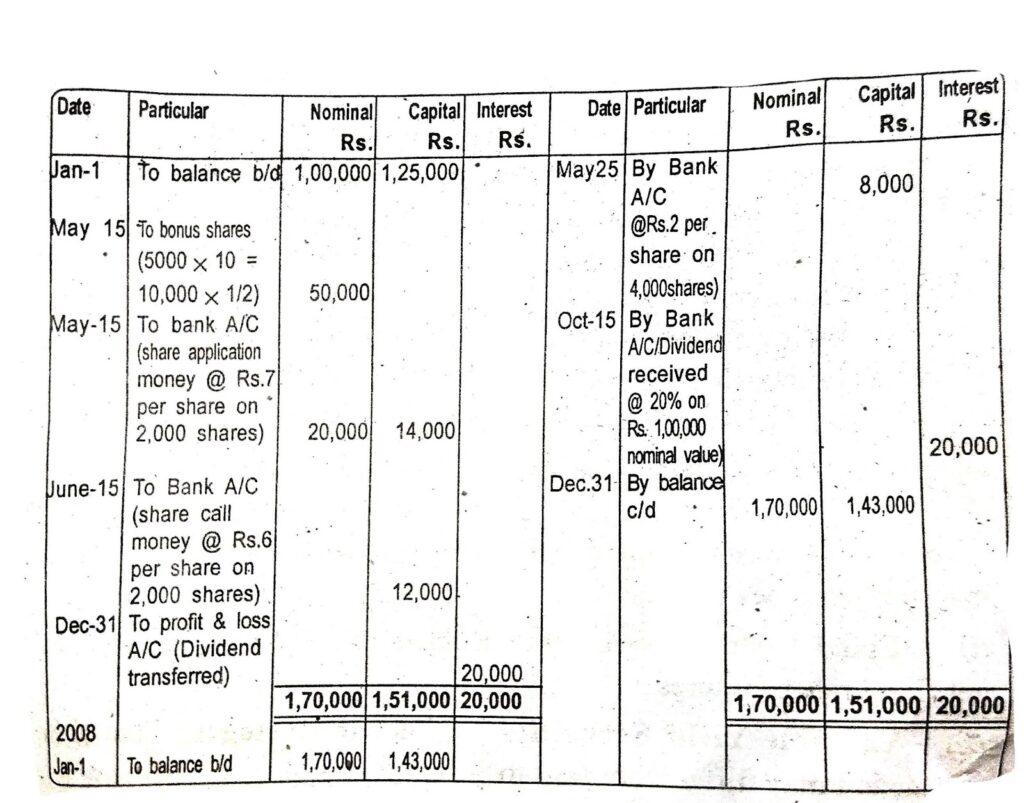

14. On 1.1.04 × Ltd.had 10,000 equity shares of Rs. 10 each in Agoha Ltd. Purchased for Rs.1,25,000. The Company unlike investment Companies does not make any apportionment of dividends (receive or receivable) in between capital and revenue. On 15.5.04, the Alpha Ltd. made a bonus issue of full paid share for every 25 c/d on 15.5.04. In addition, on the same day right shares were issued at 3 for 5 held on that date at a premium of Rs. 3, Rs. 7 to be paid on application and the balance in one call after a month. These shares are not to reach for dividend for the year ending 30th June 04. 2000 right shares were taken up by × Ltd. balance right being sold at Rs. 2 each on 25.5.04. On 15.10.04 the company declared a dividend of 20% for the year ending 30th June, 2004. Make out the Investment Account in the book of X Ltd. ignore income tax.

Soln:

Books of X Ltd.

Investment Account (Excluding Income-Tax)

Nos. of Right shares 10,000×3/5 = 6,000 shares

Less Number of shares taken up = 2,000

∴ Right sold @ 2 each = 4,000 shares

∴ Sale price 4,000 × 2 = 8,000

Note:

(a) For bonus shares nominal value only will be entered in ten nominal column i.e. Rs. 50,000 (5000 × Rs. 10).

Nothing will be entered in the capital column as nothing is paid against these shares.

