Class 11 Economics Chapter 3 Production & Costs, (Assam Higher Secondary Education Council) AHSEC Class 11 Economics Question Answer in English Medium each chapter is provided in the list of AHSEC so that you can easily browse through different chapters and select needs one. Assam Board Chapter 3 Production & Costs Class 11 Economics Question Answer can be of great value to excel in the examination.

AHSEC Class 11 Economics Chapter 3 Production & Costs

Class 11 Economics Chapter 3 Production & Costs Notes cover all the exercise questions in SCERT Textbooks. The SCERT Class 11 Economics Chapter 3 Production & Costs Solutions provided here ensure a smooth and easy understanding of all the concepts. Understand the concepts behind every chapter and score well in the board exams.

Production & Costs

Chapter – 3

PART – A

VERY SHORT ANSWER QUESTIONS

1. What does the production function of a firm refer to ?

Ans: Production function is a functional relationship between physical inputs and physical outputs. For various quantities of inputs used, it gives the maximum quantity of output that can be produced.

2. Suppose there are two factors in a production process, ― factor 1 and factor 2. Write down the production function.

Ans: Q = F (Factor 1, factor 2)

3. Simplify the meaning of the following production function q = f ( x₁.x₂ ).

Ans: With the given amount of input X₁ , and X₂ , the output ‘q’ have been produced.

4. What is an isoquant ?

Ans: An isoquant shows different combinations of factors of production , which when used in the production process , yield equal production or equal amount of output and the producer will be indifferent as regards choice among those factor combinations.

5. Write true or false :

In the long run, there is no fixed input.

Ans: True

6. What us average product ?

Ans: Average product of an input is defined as the output per unit of variable inputs. i.e. Ap=TP/Qx

7. What is marginal product ?

Ans: Marginal product of an input is defined as the change in output per unit of change in the input , when all other inputs are held constant i.e. MP = Change in output/ change in input

8. What does the cost function of a firm reveal ?

Ans: Cost function refers to the mathematical relation between cost of a product and the various determinates of its costs. In the cost function , the dependent variable is unit cost or total cost and the independent variables are variable cost .

9. Fill in the blank :

TC= ____+ TFC .

Ans : TVC

10. How can you define marginal cost at zero level of output ?

Ans: Can’t define.

11. Fill in the blank :

AC = AVC + ___.

Ans : AC = AVC + AFC

12. The total output of a firm is 60 units when it uses 12 units of labor.Calculate average product of labour.

Ans : AP=TP/L=60/12=5 units

13. The total product of a firm is 70 units when it employs 10 units of labour. If the level of output increases to 75 units due to one increase in labour , find out the marginal product of labour.

Ans: Marginal Product of Labour is MPL= 5 units

14. The total cost of a production unit is Rs. 100 and it produces 10 units of output . If the marginal cost of the 11th unit of the product is Rs. 15 , what will be the total cost of the production unit ?

Ans: 115 units.

15. Write true or false :

In the process of production, the consumer combines the inputs and produces output.

Ans: True.

16. Write true or false :

The revenue earned by a firm is called profit.

Ans: False .

17. Write true or false :

The production function of a firm reveals the relationship between inputs used and output produced by it.

Ans: True.

18. Choose the correct portion :

( Marginal product / total product / average product ) – is defined is the change in output per unit of change in the input when all other inputs are held constant .

Ans: Marginal Product.

19. Choose the correct portion :

When a proportional increase in all inputs results in an increase in output but by less than the proportion, it calls ( decreasing returns to scale / increasing returns to scale / constant returns to scale ) .

Ans: Decreasing Returns to Scale.

20. Fill in the blanks :

In order to produce output , the firm needs to employ___.

Ans: Inputs.

21. What does the constant return to scale imply ?

Ans: A proportional increase in all inputs results in an increase in output by the same proportion.

22. What is increasing return to scale ?

Ans: A proportional increase in all inputs results in an increase in output by more than the proportion.

23. What does return to scale refer ?

Ans : It refers to the long run production function.

24. Fill in the blanks :

(i) A.C= Total Cost/?

(ii) T.C= TVC+___

Ans: (i) A.C= Total Cost/quantity

(ii) T.C= TVC+TFC

25. Fill in the blanks :

The relationship between inputs used and output produced by the firm is called___.

Ans : production function.

26. What is factors of production ?

Ans: Whatever is used in the production process is called factors of production.

27.State any two factors affecting the supply of a commodity.

Ans: The two factors affecting the supply of a commodity are –

(a) Price of the commodity : There is a direct relationship between price of a commodity and its quantity supplied Generally higher the price , higher the quantity supplied and vice versa.

(b) Prices of other goods : The supply of a good depends upon the prices of other goods . An increase in the prices of other goods makes them more profitable for the firms. They will increase their supply .

B. SHORT ANSWER QUESTION TYPE- II : ( MARKS : 3 )

1. Distinguish between input and output .

Ans : Inputs are the ways or methods through which production is done and output are its results, that are provided by the services of the inputs.

2. Distinguish between fixed input and variable input.

Ans: Fixed input do not changes with the level of production, but th variable inputs changes with the level of production output.

3. Distinguish between short – run and long – run.

Ans : In the short run , a firm cannot vary all the inputs. One of the factors , factor 1 or factor 2 cannot be varied and therefore, remain fixed in the short run. In order to vary the output level, the firm can vary only the other factor . The factor that remains fixed is called the fixed input , whereas the other factor , which the firm can vary is called the variable input .

In the long run, all factors of production can be varied. A firm in order to produce different level of output in the long run may vary both the inputs simultaneously. So, in the long run , there is no fixed input .

4. State the law of diminishing marginal product.

Ans : The law of diminishing marginal product says that if we keep increasing the employment of an input , with other inputs fixed, eventually lity. a point will be reached after which , the resulting addition to output will re start falling .

5. State the law of variable proportion .

Ans : The law of variable proportion states that as the proportion of factors is changed , the total production at first increases more than proportionately and finally less than proportionately.

