NIOS Class 12 Economics Chapter 18 Cost of Production, Solutions to each chapter is provided in the list so that you can easily browse through different chapters NIOS Class 12 Economics Chapter 18 Cost of Production and select need one. NIOS Class 12 Economics Chapter 18 Cost of Production Question Answers Download PDF. NIOS Study Material of Class 12 Economics Notes Paper 318.

NIOS Class 12 Economics Chapter 18 Cost of Production

Also, you can read the NIOS book online in these sections Solutions by Expert Teachers as per National Institute of Open Schooling (NIOS) Book guidelines. These solutions are part of NIOS All Subject Solutions. Here we have given NIOS Class 12 Economics Chapter 18 Cost of Production, NIOS Senior Secondary Course Economics Solutions for All Chapters, You can practice these here.

Cost of Production

Chapter: 18

Module – VII: Producer’s Behaviour

TEXT BOOK QUESTIONS WITH ANSWERS

INTEXT QUESTIONS 18.1.

Q.1. Fill in the blanks using appropriate words from the choice given in brackets:

(i) Paid out cost is ________ (explicit cost, implicit cost).

Ans. Explicit cost.

(ii) Cost in business refers to ________ (implicit cost, explicit cost)

Ans. Explicit cost.

(iii) Implicit cost is compensation for_______ (hired factors, self-owned) and self-employed input.

Ans. Self-owned.

(iv) Cost in microeconomics includes _________ (explicit cost only, implicit cost only, both explicit cost and implicit cost).

Ans. Both explicit cost and implicit cost.

(v) Normal profit _________ a part of cost of production in microeconomics (is, is not).

Ans. Is.

INTEXT QUESTIONS 18.2.

Q.1. State whether the following statements are true or false:

(i) With increase in the quantity of output fixed costs increase.

Ans. False.

(ii) There are no variable costs at zero output.

Ans. True.

(iii) Expenses incurred on watchmen and property tax are fixed cost.

Ans. True.

(iv) Variable costs change with every change in output.

Ans. True.

(v) Cost incurred on all the labour is variable.

Ans. False.

INTEXT QUESTIONS 18.3.

Q.1. Fill in the blanks with appropriate words given in the brackets:

(i) Change in total cost when output varies are due to changes in ________ (fixed cost, variable cost).

Ans. Variable cost.

(ii) To find total cost we have to ________ total fixed cost and total variable cost (add, multiply).

Ans. Add.

(iii) Total cost ________ zero at zero output (is, is not).

Ans. Is not.

(iv) When output is zero total cost equals ________ (fixed cost, variable cost).

Ans. Fixed cost.

INTEXT QUESTIONS 18.4.

Q.1. Fill in the blanks with appropriate words given in the brackets:

(i) Average cost is ________ (cost per unit, cost incurred on additional unit).

Ans. Cost per unit.

(ii) To find total cost we have to ________ average cost by quantity of output (multiply, divide).

Ans. Multiply.

(iii) Average fixed cost ________ with the increase in output (falls, rises).

Ans. Falls.

(iv) Average total cost is the sum of and ________ (average fixed cost, average variable cost, variable cost, fixed cost).

Ans. Average fixed cost, Average variable cost.

INTEXT QUESTIONS 18.1.

Q.1. Fill in the blanks:

(i) Marginal cost is the ________ cost incurred on an additional unit of output.

Ans. Additional.

(ii) Marginal cost equals the change in total cost or the change in ________ per unit change in output.

Ans. Total variable cost.

(iii) Costs increase from 3 units to 4 units. As a result TC rises from Rs. 19.60 to Rs. 24.50. MC is ________.

Ans. Rs. 4.90.

TERMINAL EXERCISE

Q.1. What is implicit cost? How is it different from explicit cost?

Ans. Implicit cost: Compensation for the use of self-owned and self-employed resources is known as implicit cost. Implicit cost is also known as imputed cost. Example, the imputed rent of the self-owned factory building. It can be taken as equivalent to the actual rent paid for a similar type of building.

Explicit cost: All actual payments, on purchasing and hiring different goods and services used in production are called explicit costs. A firm purchases the services of assets like building, machine, etc. It pays hiring charges for building, normally termed as rent. It employs workers, accountant manager, etc. and pays wages and salaries to them. It borrows money and pays interest on it. It purchases raw material, pays electricity bills and makes such other payments.