(b) For 2,000 right shares the nominal value of Rs. 20,000 (2000 × Rs. 10) is entered in the Nominal Column and amount paid on application @ Rs. 7 and on allotment @ Rs. 6 per share are entered in the Capital Column in their respective dates. No dividend accrued on these shares for the year ending on 30th June, 2004; hence nothing is to be recorded in the Dividend Column.

15. What is the meaning of Investment? Write the purpose of maintaining an investment ledger.

Ans: Investment means either buying or creating an asset with the future expectation of capital appreciation, dividends (profit), rents, interest earnings, or some combination of these returns. However, normally, investment inherent with some form of risk, such as investment in equities, property, and even fixed interest securities, among other things, are the subject to inflation risk.

Further, among all these, securities are held as long term investment to earn income. It is said to be fixed assets, but where objective of an organisation is to sell and buy securities in short term fund to utilise its surplus fund, would come under the category of current assets. There may be two types of securities –

(i) Fixed Interest Securities: Holders of fixed interest securities get fixed rate of interest.

(ii) Variable Yield Securities: Under this category, return on investment may differ from year to year.

Purpose of maintaining an investment ledger is as follows:

(i) It helps in keeping a record of each investment separately.

(ii) It helps to ascertain the value of securities at the end of the account period.

(iii) It is helpful in collection of interest and dividend as and when they become due.

(iv) It is helpful in ascertaining the amount of accrued income at the end of the accounting period.

(v) It facilitates the determination of the profit or loss on sale of any security.

16. What is an Investment Account? Explain its features also.

Ans: An investment account holds cash and the investments (stocks, bonds, ETFs, Mutual Funds, etc.) that you buy and sell to realise your financial goals. Dealers and their representative registered investment advisors administer trading accounts for individual investors. An investment account is a current account linked to a securities account. It is used to transfer money in transactions to securities and deposit services. An investment account is particularly intended for transactions in funds, stocks, bonds, and ETFs.

Features of Investment accounts:

(i) Columnar Form: An investment account contains three amount columns on either side-Nominal, Capital and Income columns.

(ii) Simultaneous recording in three columns: When investments are purchased or sold, not only the cost price or sale price is recorded in the capital column but also nominal value of the investment and accrued interest are also recorded in the nominal and income columns respectively.

(iii) Closing balance: Closing balance of investment account at the end of the accounting period shows the nominal value, capital value and accrued interest on nominal value in the respective columns.

(iv) Valuation as current Assets: At the time of annual closing, securities in hand are valued treating them as current assets and are valud at cost price or net realisable market price whichever is lower.

(v) Determination of Profit or Loss on sale: Profit or loss on sale of investment is ascertained by balancing the capital column. Profit or loss on sale of investment is transferred to profit and loss account. The net income earned from the investment is ascertained by balancing the income columns and is transferred to the profit and loss Account.

17. Treatment of Bonus shares, Rights Shares and Brokerage in investment accounts.

Ans: (i) Bonus Shares: When successful companies issue bonus shares to capitalise their reserves, the shareholders are not required to pay any amount for such shares. The number of shares will be entered in the number column and nothing will be added in the amount of principal or capital column. When bonus shares are sold, the profit on such shares is calculated by deducting average cost of shares sold from sale price of bonus shares. Valuation of investment in shares should be made at market value or average cost price of shares, whichever is lower.

(ii) Right shares: If shares are first offered to the existing shareholders as a matter of their right, such shares are called right shares. Such shares may be purchased by the shareholder or the right may be renunciated in favour of a third party for a consideration. If the shares are purchased, the number of shares & amount paid will be entered in the number & principal columns actively. If the shares are not subscribed for but are sold in the market, the amount received will be entered only in the profit and loss account.

(iii) Brokers and Brokerage: Brokers are primarily Commission agents and act as an intermediary between buyer & seller of securities. They do not purchase & sell securities on their behalf. They bring together buyers & sellers and help them make a deal. They charge commission from both parties. Such a commission is called brokerage. Brokerage is added with the cost of investments and deducted with sale proceeds of investments.

18. What is the purpose of maintaining an investment ledger?

Ans: Purpose of maintaining an investment ledger is as follows:

(i) It helps in keeping a record of each investment separately.

(ii) It helps to ascertain the value of securities at the end of the account period.

(iii) It is helpful in collection of interest and dividend as and when they become due.

(iv) It is helpful in ascertaining the amount of accrued income at the end of the accounting period.