6. Define average variable cost.

Ans : Average fixed cost of a firm is equals to total fixed cost divided by output . i.e , AFC = TFC/Q

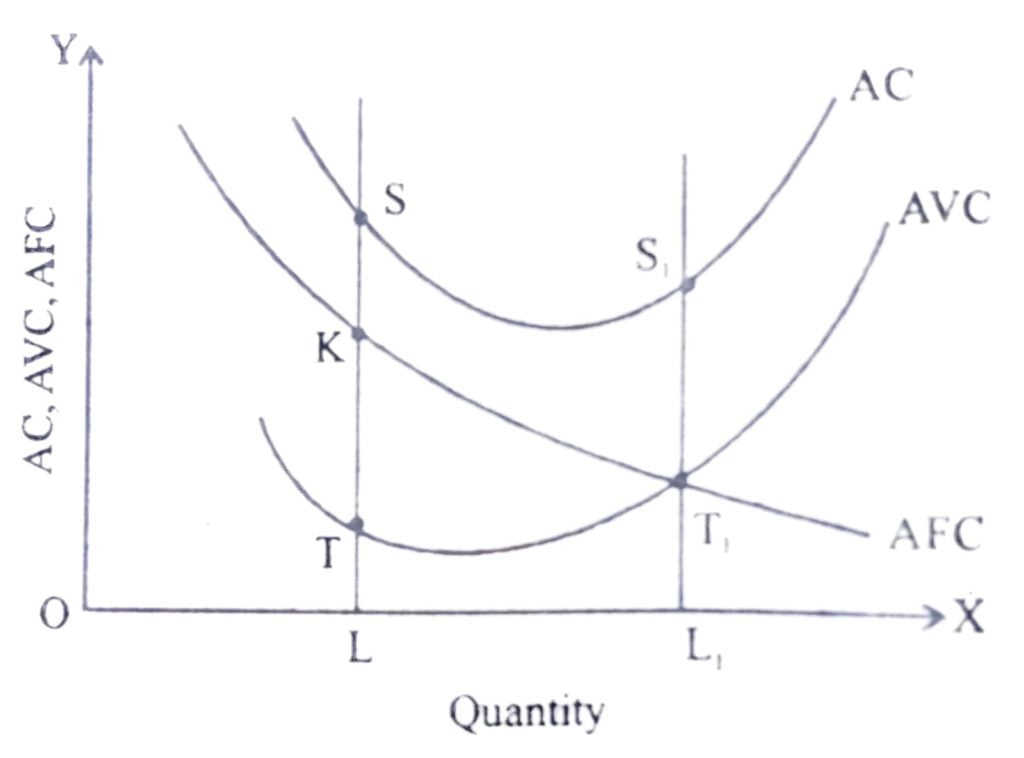

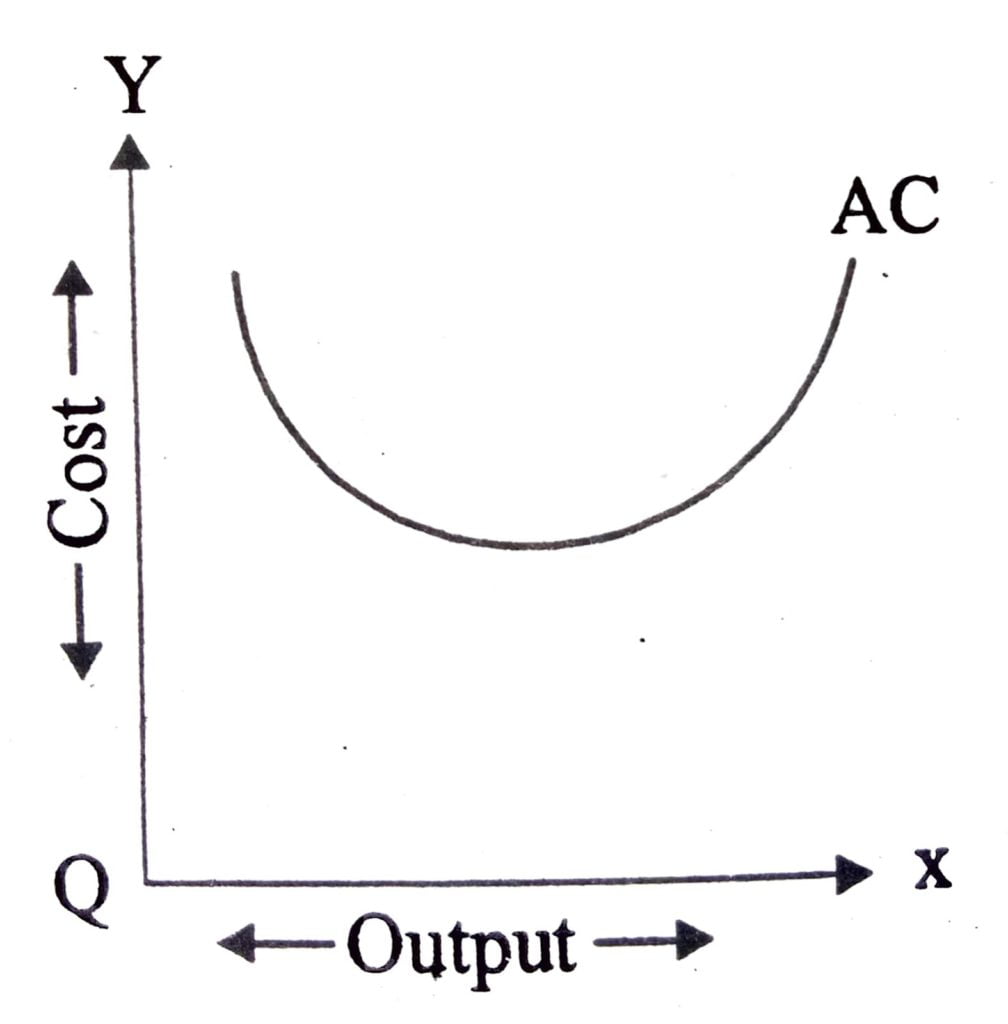

Average variable cost of a firm is the total variable cost divided by the output , AVC = TVC/Q. Average cost of a firm is the total cost divided by output. Cost per unit of commodity is called average cost .In the words of Dooley. “The average cost of production is the total cost per unit of output.”

Average cost is the sum total of average fixed cost variable and average cost i.e. , AC = AFC + AVC It is shown in the following diagram .

In the diagram, AC is the average cost curve, AVC is the average variable cost curve and AFC is the average fixed cost curve.