Q.2. What is explicit cost? Distinguish it from implicit cost.

Ans. Explicit cost is that cost which is paid by businessman for buying raw materials and using services of factors of production.

Normally in business, the accountant takes into account only the actual money expenditure as cost. So, in business the cost is normally the implicit cost only.

Implicit cost: It is the cost of self-provided inputs. The businessmen do not make any payment for using services of self-provided inputs.

Difference: Explicit cost is paid in the form of money while no payment is made for implicit cost in the form of money.

Q.3. Explain the concept of ‘normal profit’. Justify that it is an element of cost in microeconomics.

Ans. Normal profit is an additional amount over the monetary and imputed cost that must be received by an entrepreneur to induce him to produce the given product. Normal profit is entrepreneur’s opportunity cost and therefore, enters into cost of production. Opportunity cost is the value of the opportunity or alternative that is sacrificed.

Normal profit as an element of cost: Normal profit is nothing but the minimum assured profit in the next best occupation. It is the reward which an entrepreneur must receive for the risk and uncertainties he bears in the production of a commodity. It can be proved with an example. Suppose there is a publisher who has the option of publishing commerce books or the science books. He chooses to publish commerce books because he gets more profit from these. Now suppose that the market for science books is more assured but profit is lower. This would mean that publisher who is publishing commerce books is sacrificing an assured return on science books is taking a risk. He would be prepared to face the risk only when he thinks that he would be able to earn at least the same profit which he would have in any way got from science books. Loss of assured return on science books is then an element of cost for the publisher who is publishing commerce books instead of science books. It is termed as ‘normal profit’ because it is that minimum profit which a producer must get in order to continue to produce the given good, otherwise he will discontinue production of that goods. In other words we can say that a producer must get normal profit in addition to recovering his ‘paid out cost’ and ‘imputed cost.’

It is clear from the above discussion that normal profit is an element of cost in microeconomics.

Q.4. Explain the various elements of cost in micro economics.

Ans. Various elements of cost: There are three elements of the total cost of production in microeconomics:

1. Money costs/paid out costs: For production a firm purchases the services of assets like building, material/machine, etc. It pays hiring charges for building, normally termed as rent. It employs workers, accountant, manager, etc. and pays wages and salaries to them. It borrows money and pays interest on it. It purchases raw material, pays electricity bills and makes such other payments. All such actual payments, on purchasing and hiring different goods and services used in production are called ‘Paid out costs’ or ‘explicit costs’.

2. Imputed cost: This cost refers to the estimated value of the inputs provided by the owner of the production unit (firm). The owner may supply his own labour as a manager, etc. his own funds and his own building. The value of these inputs is not entered into the accounts. But in economics, the value of these services provided by the owner is estimated and included in cost. These are in the form of imputed wages of the owner’s labour, imputed interest of the funds provided by the owner and imputed rent of the building provided by the owner.

In microeconomics, in addition to the paid out cost, imputed cost is also included in the cost of production. This is not all. There is yet another element of cost described as ‘normal profit’.

3. Normal profit: Normal profit means that minimum profit which a producer must get in order to continue to produce the given goods in the long-run. If a producer does not get this profit in the long run he will stop production of goods is high, low or nil. Similar is the position of cost like interest, salary of the permanent staff, depreciation, licence fees, etc. All these are fixed costs.

4. Variable costs: Variable costs are those costs which change with the change in output of a good.

Example of variable costs are cost on raw materials used in production, casual labour employed, power consumed in production etc. These costs are incurred only when actual production takes place. When output is increased, expenditure on raw material and labour also increases. For example, the firm producing pens will need more raw materials, more labour, etc. if it wants to produce more pen. But if the firm decides to reduce the productions, less will have to be spent on these items. In case production is completely stopped, no expenditure need be incurred on these items. This would mean that there are no variable costs at zero output.

Example: The concepts of fixed cost and variable cost will be more clear and better with the help of a schedule and an illustration. Suppose a firm producing pens incurs the following costs at different levels of output (as given in table). We see that its fixed cost remains constant whereas variable cost changes with every change in output. In this schedule, the fixed cost is Rs. 500 and remains the same at all levels of output. The variable cost is Rs. 60 when the producer is producing 100 pens. It rises to Rs. 100 when he produces 200 pens and to Rs. 150 at 300 pens and so on.