(v) It facilitates the determination of the profit or loss on sale of any security.

19. How to Prepare an Investment Account?

Ans: Preparation of Investments Account: Concerns holding a large number of investments may find it more convenient to use a separate ledger called an Investment Ledger, for keeping the accounts of all their investments. Such a ledger is kept on the columnar system and is ruled differently from an ordinary ledger. As the issuing authority of a security pays interest to the holder at a certain rate calculated on its face value, it is desirable that the face value (also known as the nominal value) as well as the interest or dividend received should appear side by side with the capital invested in it. Therefore, the investment Ledger is provided with three columns on either side headed ‘Nominal Value’, ‘Interest or Dividend’ and ‘Capital or Principal’. The name of each investment is written at the tip of the account followed by the rate of interest or dividend and the dates on when it is payable; when an investment is purchased “cum- dividend”, “ex-dividend” its cost is analysed into the nominal price and the dividend or interest accrued and as entry is made on the credit side of the Cash Book, from where it is posted to the respective columns on the debit side of the particular Investment Account in the Investment Ledger. When the whole or part of the investment is sold, the price received, similarly split up into the nominal price and the dividend or interest accrued, is entered on the debit side of the Cash Book, from where it is posted to the respective columns on the credit side of the particular Investment Account in the Investment Ledger. Expenses by way of brokerage, stamps etc., will be debited to the capital account. When dividend or interest accrued on an investment is received, it is first entered on the debit side of the Book and then posted to the credit side of the particular Investment count in the ‘Dividend or Interest’ column in the investment Ledger. At the close of the financial year, the dividend or interest accrued on investments, but not received, is brought into account by crediting ‘Dividend or Interest’ columns of the different Investment accounts in the Investment Ledger and bringing down such balances as an asset after the accounts have been balanced.

The first column is of Nominal Value and in it on the credit side is entered the nominal value of investments on hand and the totals on both sides will then agree. The second column is of Interest or Dividend and it will always show a credit balance representing interest or dividend on investments for the period and it will be carried to Profit and Loss Account. The third column is for Capital or Principal. In this column against the closing balance will be entered the value of securities is hand and the difference of the two sides will show profit or loss on the sale of investments during the period. Value of securities in hand is the lower of cost and fair values as per Para 14 of AS-13.

When the whole of an investment has been sold, the difference between the two sides of an Investment Account will be profit or loss on the sale. Where only part of an investment has been sold during the year, the cost of the remaining investment will be brought down as a balance in the Investment Account and the difference between its two sides will be profit or loss on the investments sold. When the investment is a fixed asset, any profit or loss made on the sale thereof will be of a capital nature and should be treated accordingly.

20. What are the four basic types of investment accounts?

Ans: There are four basic types of investment accounts:

(i) Individual Brokerage Account (or Joint Brokerage Account): An individual brokerage account is the most basic and flexible type of investment account. In the simplest terms, a brokerage account allows you to buy and sell investment vehicles through a licensed broker (like Charles Schwab) with very little restrictions. Opening an individual brokerage account has become very simple thanks to the rise of online brokers. The basic process is as follows:

(a) Open an online brokerage account (i.e. through Betterment or Charles Schwab).

(b) Deposit money into the account – there are a couple ways to do this, but the easiest is to link your checking account and electronically transfer money. You can usually mail a check as well if you prefer.

(c) Start Investing.

(ii) IRA (Individual Retirement Account): Roth or Traditional: An account designed to help you save for retirement is an IRA (Individual Retirement Account) – exactly what it sounds like. There are significant tax benefits to IRAs that help you keep more of your money, but also some rules on when you can withdraw your money (and penalties if you do not follow these rules). There are several types of IRAS, but the two most common are the Roth IRA and Traditional IRA. Tax-advantaged accounts come with rules you need to follow. Here a couple key ones to keep in mind with IRAs:

(a) Max Contributions: In 2021, the maximum amount of money you can contribute to an IRA is $6,000 ($7,000 if you are 50+ using catch up contributions) annually. This applies to both Roth and Traditional IRAs (so, you cannot contribute $6,000 each to both a Roth and Traditional IRA).

(b) Withdrawal Rules: Money withdrawn before age 59.5 has a 10% additional tax (note: for Roth IRAs this only applies to capital gains, not your original contribution).