When output = OL

AVC = LT

AFC = LK

AC = ( AVC + AFC ) = ( LT + LK ) = LS

LT = SK

Likewise , when output = OL ,

AVC = L₁T₁

AFC = L ₁ T₁

AC = L ₁T ₁ + L ₁ T ₁

= L ₁ S₁

L₁T₁ = T ₁ S ₁

7 . In which situation a production function satisfy increases returns to scale ?

Ans : A production function satisfy increasing returns to scale , when proportional increase in all inputs result in an increase in output by than the proportion .

8. When does a production function hold constant returns to scale ?

Ans: A production function satisfy constant returns to scale , when a proportional increase in all inputs results in an increase in output by the same proportion.

9. State the reason behind the U – shaped short – run marginal cost curve.

Ans : Marginal cost is the additional cost that a firm incurs to produce one extra unit of output. According to the law of variable proportions initially , the marginal product of a factor increases as employment increases , and then after a certain point, it decrease.This means initially to produce every next unit of output , the requirement of the factor becomes less and less and then after a certain point , it becomes greater and greater . As a result , with the factor price given , initially the SMC falls and then after a certain point , it rises . SMC curve is therefore , ‘ U ‘ shaped .

10. What is isoquant ? Explain graphically.

Ans : An isoquant shows different combinations of factors of production , which when used in the production process , yield equal production or equal amount of output and the producer will be indifferent as regards choice among those factor combinations.

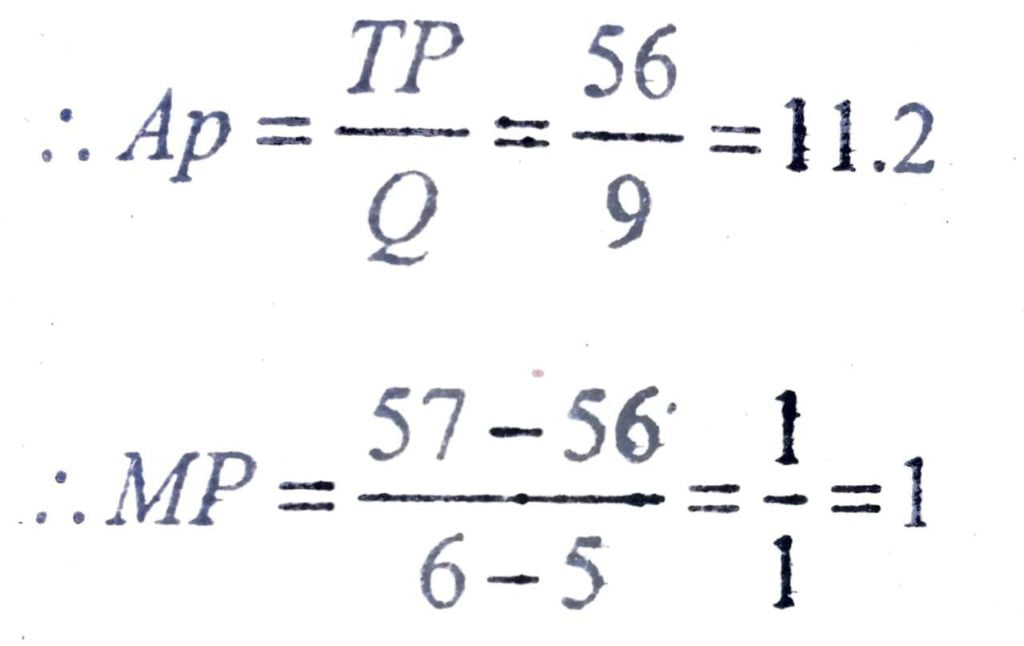

11. If the total production with 5 units of a variable factor is 56, calculate the average product. If the variable factor is increased by 1 more unit as a result of which the total factor becomes 57 , what will be the marginal product ?

Ans: Given TP = 56

Q= 5

Again, the variable factor increased by 1 more unit

Q₁ = 6

12. State the reasons behind the working of the law of diminishing marginal product .

Ans: Causes of diminishing returns to a factor are as fallows :

(a) Fixity of the factor : Fixity of the factor is the principal cause that explains the occurrence of the law of diminishing returns . As more and more units of the variable factor recontinue to be combined with the fixed factor, the letter gets overutilized.

(b) Imperfect factor substitutability : Factors of production are imperfect substitutes of each other. More and more of labour for example, cannot be continuously used in place of additional capital. Accordingly, diminishing return to the variable factor become inevitable.

(c) Poor co – ordination between the factor : Continuous increasing application of the variable factor along with fixed factor beyond a point cross the limit of ideal factor ratio. This results in poor co ordination between fixed and variable factors. The law of diminishing returns accordingly sets in.

13. Give the meanings of increasing returns to scale, decreasing returns to scale and constant returns to scale .

Ans: In the long run , all factors of production become variable; no factor remains fixed . In this period, production of a commodity can b increased by increasing all the factors in the same proportions. If all factors are increased in the same proportion, the scale of production increases and the corresponding behaviour of output is studied as return to scale. Thus , returns to scale refers to the behaviour of output as all factor inputs are varied in the same proportion . It is a long run concept. According to Watson , ” Returns to scale relates to the behaviour of total output as all inputs are varied in the same proportion and it is a long run concept . ” There are three types of returns to scale .