Table: Cost schedule of firm

| No. of pens in units (1 unit = 100 pen) | Total fixed cost (Rs.) | Total variable cost (Rs.) |

| 0 | 500 | 0 |

| 1 | 500 | 60 |

| 2 | 500 | 100 |

| 3 | 500 | 150 |

| 4 | 500 | 260 |

| 5 | 500 | 390 |

Q.5. Differentiate between the concepts of cost as used in business and in micro-economics.

Ans. We know that all production involves cost. To produce any commodity a producer or a firm requires inputs. A producers has to either incur expenditure on procuring various inputs or he provides these himself. The inputs may be partly purchased or partly provided. Actual payments on purchasing and hiring different goods and services used in production area called explicit cost or money cost. The concept of cost as used in business generally refers to money or explicit cost.

Money costs or explicit cost are not the only costs in microeconomics. In microeconomics cost is the sum of

(a) explicit cost.

(b) implicit cost. and

(c) normal profit.

Implicit cost is the cost of the inputs which are owned and supplied by the entrepreneur himself in the production of a commodity. Normal profit is the minimum supply prices of the entrepreneur which he must get in order to remain in the present business.

Q.6. Distinguish between fixed cost and variable cost with examples.

Ans. Fixed Cost: Expenditure which remains fixed irrespective of the quantity of output produced is classified is fixed cost. It is incurred whether the output is large or small or even when it is zero. It does not change when quantity of output is increased or decreased.

For example, a firm producing pens must have a building, machinery and equipment, a manager, a watchman, etc. whether it is producing smaller or larger quantity of pens. Suppose that the factory is not functioning for some period of time due to some reason. It means that no output is produced during that period. But still rent will have to be paid fee that period. Wages of permanent employees of the factory will have to be paid. These are unavailable costs which remains fixed. Examples of fixed costs are rent on factory, building, interest on money borrowed. Property taxes and salaries of permanent employees. All these costs remain the same whether the output is small or large or zero. Fixed costs are also called overhead costs.

Fixed costs are costs that do not vary with changes in the level of output. They remain fixed whatever may be the level of output.

Variable cost: Costs which change with every change in output are called variable costs. Variable costs are costs that directly vary with the changes in the level of output.

Examples of variable costs are cost on raw materials used in production casual labour employed, power consumed in production, etc. These costs are incurred only when actual production takes place. When output is increased expenditure on raw material and labour also increases. For example, the firm producing pens will need curve raw materials, more labour etc., if it wants to produce more pens. But if the firm were to reduce the production, less will have to be spent on these items. In case production is completely stopped. No expenditure need be incurved on these items. This would mean that there are no variable costs at zero output. These costs are available in the period during which the production is not done due to one reason or the other. These costs due incurred when actual production starts. There costs rise along with the increase in production.

Q.7. Explain the relationship between output and average fixed cost.

Ans. Average Fixed Cost (AFC): By dividing total fixed cost (TFC) by the number of units of output produced we get AFC.

AFC = TFC/units of output

Now, as output increases AFC falls because TFC is constant. So AFC continuously falls. For example, the total fixed cost of producer is ₹ 60 when he produced one unit. Average fixed cost is ₹ 60 (₹ 60 ÷ 1), but if the production is increased to 2 units average fixed cost is ₹ 30 (₹ 60 ÷ 2). When it produces 3 units it is ₹ 20 (60 ÷ 3). Therefore, the larger the output the lower will be the average fixed cost.

Q.8. Distinguish between AFC and AVC with suitable examples.

Ans. Average Fixed Cost (AFC): By dividing total fixed cost (TFC) by the number of units of output produced we get AFC.

AFC = TFC/units of output

Now, as output increases AFC falls because TFC is constant. So AFC continuously falls. For example, the total fixed cost of producer is ₹ 60 when he produced one unit. Average fixed cost is ₹ 60 (₹ 60 ÷ 1), but if the production is increased to 2 units average fixed cost is ₹ 30 (₹ 60 ÷ 2). When it produces 3 units it is ₹ 20 (60 ÷ 3). Therefore, the larger the output the lower will be the average fixed cost.

Average Variable Cost (AVC): Average variable cost is obtained by dividing the total variable cost by the units of output produced.