(c) Income Limits (Roth): Your ability to contribute to a Roth IRA reduces (and eventually goes down to $0) if your modified adjusted gross income (MAGI) is above certain levels. If you are single or filing separately from your spouse the limit is $125,000. If you are married filing jointly the limit is $198,000.

(d) Income Limits (Traditional): For a traditional IRA, the limits depend on if you qualify for a retirement plan through work. If you do not qualify for a corporate-sponsored plan, then there are no income limits.

(iii) 401k (and other Corporate Sponsored Accounts): A 401k is a corporate-sponsored account provided by your employer. As mentioned above, a 401k is similar to a Traditional IRA – it offers a tax break on your income now and you are taxed on your money later. With 401ks, you designate a percent of your income (paycheck) that you want to contribute and it is automatically deducted and invested for you (based on your pre- selected investment vehicles). The largest benefit of a 401k is employer match programs (as applicable). In short, some companies contributes a certain percentage of your income to your 401k in addition to your contributions (as long as you meet certain contribution thresholds). The most common example is companies matching 50% of the first 6% you contribute. Here are a couple of examples to help illustrate:

Example 1: You contribute 3%, employer contributes 1.5%. Total = 4.5%.

Example 2: You contribute 6%, employer contributes 3%. Total = 9%.

Example 3: You contribute 9%, employer contributes 3%. Total = 12%.

There are a few rules to keep in mind with 401ks:

(a) Max Contributions: The max contribution for any individual is $19,500 annually, while the max contribution for the individual + employer is $58,000 annually.

(b) Withdrawal Rules: Money withdrawn before age 59.5 has a 10% additional tax.

(c) Mandatory Withdrawals: Similar to Traditional IRAs, you must start withdrawing from the plan starting at age 72 (if you were born after June 30, 1949)

(iv) 529 College Savings Account: Last on the list of types of investment accounts is the 529 Savings Account (specifically, the Education Savings Plan). This account is designed to help save for a beneficiary’s higher education (i.e., college) and includes generous tax benefits (benefits vary slightly by state).

21. Concept of Jobbers and Brokers?

Ans: Jobbers: Jobbers are security merchants dealing in shares, debentures as independent operators. They buy & sell securities on their own behalf and try to earn through price changes. They directly deal with brokers who make transactions on the behalf of public. They generally quote two price, one – for purchase and other for sell. The difference between the two prices constitutes his remuneration. This system enables specialisation in the dealings and each jobber specialises is certain group of securities. It also ensures smooth and prompt execution of transactions. The double quotation of a jobber assures fair-trading to investors.

Brokers: Brokers are primarily Commission agents and act as an intermediary between buyer & seller of securities. They do not purchase & sell securities on their behalf. They bring together buyers & seller and help them making a deal. They charges commission from both parties. They are experts in estimating prices and advise their clients in getting gain. They get orders from public and execute the orders through jobbers.

22. How Cum-Dividend Works? Write an Example of Cum-Dividend.

Ans: Before the announcement of year-end results for companies, dates are set out for closing the register for dividend payments and scrips. These dates will determine the qualification for dividends and scrips. A scrip is a document acknowledging a debt. Companies short on cash often pay scrip dividends instead of cash dividends. Cum dividend is the status of a security when a company is preparing to pay out a dividend at a later date. The seller of a stock cum dividend is selling the right to the share and the right to the next dividend distribution. This situation often results from the timing of the sale rather than the preference of the seller.

In order to buy a share cum dividend, the buyer must complete the purchase before a certain point in the dividend period, called the record date. Often, companies will require the sale to be completed two business days before the end of the period. However, some corporations will push the deadline to the last day of the period. If the buyer completes the recording of the transaction in time, they will receive the eventual distribution. If the buyer misses the deadline, then the share is sold ex-dividend, or without the right to the next distribution. The dates are set based on the declaration date and recording date chosen by the company that issues the stock.

There is no specific schedule for the release of dividends, and the payment dates can vary from company to company. Some companies offer quarterly dividends, while others may pay dividends only once or twice a year. While it is not typical, some companies pay dividends monthly.