They are :

(a) Increasing returns to scale ,

(b) Constant return to scale ,

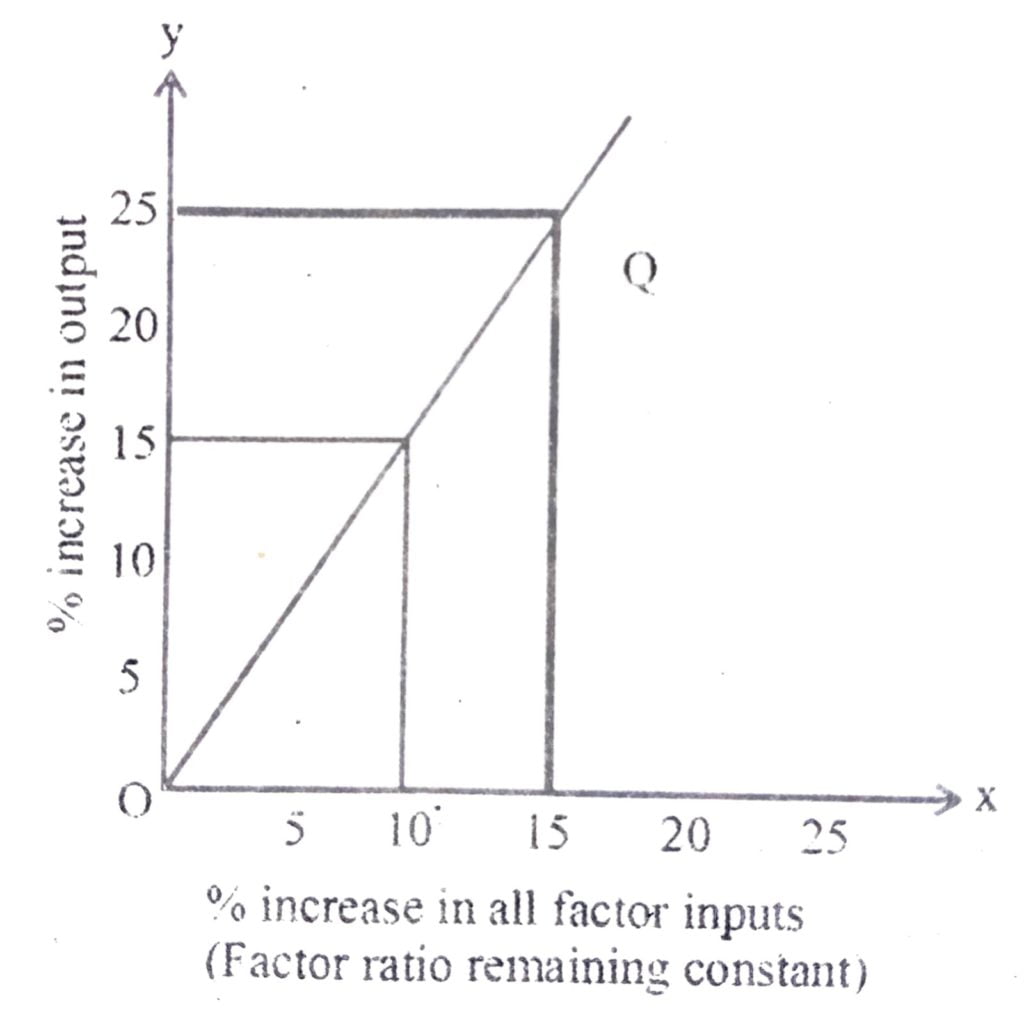

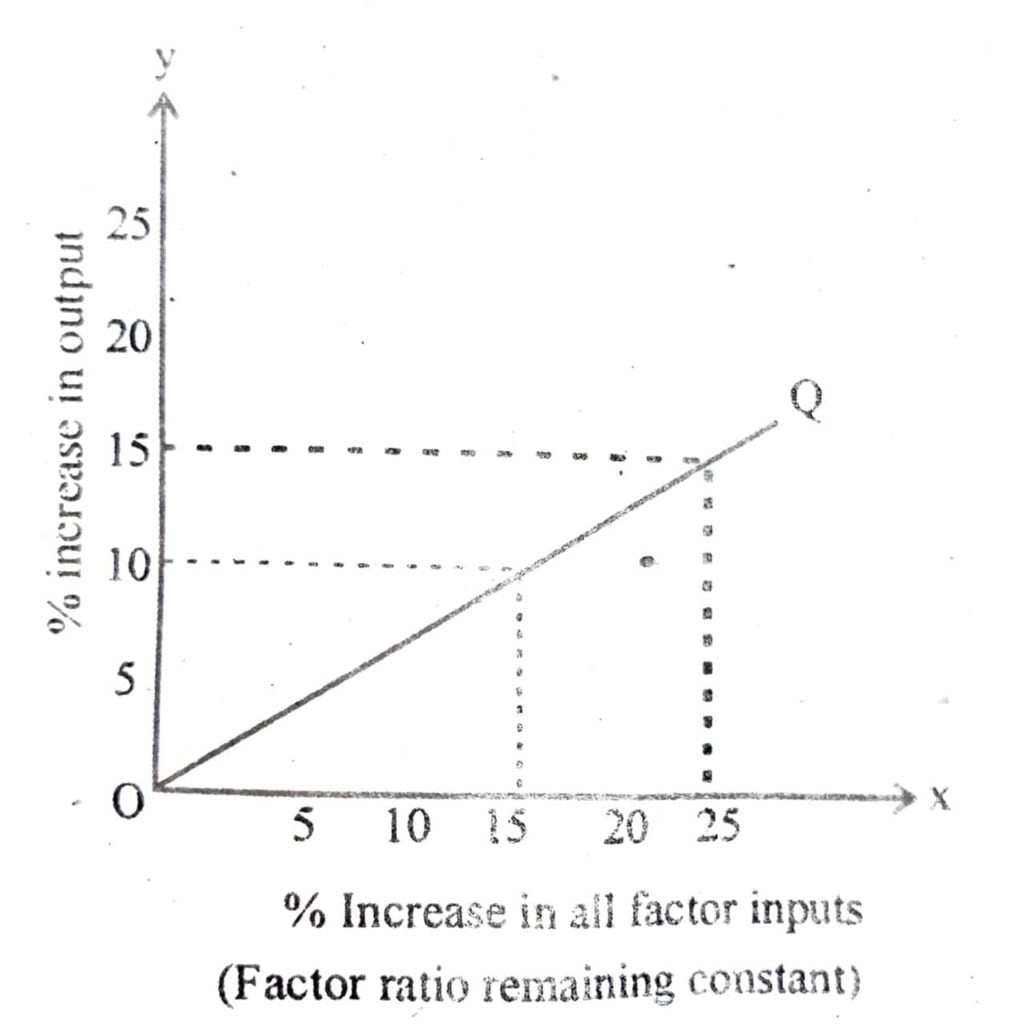

(c) Diminishing return to scale occur when a given percentage Increasing in all factor inputs causes proportionately greater increase in output . If 10% incomes in all factor input cause , say 15 % increase in output , it is evidently a case of increasing return to scale . This is illustrated in the figure beside The fig.

shows that 10 % increase in all factor inputs causes 15 % crease in output . Likewise, 15% crease in factor inputs causes 25% increase in output. Thus , any percentage increase in inputs is causing a greater percentage increase in output .