AVC = TVC/ Units of output

As output increases AVC falls in the beginning and then rises. When output of pen is one unit. TVC is ₹ 60, so AVC will be ₹ 60 (₹ 60 ÷ 1). TVC at 2 units of pens is Rs. 100. So AVC at 2 units of output of pen is Rs. 50 (Rs. 100 ÷ 2) and so on.

Q.9. Explain the term ‘marginal cost.” Show with the help of an example how is it calculated.

Ans. Marginal Cost (MC): MC is the additional cost of producing additional units of output. For example if total cost (TC) of one unit of output is Rs. 10 and that of two units is Rs. 18 then MC of two units output is Rs. 8 (18-10). Let total units of output be ‘n’ so

MCₙ = TCₙ – TCₙ–₁

= 18 – 10 = Rs. 8.

Q.10. Which cost, fixed or variables determines marginal cost? Give reason.

Ans. Variable cost determines marginal cost. It (marginal cost) is not affected by fixed cost because fixed cost remains constant. As output expands change in total cost are due to changes in variable cost only. So, marginal cost can also be calculated if only total variable costs are known to us. For example, take the following schedule (Table) showing TFC, TVC and TC. When MC is calculated from either TC or TVC we get the same result.

Table

| Output of pens (1 unit = 100 pens) | Total cost (Rs.) | TFC (Rs.) | TVC (Rs.) | MC (Rs.) |

| 0 | 60 | 60 | – | – |

| 1 | 120 | 60 | 60 | 60 |

| 2 | 160 | 60 | 100 | 40 |

| 3 | 210 | 60 | 150 | 50 |

| 4 | 320 | 60 | 260 | 110 |

| 5 | 450 | 60 | 390 | 130 |

Calculation of MC on the basis of TC and TVC

| Output of pens (1 unit = 100 pens) | TC | MC | TVC | MC |

| 0 | 60 | – | – | – |

| 1 | 120 | 60 | 60 | 60 |

| 2 | 160 | 40 | 100 | 40 |

| 3 | 210 | 50 | 150 | 50 |

| 4 | 320 | 110 | 260 | 110 |

| 5 | 450 | 130 | 390 | 130 |

Q.11. Classify the following expenditure into explicit costs and implicit costs:

(a) A farmer growing seeds and using for cultivation.

(b) Use of chemical fertilizers by a farmer.

(c) Use of the services of a tractor owned by the farmer.

(d) Farming by the farmer who owns the land.

(e) Unpaid family labour used on farms.

(f) Transport charges.

(g) Interest on borrowings.

(h) Wages paid.

(i) Use of own building for production.

(j) Excise duty.

Ans. Explicit costs:

(b) Use of chemical fertilizers by a farmer.

(f) Transport charges.

(g) Interest on borrowings.

(h) Wages paid.

(j) Excise duty.

Implicit costs:

(a) A farmer growing seeds and using for cultivation.

(c) Use of the services of a tractor owned by the farmer.

(d) Farming by the farmer who owns the land.

(e) Unpaid family labour used on farms.

(i) Use of own building for production.

Q.12. Classify the following expenditure into fixed cost and variable cost:

(a) Rent of the factor building.

(b) Wages to watchman.

(c) Annual licensing fee of factory premises.

(d) Raw material.

(e) Rent of the agricultural land.

(f) Seeds.

(g) Fertilizers.

(h) Interest on borrowings.

(i) Excise duty.

(j) Transport charges.

Ans. Fixed costs:

(a) Rent of the factor building.

(b) Wages to watchman.

(c) Annual licensing fee of factory premises.

(e) Rent of the agricultural land.

(h) Interest on borrowings.

Variable costs:

(d) Raw material.

(f) Seeds.

(g) Fertilizers.

(i) Excise duty.

(j) Transport charges.

Q.13. Calculate total cost, average total cost, average fixed cost, average variable cost and marginal cost, on the basis of the following information:

| Output (units) | TFC | TVC |

| 0 | 60 | 0 |

| 1 | 60 | 50 |

| 2 | 60 | 90 |

| 3 | 60 | 180 |

| 4 | 60 | 300 |

Ans.

| Total cost (Rs.) (TFC+TVC) | AFC (Rs.) | AVC (Rs.) | ATC (Rs.) | MC (Rs.) |

| 60 | – | – | – | – |

| 110 | 60 | 50 | 110 | 50 |

| 150 | 30 | 45 | 75 | 40 |

| 240 | 20 | 60 | 80 | 90 |

| 360 | 15 | 75 | 90 | 120 |

Working notes:

1. AFC = TFC/ Output

2. AVC = TVC/ Output

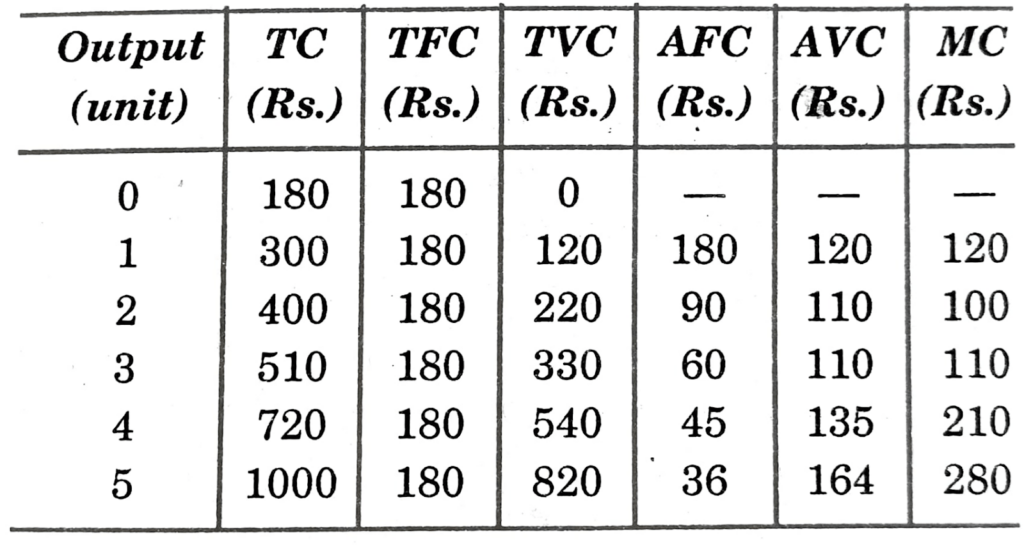

Q. 14. Calculate:

(i) TFC and TVC.

(ii) AFC and AVC.

(iii) MC.

from the following data:

| Output (units) | TC |

| 0 | 180 |

| 1 | 300 |

| 2 | 400 |

| 3 | 510 |

| 4 | 720 |

| 5 | 1000 |

Ans.

Working Note:

1. TC at zero level of output is TFC

2. TVC = TC – TFC.

3. AFC = TC / Output

4. AVC = TVC / Output

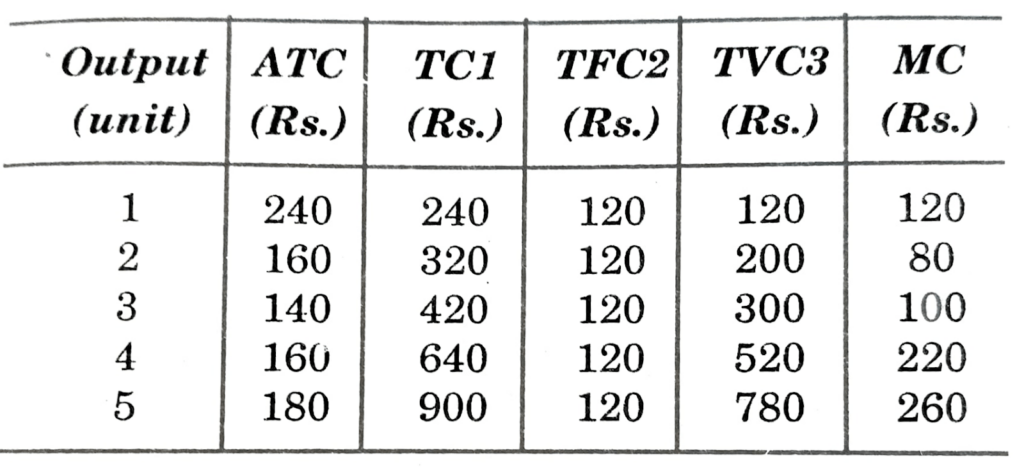

Q.15. Suppose that TFC is Rs. 120, find out

(i) TC and TVC.

(ii) MC from the following data:

| Output (units) | TC (Rs.) |

| 1 | 240 |

| 2 | 160 |

| 3 | 140 |

| 4 | 160 |

| 5 | 180 |

Ans.