Example of Cum-Dividend:

Let’s say an investor owns 100 shares of e-commerce firm Priced to Sell, and the company’s board of directors has declared a quarterly dividend of $0.10 per share. The ex-dividend date is ten days away. The investor is considering selling their shares to finance another purchase. If they sell cum dividend, the buyer would receive the 100 shares at the current price and would be entitled to the $10 in dividend payouts.

Suppose the seller holds off on selling during the cum dividend period, waiting to see if other investments pan out. Those investments don’t end up panning out, and the seller is forced to sell the 100 shares of Priced to Sell. However, the cum dividend date has passed, and the shares are ex- dividend. To reflect the loss of the dividend, the market price of the shares will be $10 lower, all other things being equal. While the buyer won’t receive that quarter’s distribution, they will be entitled to future distributions if they continue to hold the shares.

23. Write an Example of Ex-Dividend.

Ans: For example, Walmart (WMT) paid $0.53 per share dividend on Jan. 2, 2020. The payment went to shareholders who had purchased Walmart stock prior to the ex-date of Dec. 5, 2019. The company had previously declared the dividend on Feb. 19, 2019, and the record date was set as Dec. 6, 2019.2 Only shareholders who had purchased Walmart stock prior to the ex-date were entitled to the cash payment.

24. What is a brokerage account? State its features? Give an Example of a Brokerage Account.

Ans: A brokerage account is an investment account that allows you to buy and sell a variety of investments, such as stocks, bonds, mutual funds, and ETFs. Whether you’re setting aside money for the future or saving up for a big purchase, you can use your funds whenever and however you want.

Features are:

(i) A brokerage account is a type of financial account that allows a person to trade investment products.

(ii) Many different kinds of investment products can be held in an investment account, including stocks, bonds, mutual funds, and much more.

(iii) Brokerage accounts offer fewer tax shelters than retirement accounts, but there are also fewer restrictions on when a trader can contribute or withdraw money,

Example of a Brokerage Account:

A brokerage account is a type of taxable investment account that can be opened with a brokerage firm. The account holder can order trades, such as buying or selling stocks, and those orders are executed by the brokerage firm. Alternate name: Taxable account. Brokerage accounts are the more basic alternative to retirement investment accounts, like 401(k) plans and Roth IRAs. Unlike retirement accounts, which have special rules and tax advantages, brokerage accounts have very few restrictions, and any gains or losses (including dividends) are reflected on your taxes for that year.

25. How Does a Brokerage Account Work?

Ans: Brokerage accounts are easy to open. The process is similar to opening a checking account with a bank. Someone who wants a brokerage account files an application with a brokerage firm. The application will ask for basic personal information, such as your name, address, and Social Security number. Once your application is approved, you deposit money into the account by writing a check, wiring money, or transferring money from your checking or savings account. After your deposited funds settle, you can use the money to buy different types of investment securities. There is no limit to the number of non-retirement brokerage accounts you are allowed to have. You can have as many or few brokerage accounts as you want, unless an institution chooses not to allow you to open a brokerage account. You can have multiple brokerage accounts at the same institution, segregating assets by investing strategy. You can have multiple brokerage accounts at different institutions, diversifying your relationships and exposure.

As you shop for a brokerage, take note of the financial strength of your broker and the extent of its SIPC coverage, which is the insurance that compensates investors if their stock brokerage firm goes bankrupt. Different types of assets have different levels of coverage, and some-like commodities-have no coverage at all.

26. Difference between Jobber and Broker.

Ans:

| Basis | Jobber | Broker |

| Meaning | Jobber is a dealer who deals in buying and selling of securities. | Broker is an agent who deals in buying and selling of securities on behalf of his client. |

| Specialisation | Jobber is a specialist mercantile agent. | Broker is a general mercantile agent. |

| Nature of trading | A jobber carries out trading activities only with the broker. | A broker carries out trading activities with the jobber on behalf of his investors. |

| Restrictions on dealings | A jobber is prohibited from buying or selling securities directly in the stock exchange. Also he cannot directly deal with the investors. | A broker Acts as a link between the jobber and the investors. He trades i.e. buyers and sells securities on behalf of its investors. |

| Agent | Jobber is an independent dealer or a merchant willing to buy and sell securities. | Broker is merely an agent to buy or sell on behalf of his clients. |

| Form of consideration | A jobber gets consideration in the form of profit. | A broker gets consideration of commission or brokerage. |

| Price Quotations | Jobbers quote two prices to the broker, one for buying and one for selling. Sale quotation is higher than the purchase quotations. | Broker has to negotiate terms and conditions of sale or purchase and safeguard his client’s interest. |

27. Explain the Types of Brokerage Accounts.

Ans: While brokerage accounts have fewer special rules than retirement accounts, there are a few different kinds of brokerage accounts. When you’re shopping for a brokerage account, pay attention to whether the account falls into one of the following categories.