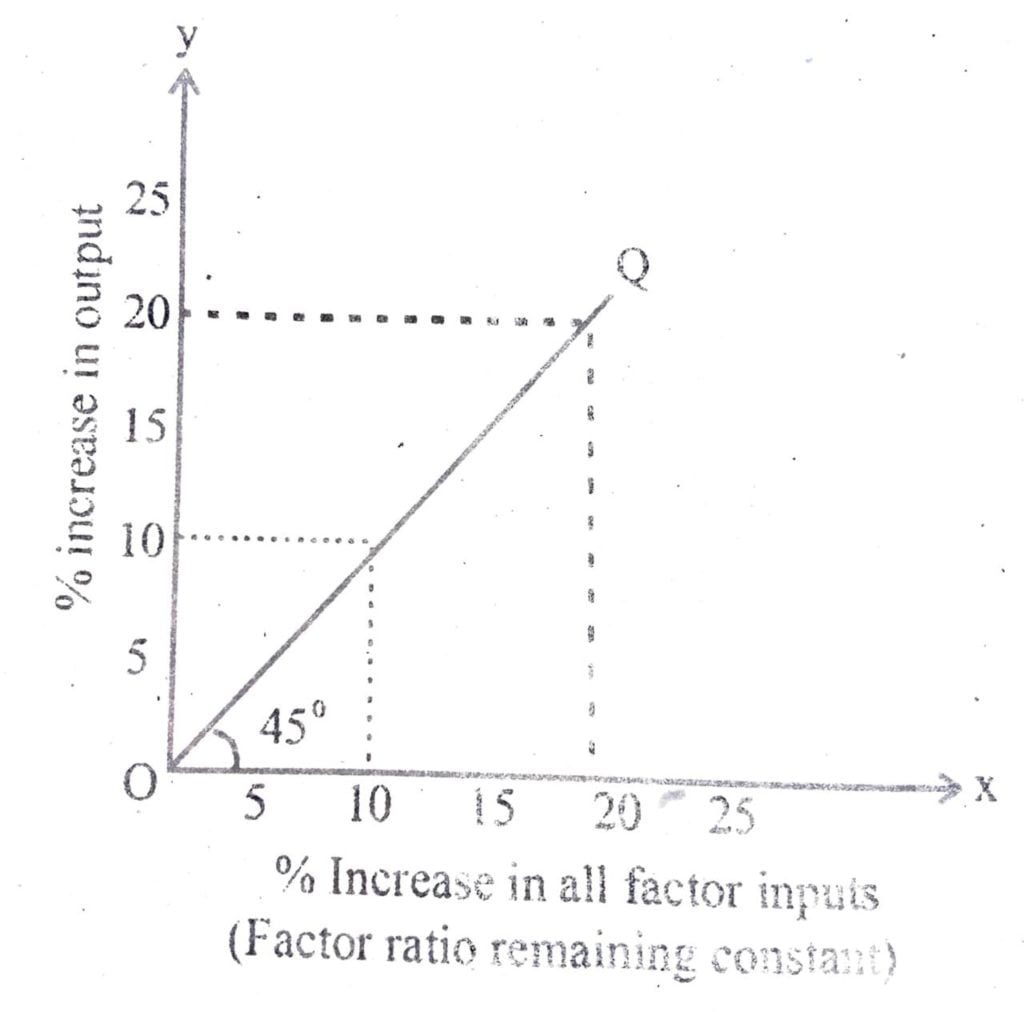

Again , constant returns to scale occurs when a given percentage increase in all factor inputs causes equal percentage increase in output , If 10 % increase in all factor inputs causes 10 % increase in output , it is a case of constant returns to scale. The following figure illustrate this situation.

the fig. shows that 10 % increase in all factor inputs causes 10 % increase in output . Likewise, 20 % increase in input causes 20 % increase in output. Thus, any percentage increase in inputs is matched with equal percentage increase in output. OQ line , accordingly forms a 45 ° angle from the origin .

On the other hand , diminishing returns to scale occur when a given percentage increase in all factor inputs causes proportionately lesser increase in output . If 15 % increase in all factor inputs causes , say , only 10 % increase in , output it is a case of diminishing returns to scale. The fig shows that 15% increase in altr. inputs causes only 10% increase in output. Likewise, 25% increase factor inputs causes only 15% increase in output. Returns to scale thus diminishing.