Working Notes:

(i) TC = ATC x Output (Q)

(ii) TFC = Rs. 120

(iii) TVC = TC – TFC.

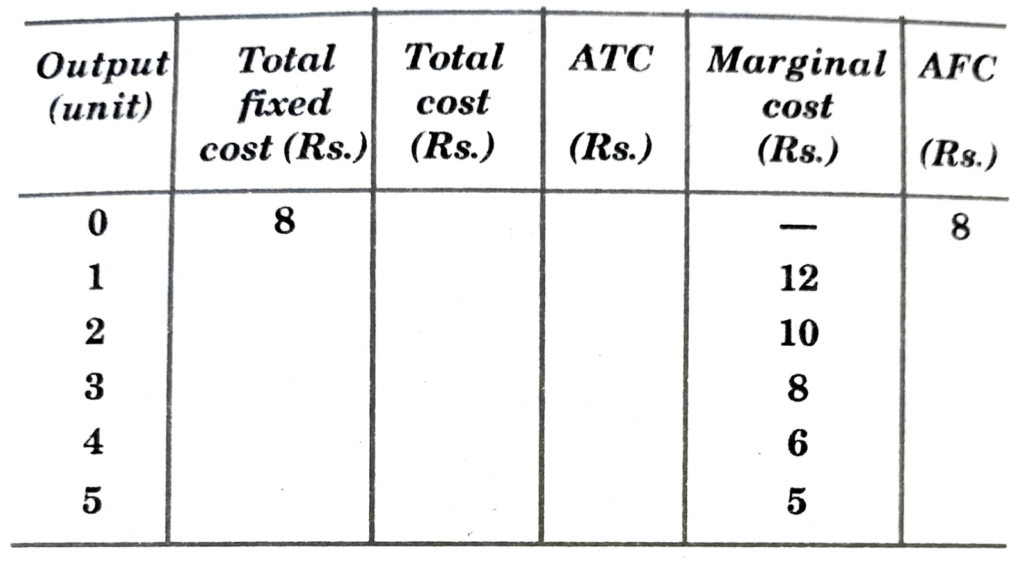

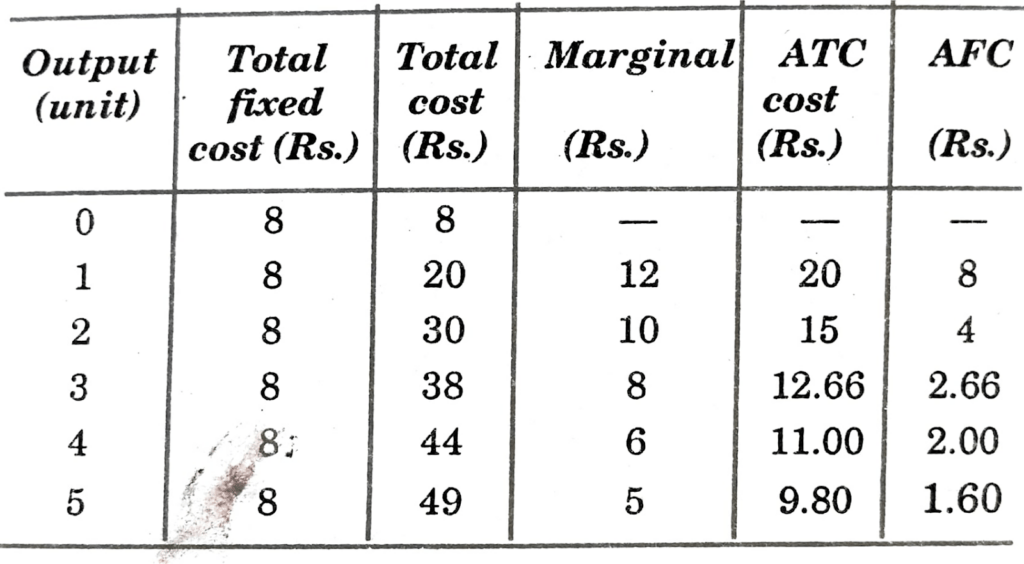

Q.16. Fill in the blanks:

| Output (units) | TC (Rs.) | TFC (Rs.) | TVC (Rs.) | MC (Rs.) |

| 1 | 12 | – | – | – |

| 2 | 20 | – | – | – |

| 3 | 24 | – | – | – |

| 4 | 30 | – | – | – |

| 5 | 44 | – | – | – |

Ans.

| Output (units) | TC (Rs.) | TFC (Rs.) | TVC (Rs.) | MC (Rs.) |

| 1 | 12 | 12 | 0 | – |

| 2 | 20 | 12 | 8 | 8 |

| 3 | 24 | 12 | 12 | 4 |

| 4 | 30 | 12 | 18 | 6 |

| 5 | 44 | 12 | 32 | 14 |

Q.17. Complete the following table:

Ans.