(i) Discount Brokerage: A discount brokerage account, or discount broker, is the most common form of brokerage account for casual investors who are just starting out. It may be an online-only brokerage, or there may be a few branch offices around the country. Everything is pretty much do-it-yourself, and you have to execute your own trades. As a result, you save on fees.

(ii) Full-Service Account: A full-service brokerage account is a brokerage account that pairs you with a dedicated broker who knows you, your family, and your financial situation. You can pick up the phone and speak to them, or walk into their office and regularly have meetings to discuss your portfolio. In exchange for that personalised service, you’ll pay higher fees. These fees may be bundled into your commission fees, or they may be charged to your account in some other form.

(iii) Cash Brokerage Account: A cash brokerage account is one that requires you to deposit cash before you can start trading. In other words, the brokerage won’t lend you any money, and you can’t spend what you don’t have. If you want to buy a stock worth $20, you have to deposit at least $20 into your account and use those funds to complete the trade. This limits traders to basic trades-they can’t short a stock, for instance.

(iv) Margin Account: A margin account, as opposed to a cash account, allows you to borrow money to make trades. The broker essentially doubles as a lender, giving you what amounts to low-interest loans for the specific purpose of making trades. These loans allow for more advanced trades, such as shorting. As with cash accounts, margin accounts can be either discount or full-service brokerage accounts. While borrowing money to make trades enhances your potential gains, it also adds to your risk. Only experienced traders should consider using a margin account.

28. Define Contango and Backwardation.

Ans: Contango and backwardation are two technical terms used in the futures market. These terms are used to describe the position of futures price in comparison with the spot price.

(i) Contango: Futures markets, by definition, are predicated on the future price of a commodity. Analysing where the future price of a commodity is heading is what futures trading is all about. Because futures contracts are available for different months throughout the year, the price of the contracts changes from month to month. In a normal market, futures price would be greater than the spot price due to the effect of cost of carry. This situation is generally referred to as a ‘Contango’ market. The market is also in Contango when the price of the front month is higher than the spot market, and also when late delivery months are higher than near delivery months.

(ii) Backwardation: Backwardation is just the opposite of Contango. In some special situations, the futures prices may be decided by factors other than cost of carry. In such cases, futures may trade below the spot. Such situations, where the spot price minus futures price (basis) is a positive figure, is generally termed as ‘backwardation’ market. It occurs normally in an “inverted futures curve” environment. Essentially, on the maturity date, the futures price will converge higher to the spot rate. This means that a commodity is worth more right now than it is in the future.

29. Why Should an Investor Understand Accounting?

Ans: Investors use financial statements to obtain valuable information used in the valuation and credit analysis of companies. This makes it important to understand how business accounting is done and which principles guide financial statement preparation. Knowledge of accounting helps investors determine an assets’ value, understand a company’s financing sources, calculate profitability, and estimate risks embedded in a company’s balance sheet.

Understanding a company’s classification of its assets, liabilities, and valuation methods in financial accounting is paramount in investment and credit analysis. For example, according to U.S. Generally Accepted Accounting Principles (GAAP), the asset value is, for the most part, based on historical cost and does not reflect its market value. Therefore, obsolete equipment with positive book value may be worthless if the company attempts to sell it. Also, the value for a certain class of assets is based on management’s judgement and may not reflect its true economic value.

For instance, if the value of the company’s goodwill is based on unrealistic assumptions, the management may have to take a large earnings charge in the future. Investors who have a strong knowledge of business accounting can be ahead of the curve by identifying such problems early on.

30. What is Accounting for Investments? Describe the procedure of accounting for investments.

Ans: The accounting for investments occurs when funds are paid for an investment instrument. The exact type of accounting depends on the intent of the investor and the proportional size of the investment.