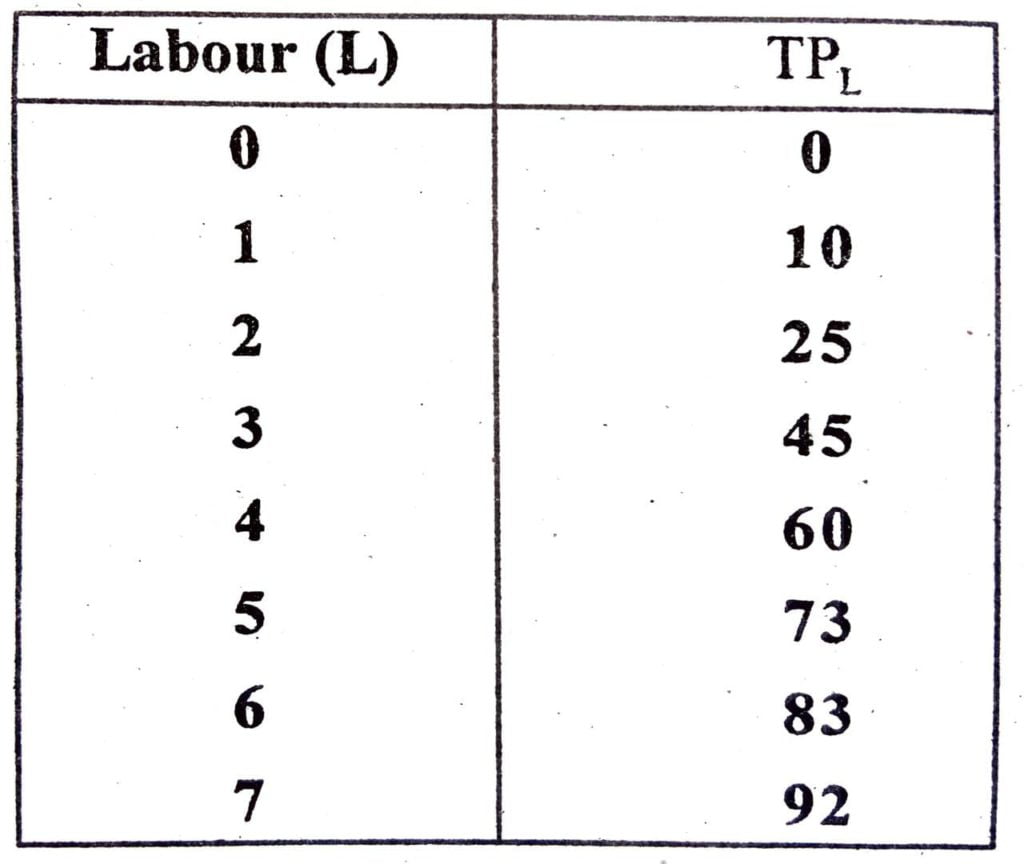

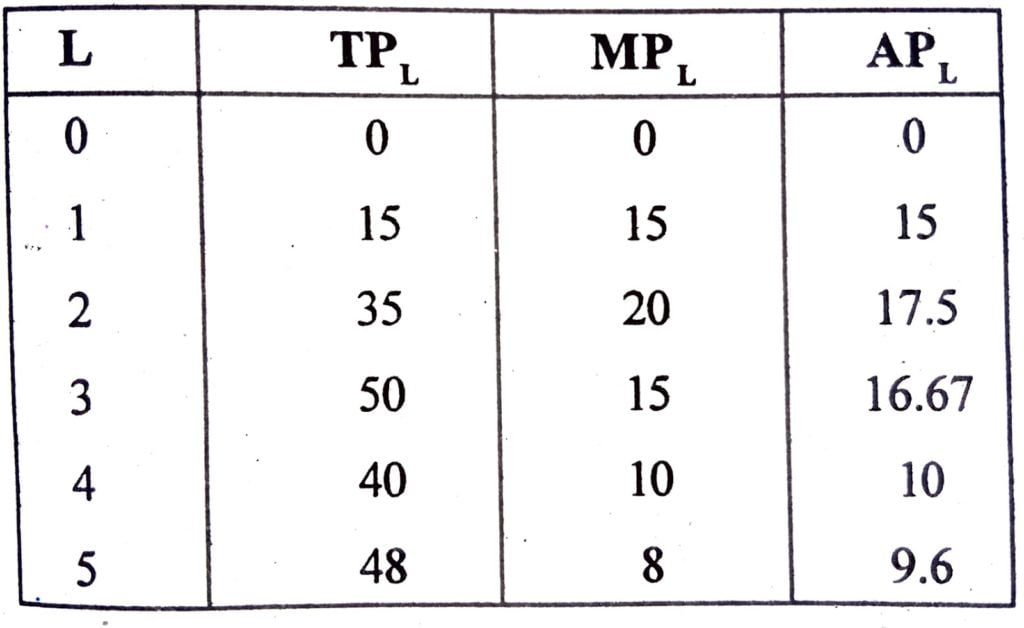

14. The total production schedule (TPL) of labour (L) is give Find out the average product schedule (APL) and marginal proda schedule (MPL) of labour.

Ans:

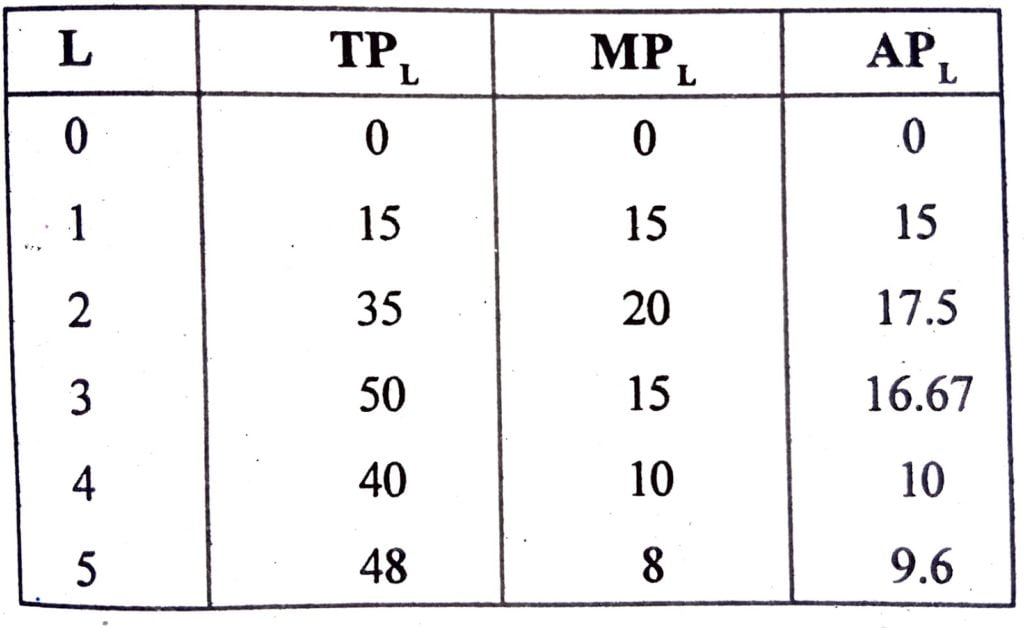

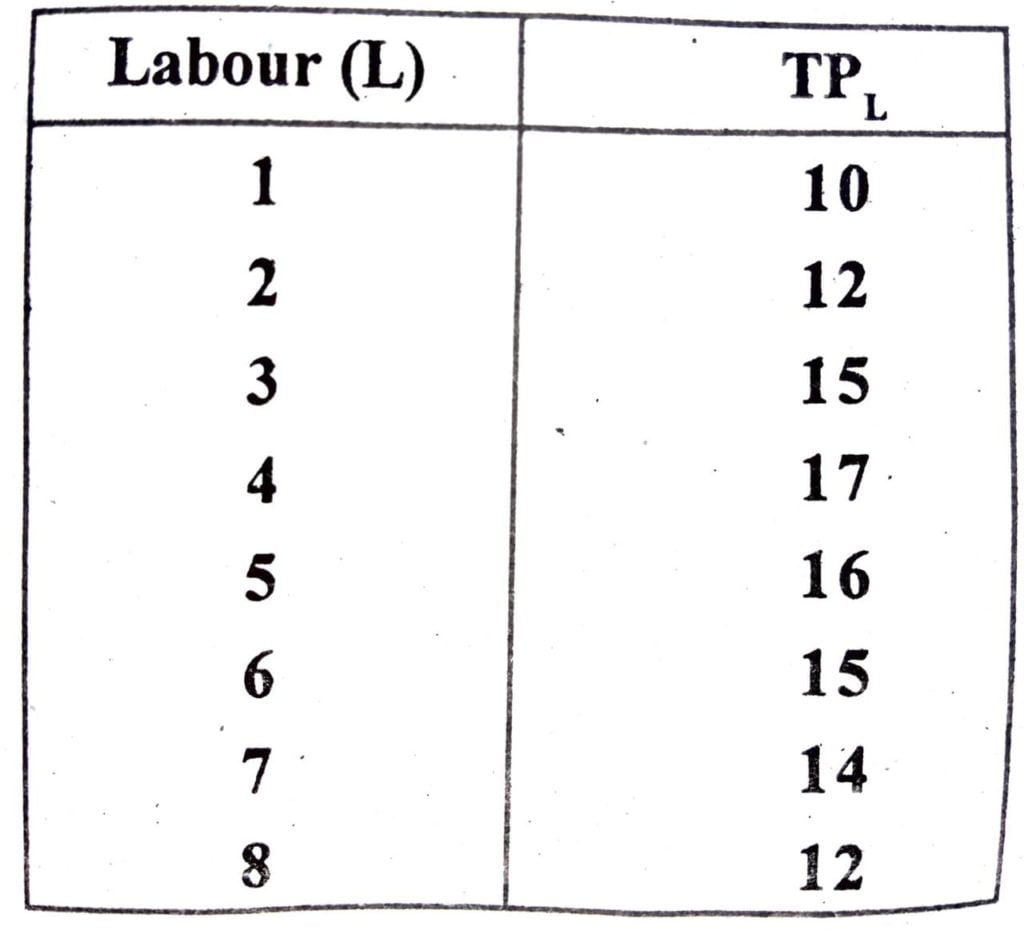

15. The average product schedule (APL) of labour (L) is given below. Find out the total product schedule (TPL) and marg product schedule (MPL)

Ans:

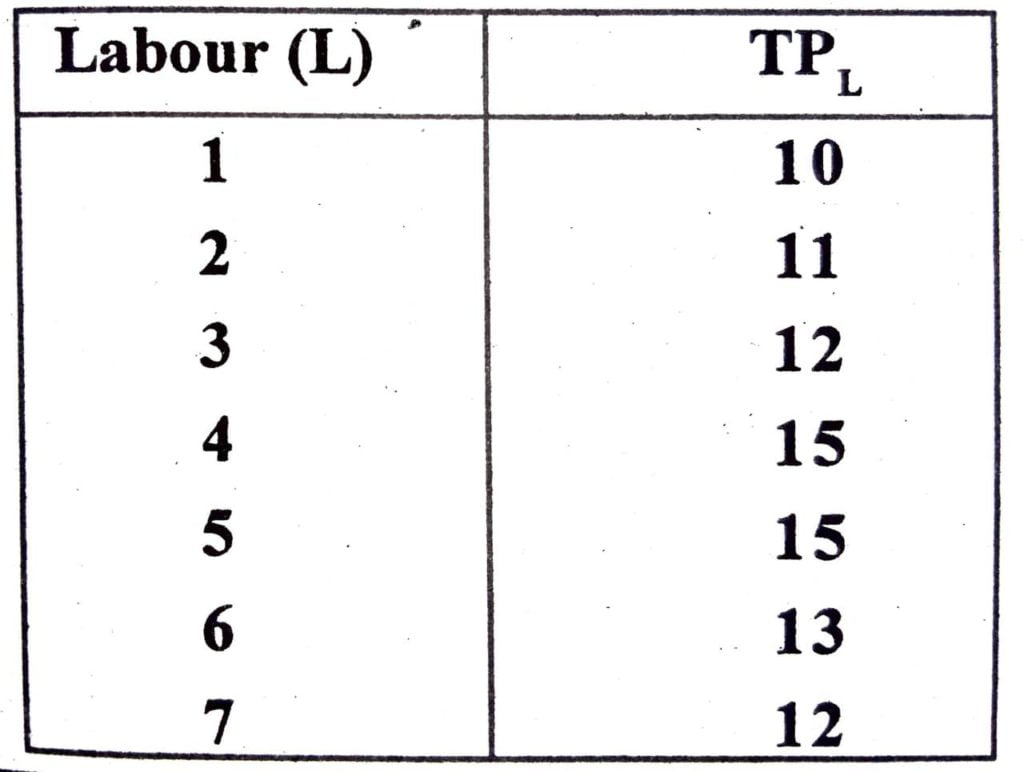

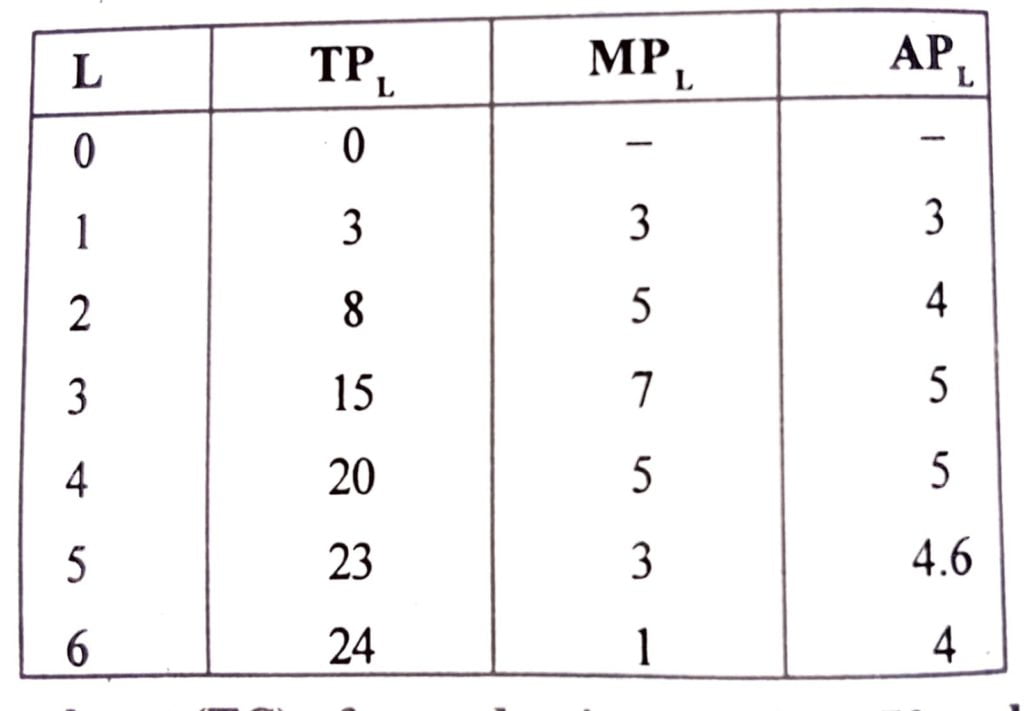

16. The marginal product schedule of labour (L) is given below. Find out the total product schedule (TPL) and average product schedule (APL) of labour.

Ans:

17. The total cost (TC) of a production unit is Rs. 70 and the level of output (Q) is 5. Find out the average cost (AC) and variable cost (AVC) if the average fixed cost (AFC) is Rs. 4.

Ans: Given, T Rs. = 70

Q = 5

∴ AC= TC/Q =70/5 =14

Niw, we know that,

AC=AVC + AFC

⇒14=AVC +4

∴ AVC=14-4=10

18. The total fixed cost of a firm is Rs. 100, when it produces 15 units of output. If the level of output increases to 30 units, will be the fixed cost in the short-run ? Explain.

Ans : Total fixed cost (TFC) = Rs. 100

Level of output, Q=15 units

increase in output = 30 units

We know that fixed costs of a firm do not vary with the level of output. They remain fixed even if the production process is temporarily shut down. So although the level of output increases from 15 units to 30 units. The fixed cost in the short run will be same as before i.e. Rs. 100. Thus the fixed costs in the short run is Rs. 100.

19. What is Cobb-Douglas Production function.

Ans: Cobb-Douglas Production function is

Q-AKᵃLᴮ

Where Q= quantity

A=constant

K=Capital

L= labour

20. Match the following:

(a) Law of variable proportion

(b) Returns to scale

(c) Long run average cost curve

(i) U shoe

(ii) Short run

(iii) Long run

Ans: (a) Law of variable proportion

(b) Returns to scale

(c) Long run average cost curve

(ii) Short run

(iii) Long run

(i) U shoe

21. State the reasons behind the U-shaped long-run average cost curve.

Ans:

Long run average cost curve is U shaped due to operation of law of variable proportions increasing returns imply diminishing costs, constant returns mean constant costs and diminishing returns imply increasing costs. An output is increased, AC first falls, reaches its minimum and then rises. Hence AC curve became U- shaped. Minimum point of AC curve indicates lowest per unit cost of production.

22. State the relationship between TC, AC and MC in a process of production.

Ans : (i) AC and MC are derived from TC.

(ii) AC and MC curve are U shaped due to the law of variable proportions.

(iii) When TC rises at a diminishing rate, MC declines.

(iv) When the rate of increase is total cost start rising the MC is increasing.

23. Explain the concept of short-run and long-run in the of production.

Ans: A period is defined as short run or long run simply by looking at weather all the inputs can be varied or not. In the short run, a firm cannot alter all the inputs. Only one factor can be varied other factors remain fixed in the short run. The firm does not have sufficient time to very factors like machine, building etc.

In the long run a firm can change all factors of production. To produce different levels of output, it may vary both the inputs simultaneously. Hence there is nothing like fixed input in the long run. Long run, thus refers to longer time period than the short run.

24. Explain the meaning of returns to scale with the help of a production function.

Ans: Return to scale studies the behaviour of output, when all the factor inputs are changed, simultaneously, in the same proportion, in the lo run. When we change all the inputs, that too in the same ratio, it leads a change in scale of production. For example one unit of capital (k) a one unit of labour (L) i.e. Ik+1L produce 100 units of output. If inputs are doubled i.e. 2k+2L then output may increase by more then 100%, equal to 100% or by less then 100% All these possibilities are returns to scale which called used. Increasing returns to scale, constant returns to sc and diminishing returns to scale.

25. Explain the reasons behind the working of the law of variable proportion.

Ans: The reason behind the working of the law of variable proportion are as follows :

(i) Better utilisation of the fixed factors

(ii) Increase efficiency of variable factors (iii) Indivisibility of fixed factor.

(iv) Optimum combination of factors

(v) Imperfect substitutes.

(vi) Limitation of fixed factor

(vii) Poor coordination between variable and fixed factor

(viii) Decrease in efficiency of variable factor.

26. Explain the relation between market price and marginal revenue of a price taking firm.

Ans: Marginal revenue refers to the increase that a company received when it sells one additional unit of a product. At first glance, you might assume that marginal revenue is simply the price of the product: If your product selles for $5, for example , it would appear you’d get $5, in revenue if you sold one unit. But it’s more complicated than that.

27. State any two assumptions of the law of variable proportions.

Ars : The assumptions of the law of variable proportion are given as below:

(a) It is assumed that the technique of production should remain constant during production.

(b) It operates in the short-run because in the long run, fixed inputs become variable. facto There’s really nothing tricky about price. The basic definition of price the amount of money a customer pays for something is absolutely correct.But to understand the difference between price and marginal revenue, it’s critical to recognize where prices come from.

Hi, I’m Dev Kirtonia, Founder & CEO of Dev Library. A website that provides all SCERT, NCERT 3 to 12, and BA, B.com, B.Sc, and Computer Science with Post Graduate Notes & Suggestions, Novel, eBooks, Biography, Quotes, Study Materials, and more.