Some Other Important Questions For Examinations

Very Short Answer Type Questions

Q.1. What do you mean by cost of production?

Ans. Cost of production refers to the expenses incurred on the factor inputs used in production of a commodity.

Q.2. What are explicit costs?

Ans. All actual payments, on purchasing and hiring different goods and services used in production are called explicit costs.

Q.3. In business which cost is normally used?

Ans. In business, the accountant takes into account only the actual money expenditure as cost. So, in business the cost is normally the explicit cost only.

Q.4. What are implicit costs?

Ans. Implicit costs refer to those costs which arise due to the factors supplied by the producers.but for which no payment is made in cash.

Q.5. What is normal profit?

Ans. Normal profit is an additional amount over the monetary and imputed cost that must be received by an entrepreneur to induce him to produce the given product. Normal profit is entrepreneur’s opportunity cost and therefore, enters into cost of production.

Q.6. Mention the elements of the total cost of production in microeconomics.

Ans. There are three elements of the total cost of production in microeconomics:

(i) Explicit costs.

(ii) Implicit costs.

(iii) Normal profits.

Q.7. What is a private cost?

Ans. Private costs are the costs to an individual firm in producing a commodity.

Q.8. What is a social cost?

Ans. Social costs are the costs of producing a commodity to the society as a whole.

Q.9. What is fixed cost?

Ans. The fixed cost refers to the expenses incurred on variable inputs used in the process of production of a commodity.

Q.10. What is meant by prime cost?

Ans. Prime costs are also known as variable costs and refer to expenses incurred on those factor inputs whose quantity need be varied at different levels of output.

Q.11. What are variable costs?

Ans. Costs which change with every change in output are called variable costs.

Q.12. What is total cost?

Ans. Total cost of a given volume of output is the sum of the explicit and implicit costs and normal profit.

Q.13. How the average fixed cost is obtained?

Ans. Average fixed cost is obtained by dividing total fixed cost by the number of units of output produced.

AFC = TFC/ Units of output

Q.14. What is average variable cost?

Ans. The average variable cost is per unit variable cost in producing a commodity.

Q.15. What is average total cost?

Ans. Sum of average fixed cost and average variable cost is known as average total cost.

Q.16. What is marginal cost?

Ans. Additional cost incurred on producing an additional unit of output is known as marginal cost.

Q.17. Define cost.

Ans. Cost refers to all sorts of monetary expenditures incurred in the production of the commodity.

Q.18. How can average variable cost obtained?

Ans. Average variable cost can be obtained by dividing total variable cost by the quantity of output.

Q.19. When the average cost is important?

Ans. Average cost is important when the firm wants to calculate its profit.

Q.20. In which situation marginal cost is important?

Ans. Marginal cost is important for deciding whether any additional output can be produced or not.

Q.21. How does total fixed cost change when output changes?

Ans. When output changes, total fixed cost remains same because fixed costs do not vary with the level of output.

Q.22. What is the general shape of MC curve?

Ans. MC curves are generally U-shaped.

Q.23. What is the general shape of AFC curve?

Ans. The shape of AFC curve is downward sloping.

Q.24. What will happen to ATC when MC > ATC?

Ans. When MC > ATC then ATC will increase.

Q.25. What is the general shape of the AC curve?

Ans. The shape of AC curve is generally U-shaped.

Hi! my Name is Parimal Roy. I have completed my Bachelor’s degree in Philosophy (B.A.) from Silapathar General College. Currently, I am working as an HR Manager at Dev Library. It is a website that provides study materials for students from Class 3 to 12, including SCERT and NCERT notes. It also offers resources for BA, B.Com, B.Sc, and Computer Science, along with postgraduate notes. Besides study materials, the website has novels, eBooks, health and finance articles, biographies, quotes, and more.