Depending on these factors, the following types of accounting may apply:

(i) Held to Maturity Investment: If the investor intends to hold an investment to its maturity date (which effectively limits this accounting method to debt instruments) and has the ability to do so, the investment is classified as held to maturity. This investment is initially recorded at cost, with amortisation adjustments thereafter to reflect any premium or discount at which it was purchased. The investment may also be written down to reflect any permanent impairments. There is no ongoing adjustment to market value for this type of investment. This approach cannot be applied to equity instruments, since they have no maturity date.

(ii) Trading Security: If the investor intends to sell its investment in the short-term for a profit, the investment is classified as a trading security. This investment is initially recorded at cost. At the end of each subsequent accounting period, adjust the recorded investment to its fair value as of the end of the period. Any unrealized holding gains and losses are to be recorded in operating income. This investment can be either a debt or equity instrument.

(iii) Available for Sale: An available for sale investment cannot be categorised as a held to maturity or trading security. This investment is initially recorded at cost. At the end of each subsequent accounting period, adjust the recorded investment to its fair value as of the end of the period. Any unrealized holding gains and losses are to be recorded in other comprehensive income until they have been sold.

(iv) Equity Method: If the investor has significant operating or financial control over the investee (generally considered to be at least a 20% interest), the equity method should be used. This investment is initially recorded at cost. In subsequent periods, the investor recognizes its share of the profits and losses of the investee, after intra-entity profits and losses have been deducted. Also, if the investee issues dividends to the investor, the dividends are deducted from the investor’s investment in the investee.

Following is the procedure of accounting for investments:

(i) Opening balance of securities: An investment account is opened with the balance of security held on the last day of the previous year, if there be any, by writing the same on the debit side as balance b/d. the nominal value, capital value and accrued interest thereon are recorded in the respective amount columns.

(ii) Purchase of investment: When investment is purchased, it is recorded on the debit side of the investment account as under:

(a) nominal value in the nominal column.

(b) actual cost in the capital column including brokerage and expenses. and

(c) accrued interest and interest paid (for the expired period) in the interest column.

However, such recording of investment transactions depends on whether the transaction is cum-interest or ex-interest.

(iii) Receipt of interest on investment: Interest on investment received on due dates will be recorded on the credit side in the interest column.

(iv) Sale of Investment: When investment is sold, it is recorded on the credit side of the investment account as under:”

(a) nominal value in the nominal column.

(b) actual cost in the capital column.

However, such recording of investment transaction depends on whether the transaction is cum-interest or ex-interest.

(v) Valuation of closing Investment: At the end of the year, closing investment is to be valued at cost price if it is treated as a fixed asset. If the investment is treated as a current asset, it is valued at cost price (either at LIFO, FIFO or Average cost) or market price whichever is lower.

(vi) Accounting of accrued interest: Interest accrued on the closing investment from the date of last due date of interest up to the date of closing of accounts is also calculated and recorded in the interest column on the credit side of the investment account as balance c/d. The interest will be calculated at the given rate on the nominal value of investment.

(vii) Ascertainment of Profit/Loss on sale of investment: When the whole of the investment is sold, the difference between the two sides of the investment account will represent profit/loss on sale of investment.

Where only a part of the investment is sold during the year, the selling price net of interest will be compared with the cost of deb 5210 entures. The difference between the two will be the profit/loss on sale of investments which will be transferred to the profit and Loss Account.

The value of the remaining investment will be brought down as a balance in the Capital Column (credit side) of the investment account as Balance c/d as per the valuation principle. The difference, if any, between the two capital columns will represent the loss on revaluation of investments which will be transferred to the Profit and Loss Account.

31. Difference between Contango and Backwardation.

Ans:

| Basis | Contango | Backwardation |

| Definition | Contango refers to the situation where the Future prices of stock are higher than the current spot price. | It refers to the market situation where the Future prices are lower than the current spot prices for a particular commodity. |

| Future Curve | If a commodity market is in Contango, the future price curve is considered to be in an “upward-sloping” or normal market. | If a commodity market is in Backwardation, the future price curve is considered to be in an “downward-sloping” or inverted market. |

| Price Difference | Future Price is more than the Spot Price. | Future Price is less than the Spot Price. |

| Most Happen in Case of | Contango mostly happens in the Commodity market. | Backwardation commonly happens in Oil market. |

| Driving factors | Contango is a supply driven market situation. | Backwardation is a demand driven market situation. |

32. Short note on Rebate on Bills Discounted.

Ans: A rebate on bills discounted is a reduction in the price of a good or service that has been paid for in advance. Typically, this type of rebate is offered to customers who have paid their bills in full and on time. The discount may be a percentage of the total amount owed, or it may be a fixed amount. Rebates on discounted bills can be a powerful incentive to encourage customers to pay their bills on time and can help businesses improve their cash flow. In the event that the maturity dates of some bills fall after the date of preparation of final accounts, the discount credited to those bills cannot be treated as earned in the current year. Therefore, the discount for the unexpired period is debited to the discount account to cancel the credit previously given, then credited to the Rebate on Bills Discounted Account’ or Unexpired Discount Account.

33. Cum-interest and Ex-interest price.

Ans: The term ‘Cum’ and ‘Ex’ are Latin words. ‘Cum’ means with and ‘Ex’ means without. The term ‘Cum-interest’ and ‘Ex-interest’ relate to debentures and bonds. Cum-interest can be expanded as inclusive of interest and Ex-interest can be expanded as exclusive of interest. Cum interest is the amount of interest accrued in the duration between the last interest date and the settlement date or transaction date. The cum-interest price includes not only the cost but also includes the interest accrued up to the date of purchase, and when interest becomes due it would be the right of the buyer to claim interest. Conversely, the quotation, Ex-interest, covers only the cost of the debentures and the buyer is liable to pay additional amount as interest accrued up to the date of purchase of debentures.

34. Write a short note on Liability for Bills Discounted.

Ans: Business Discounting is one such option, which allows a business to get quick payment for their work and meet their operating expenses without having to depend on any external agency to provide the funds. Bill Discounting, also called Invoice Discounting, is a trading activity where a seller sells some goods or services to a buyer. The buyer has to make the payment as per the agreed credit period. Now, if the buyer needs money before that, he can approach a bank or some NBFC and ‘sell’ that invoice to them. The financial institution gets the invoice verified by the buyer and then makes payment to the seller on their behalf. However, they make some deductions, called ‘discounts’, as their commission. So, in a way, the seller gets a discounted payment for their bill, This way, they can run their business operations, and buyers get an extended credit period. On the due date, the seller makes the payment to the financial institution, which completes the cycle for that particular invoice. Since the seller gets payment on a ‘discount’, this transaction is called Bill Discounting.

35. Write a short note on Columnar Investment Account.

Ans: Prior to electronic worksheets, accountants had several pads of paper with a varying number of columns (and rows) pre-printed on them, The pads of paper were labelled as columnar pads. The pre-printed paper in these pads allowed accountants to be bookkeepers to easily prepare manual spreadsheets.

The Investment Account is maintained in a columnar form with three amount columns on each side viz., Nominal, Interest/Income and principal/capital. The face value or nominal value of securities purchased or sold is recorded, however, in the ‘Nominal’ column. The accrued ‘Interest/Income’ column. The third column, ‘Capital/Principal’, reveals the true cost or true sales consideration.

Investors are one of the many players in the financial markets, who deploy savings when there is a surplus and demand it back when they are in need. The terms at which the money will be used or lent is determined by the marketplace and the investor’s choices have to be framed in this context. The focus, therefore, is not so much on the promises that can be made to the investor, but how well the investors evaluate their own cash-flow needs and that of the seekers of their money.

The summary of an investor’s financial life can be drawn in their columns on a worksheet. The first column holds the cash inflow of the investors. The second shows the drawdown or the outflow that may be needed. The third shows the value of assets the investor has accumulated.

Hi! my Name is Parimal Roy. I have completed my Bachelor’s degree in Philosophy (B.A.) from Silapathar General College. Currently, I am working as an HR Manager at Dev Library. It is a website that provides study materials for students from Class 3 to 12, including SCERT and NCERT notes. It also offers resources for BA, B.Com, B.Sc, and Computer Science, along with postgraduate notes. Besides study materials, the website has novels, eBooks, health and finance articles, biographies, quotes, and more.